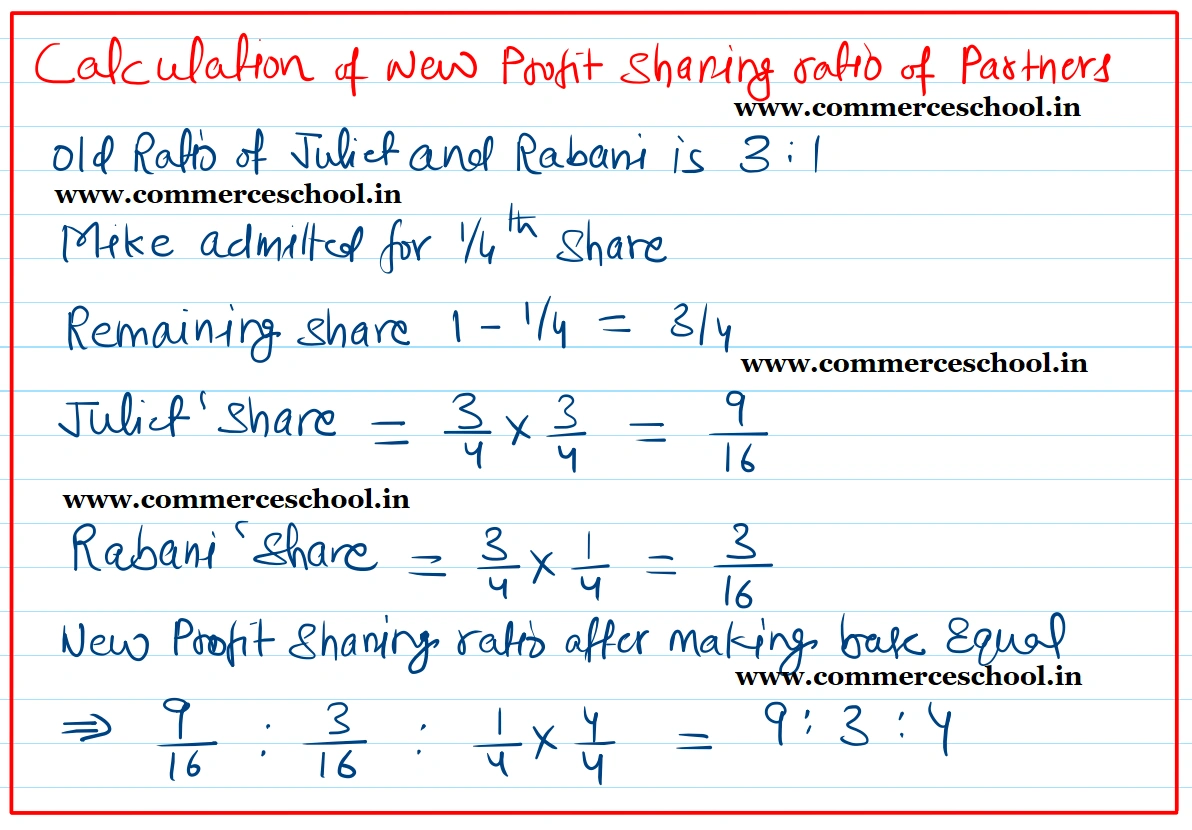

Juliet and Rabani are partners in a firm, sharing profits and losses in the ratio of 3 : 1. On 31st March, 2016, their Balance Sheet was as under:

Juliet and Rabani are partners in a firm, sharing profits and losses in the ratio of 3 : 1. On 31st March, 2016, their Balance Sheet was as under:

Balance Sheet of Juliet and Rabani as at 31st March, 2016

| Liabilities | ₹ | Assets | ₹ |

| Sundry Creditors | 70,000 | Plant and Machinery | 1,76,000 |

| General Reserve | 30,000 | Inventory | 26,000 |

| Provident Fund | 40,000 |

Sundry Debtors 57,000 Less: PDD 3,000 |

54,000 |

|

Capital A/cs: Juliet Rabani |

1,10,000 90,000 |

Cash at Bank | 68,000 |

| Profit & Loss A/c | 16,000 | ||

| 3,40,000 | 3,40,000 |

Mike was taken as a partner for 1/4th share, with effect from 1st April, 2016, subject to the following adjustments:

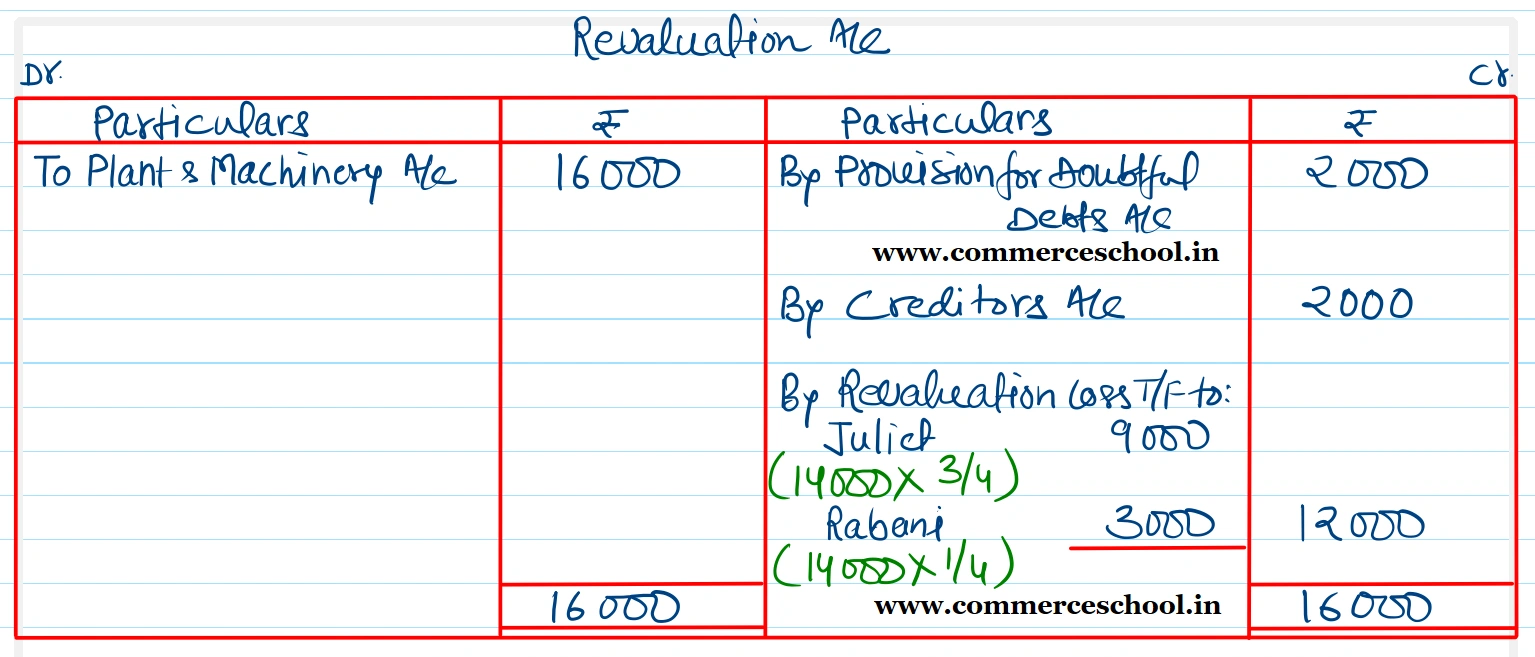

(a) Plant and Machinery was found to be overvalued by ₹ 16,000. It was to be shown in the books at the correct value.

(b) Provision for Doubtful Debts was to be reduced by ₹ 2,000.

(c) Creditors included an amount of ₹ 2,000 received as commission from Malini. The necessary adjustment was required to be made.

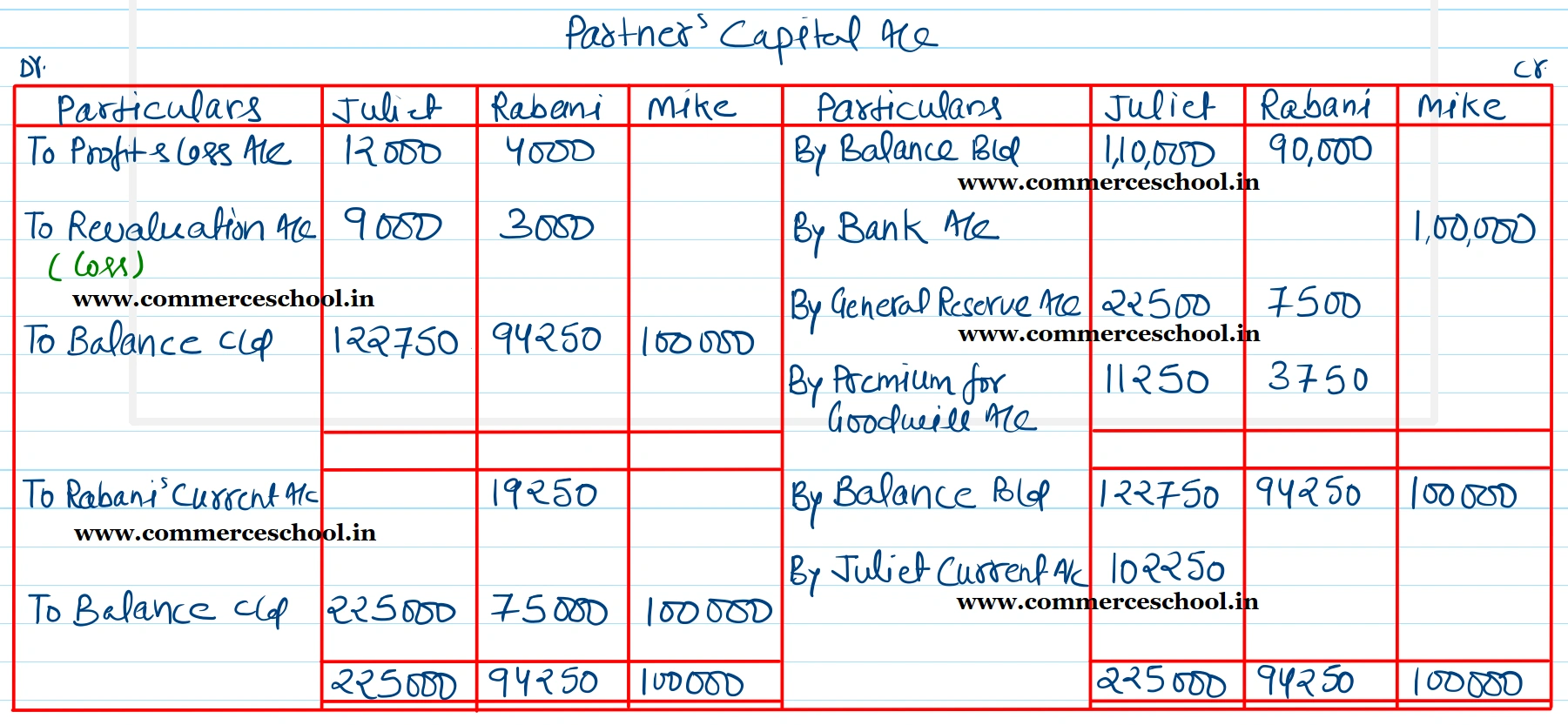

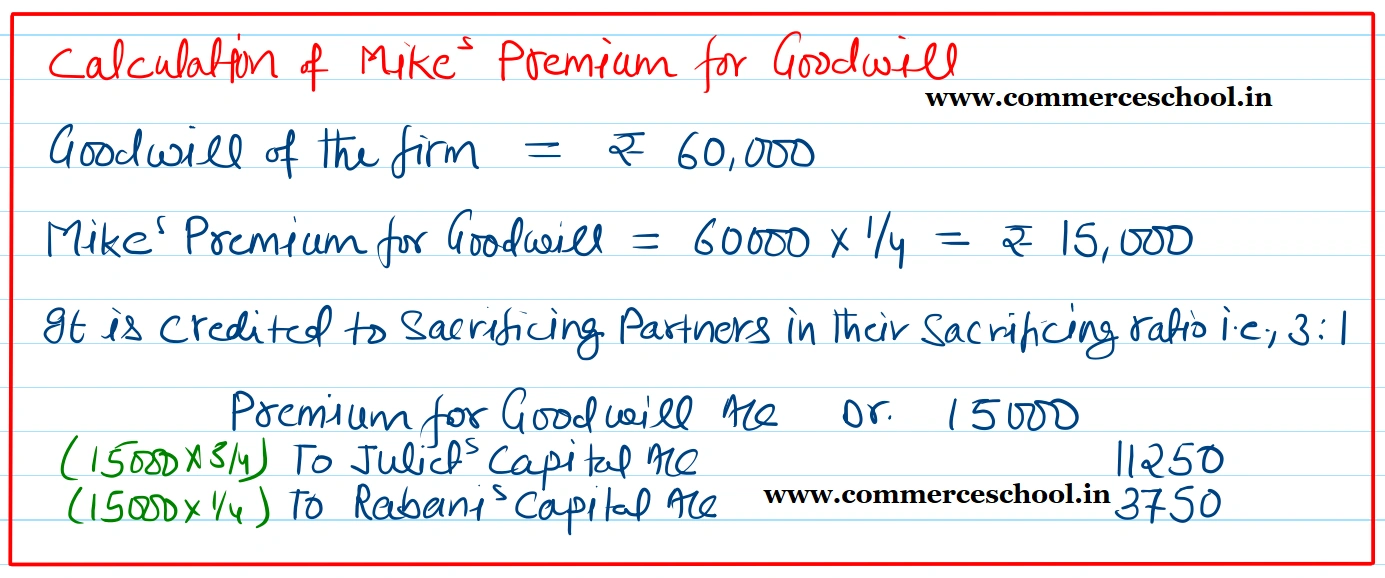

(d) Goodwill of the firm was valued at ₹ 60,000. Mike was to being in cash, his share of goodwill along with his capital of ₹ 1,00,000.

(e) Capital Accounts of juliet and Rabani were to be readjusted in the new profit sharing arragement on the basis of Mike’s capital, any surplus to be adjusted through current account and any deficiency through cash.

You are required to prepare:

(i) Revaluation Account,

(ii) Partner’s Capital Accounts, and

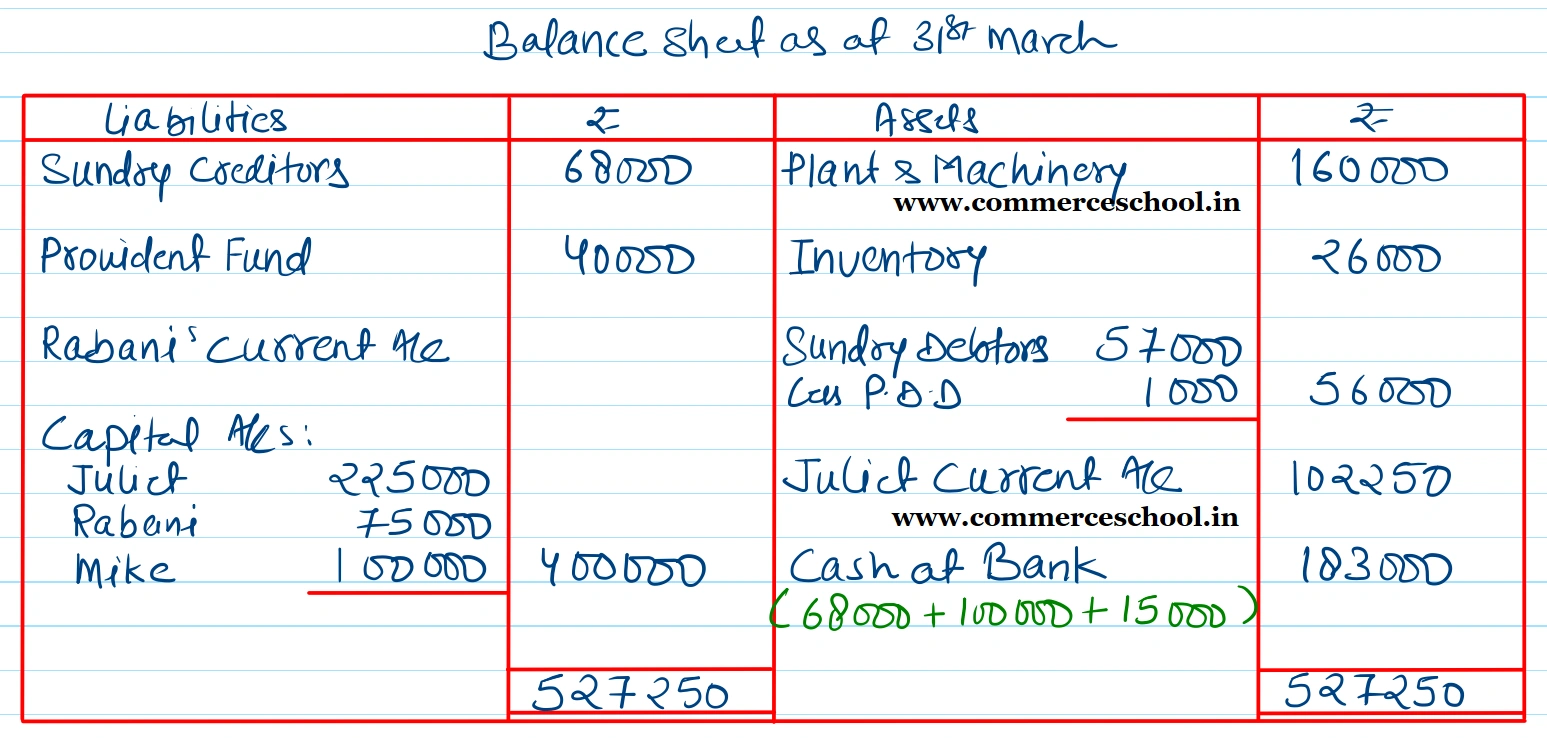

(iii) Balance Sheet of the reconstituted firm.

[Ans. Loss on Revaluation ₹ 12,000; Capital Accounts : Juliett ₹ 2,25,000 and Rabani ₹ 75,000; Juliet brings in ₹ 1,02,250; Rabani’s Current Account (Cr.) ₹ 19,250; Cash at Bank ₹ 2,85,250; B/S total ₹ 5,27,250.]

Anurag Pathak Answered question