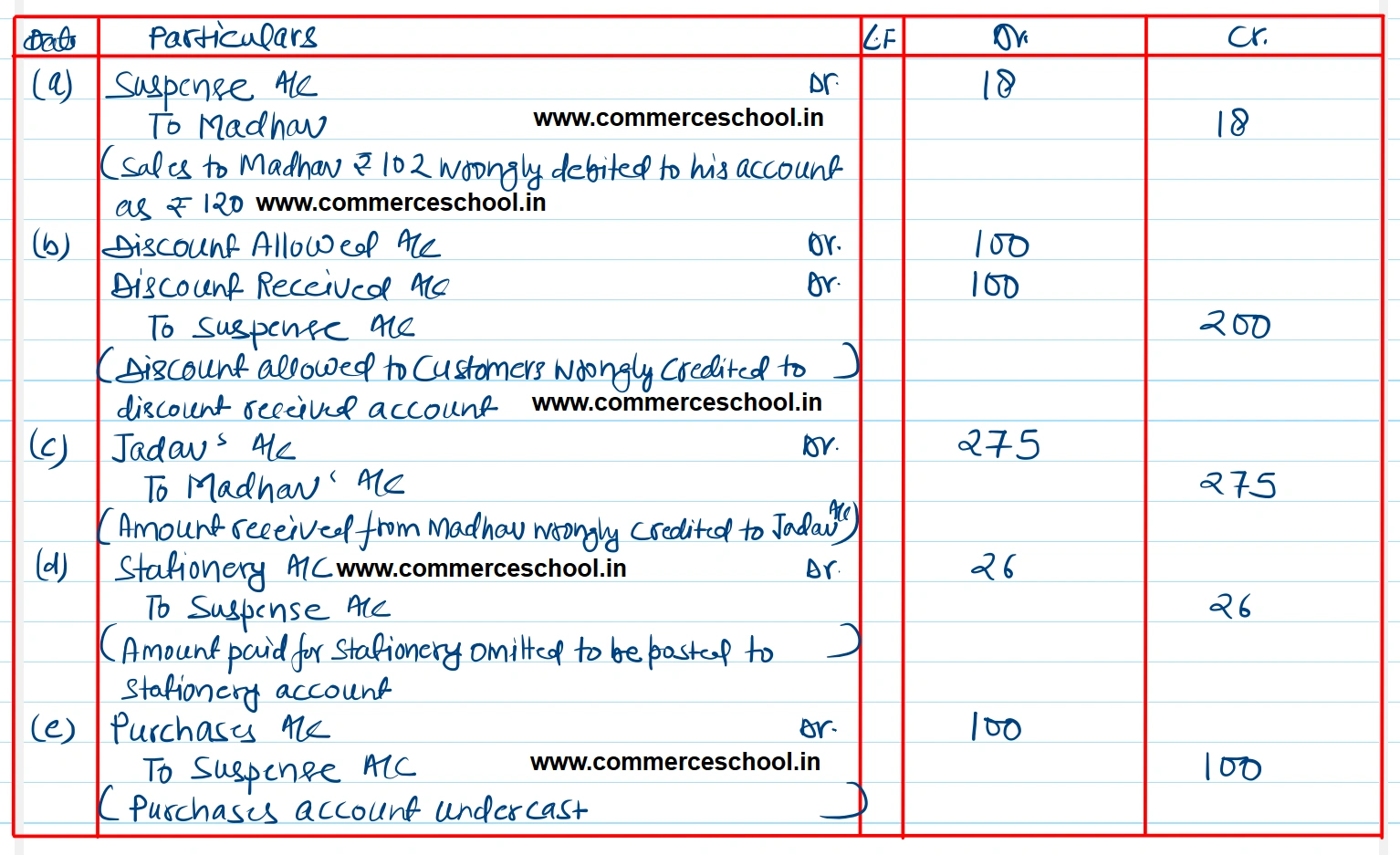

A book-keeper finds that the debit side of the trial balance is short of ₹ 308 and so far the time being, he balances the side by putting the difference to suspense account. Subsequently, the following errors were disclosed

A book-keeper finds that the debit side of the trial balance is short of ₹ 308 and so far the time being, he balances the side by putting the difference to suspense account. Subsequently, the following errors were disclosed:

(a) An entry for sale of goods for ₹ 102 to Madhav was posted to his account as ₹ 120.

(b) ₹ 100 being the discount allowed to customers were credited to discount received account in the ledger.

(c) ₹ 275 paid by Madhav were credited to Jadav’s account.

(d) ₹ 26 appearing in the cash book as paid for the purchase of stationery for office use have not been posted to ledger.

(e) The debit side of purchases account was under-cast by ₹ 100.

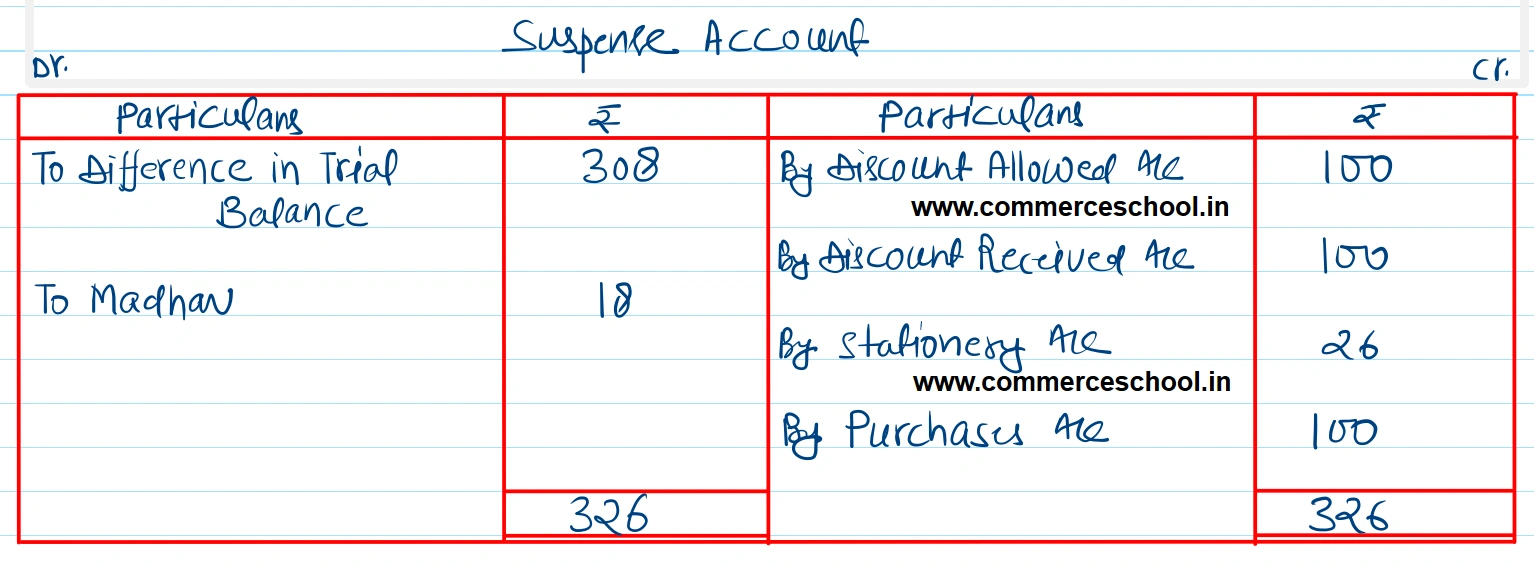

You are required to make the necessary journal entries and the suspense account.

[Ans. Suspense A/c tallies, total of Suspense A/c ₹ 326.]

Anurag Pathak Answered question