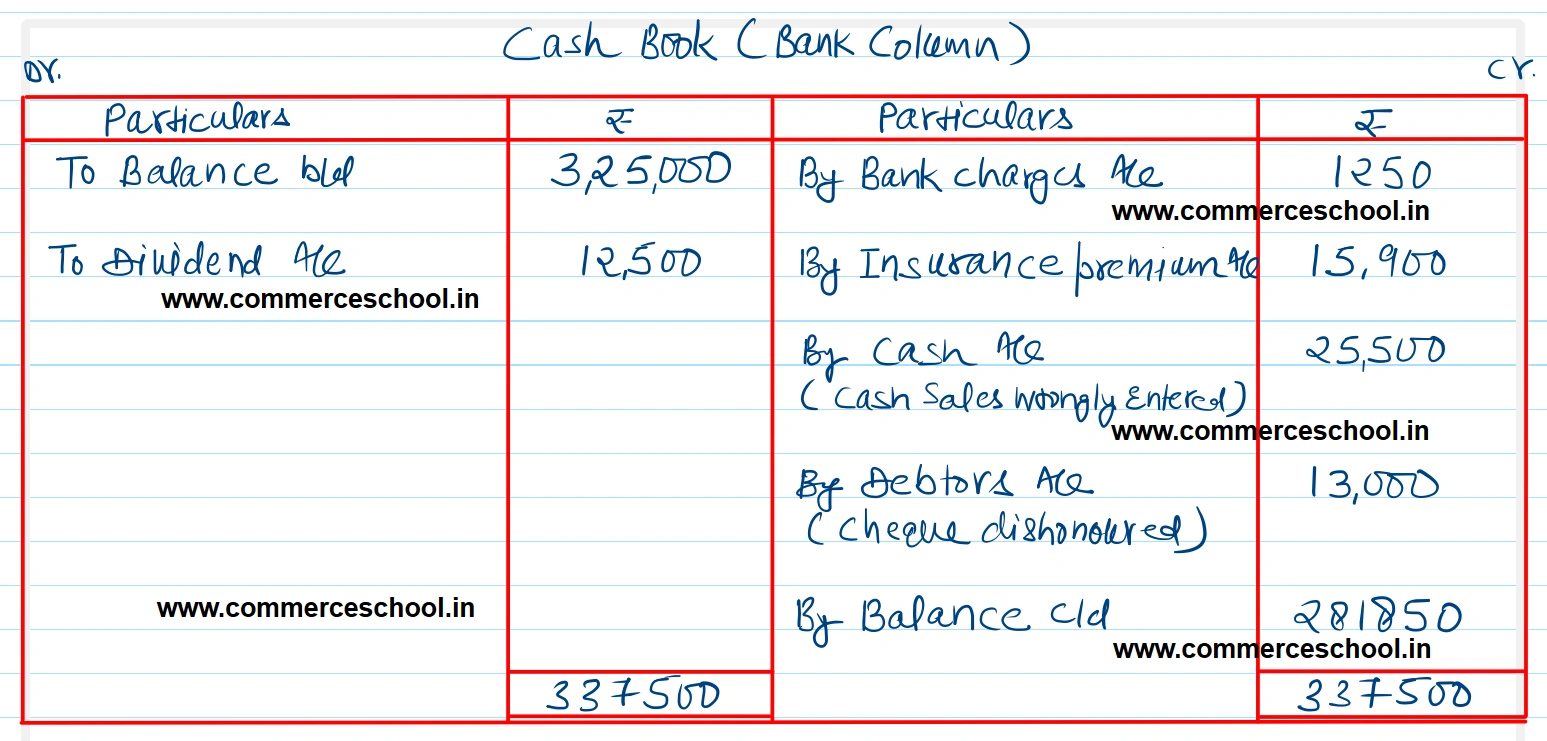

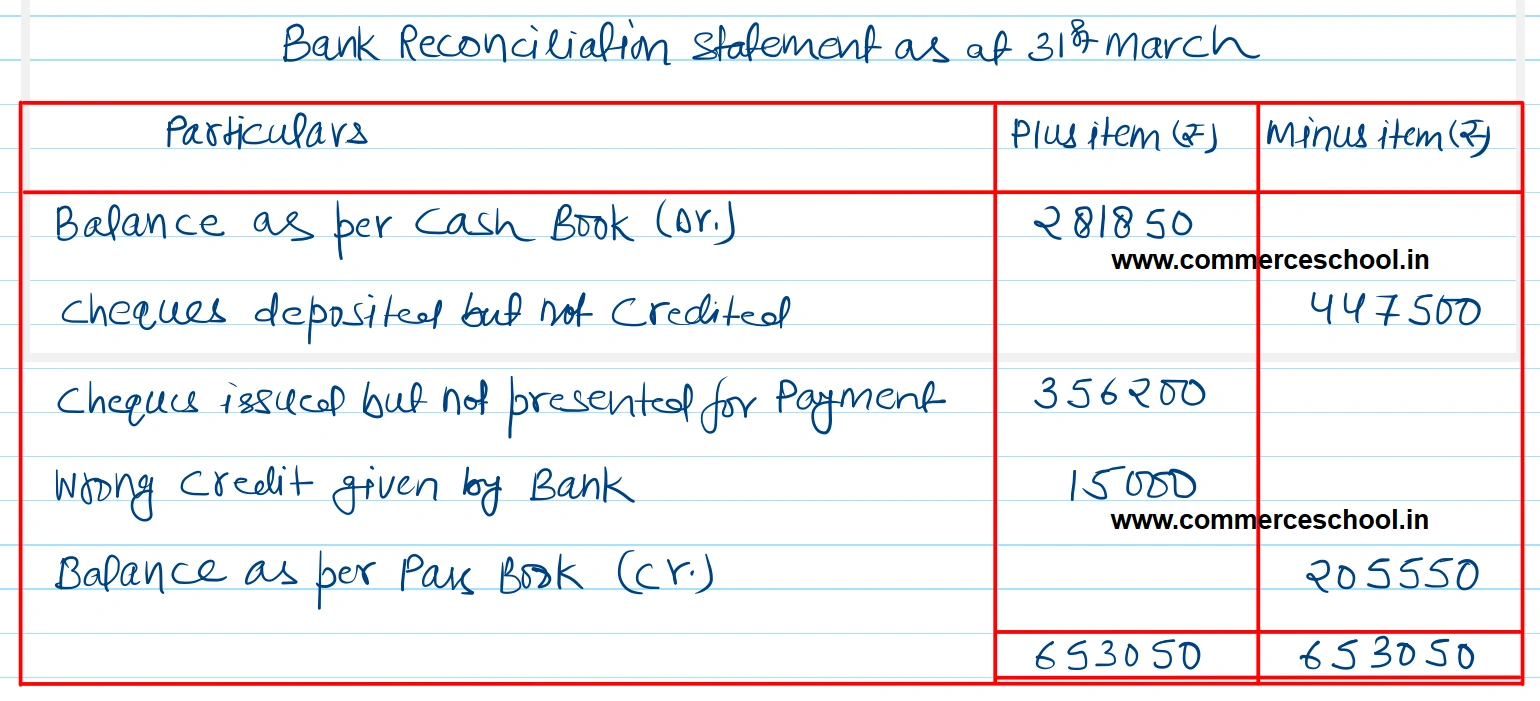

From the following information as on 31st March, 2026, prepare Bank Reconciliation Statement after making necessary amendments in the Cash Book: Bank balance as per Cash Book (Dr.) ₹ 3,25,000

From the following information as on 31st March, 2026, prepare Bank Reconciliation Statement after making necessary amendments in the Cash Book:

Show the bank balance that will be incorporated in the Trial Balance as on 31st March, 2026 and balance as per Bank Pass Book.

| ₹ | ||

| 1 | Bank balance as per Cash Book (Dr.) | 3,25,000 |

| 2 | Cheques deposited but not credited | 4,47,500 |

| 3 | Cheques issued but not presented for payment | 3,56,200 |

| 4 | Bank charges debited by bank but not recorded in Cash Book | 1,250 |

| 5 | Dividend collected by bank | 12,500 |

| 6 | Insurance premium paid by bank as per standing instruction, not intimated | 15,900 |

| 7 | Cash sales wrongly entered in the Bank Column of the Cash Book | 25,500 |

| 8 | Customer’s cheque dishonoured by bank but not recorded in Cash Book | 13,000 |

| 9 | Wrong credit given by bank | 15,000 |

Anurag Pathak Answered question