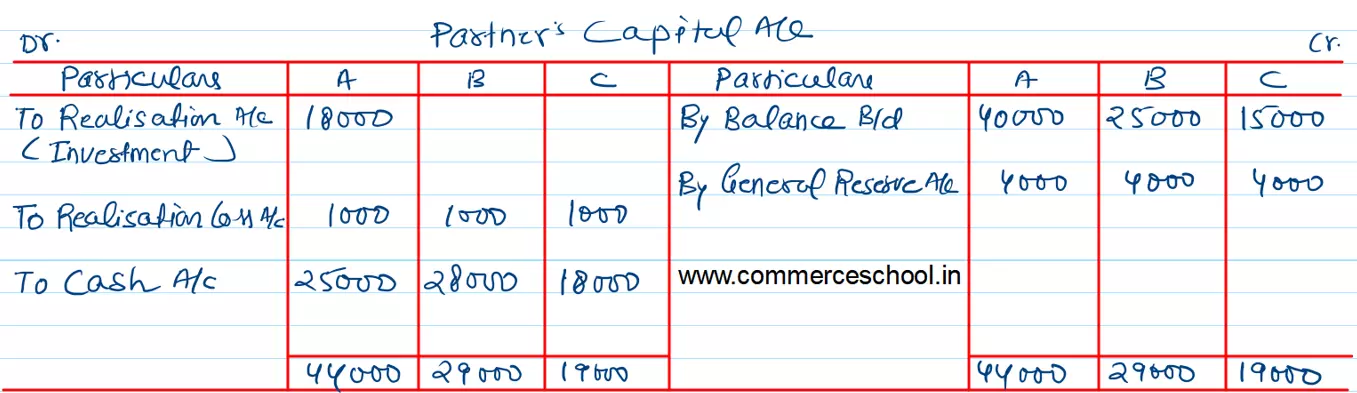

A, B and C were equal partners. On 31st March, 2023, their Balance Sheet stood as:

A, B and C were equal partners. On 31st March, 2023, their Balance Sheet stood as:

| Liabilities | ₹ | Assets | ₹ |

| Creditors

General Reserve Capital A/cs: A B C |

50,400 12,000 40,000 25,000 15,000 |

Cash

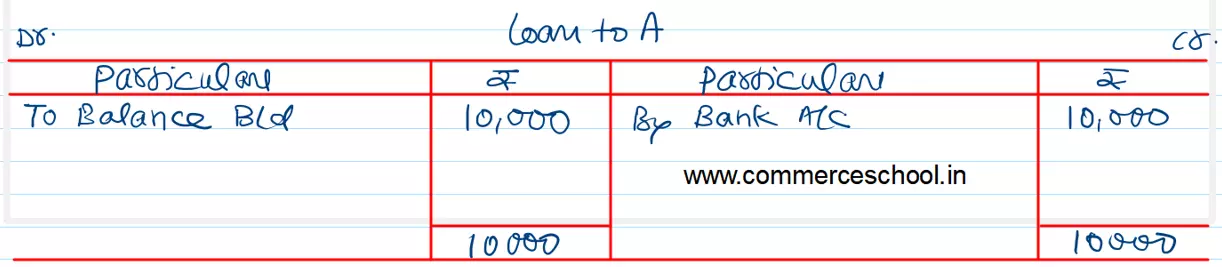

Stock Debtors Loan to A Investments Furniture Building |

3,700 20,100 62,600 10,000 16,000 6,500 23,500 |

| 1,42,400 | 1,42,400 |

The firm was dissolved on the above date on the following terms:

(a) For the purpose of dissolution, investments were valued at ₹ 18,000 and A took over the investments at this value.

(b) Fixed Assets realised ₹ 29,700 whereas Stock and Debtors realised ₹ 80,000.

(c) Expenses of realisation paid were ₹ 1,300.

(d) Creditors allowed discount of ₹ 800.

(e) One Bill Receivable for ₹ 1,500 under discount was dishonoured as the acceptor had become insolvent and was unable to pay anyting and hence the bill had to be met by the firm.

Prepare Realisation Account, Partner’s Capital Accounts and Cash Account showing how the accounts would finally be settled among the partners.

[Ans,: Loss on Realisation – ₹ 3,000; Cash paid to A, B and C – ₹ 25,000; ₹ 28,000; ₹ 18,000 respectively. Total of Cash Account – ₹ 1,23,400.]

Anurag Pathak Changed status to publish