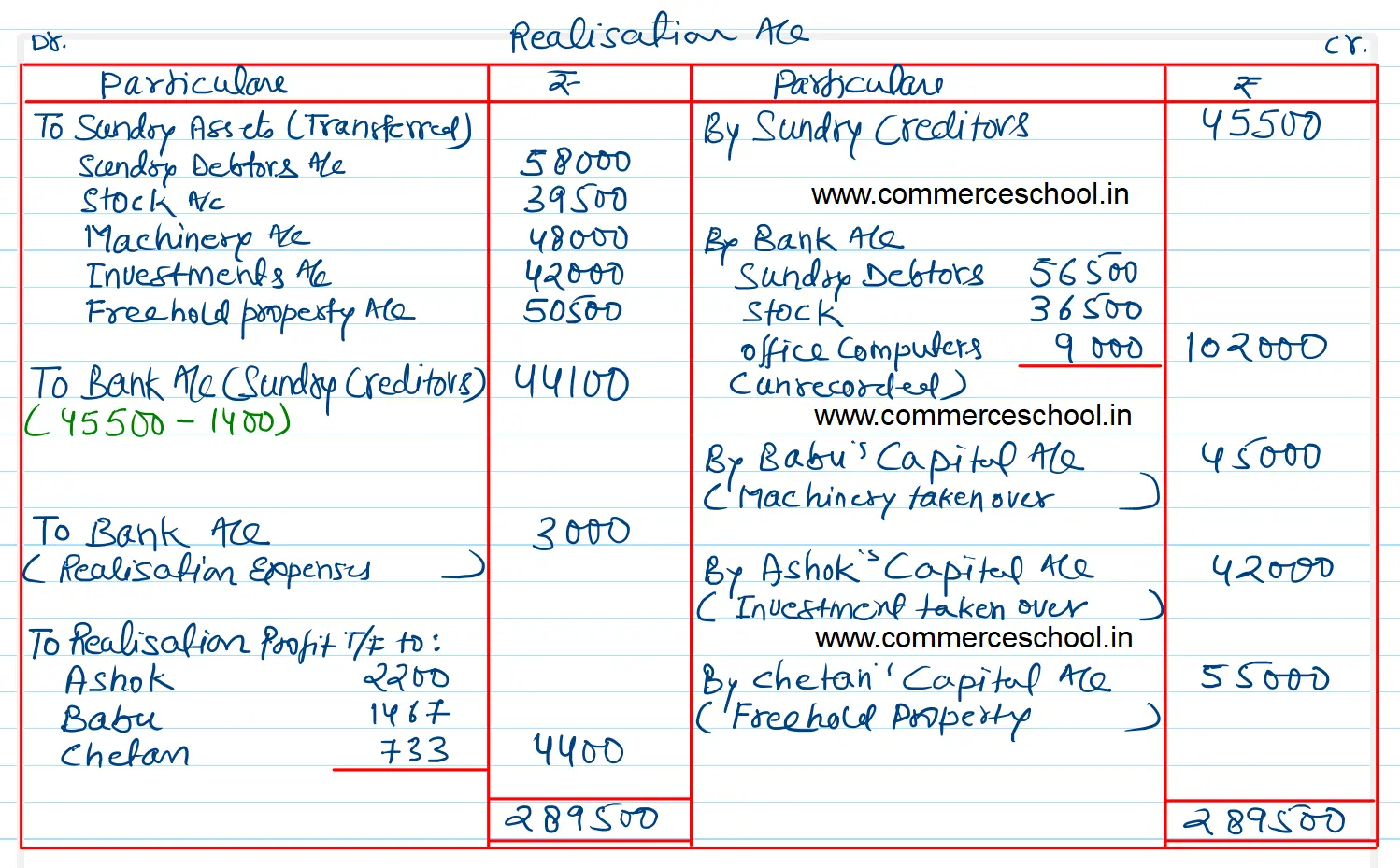

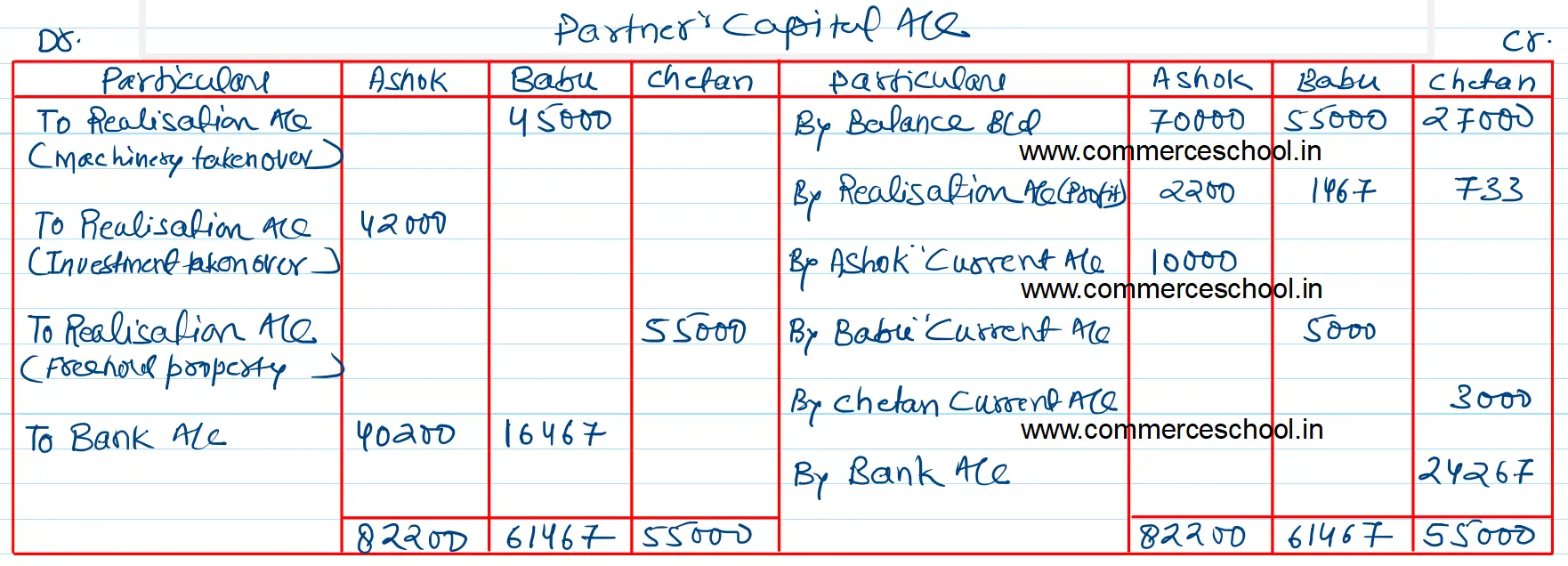

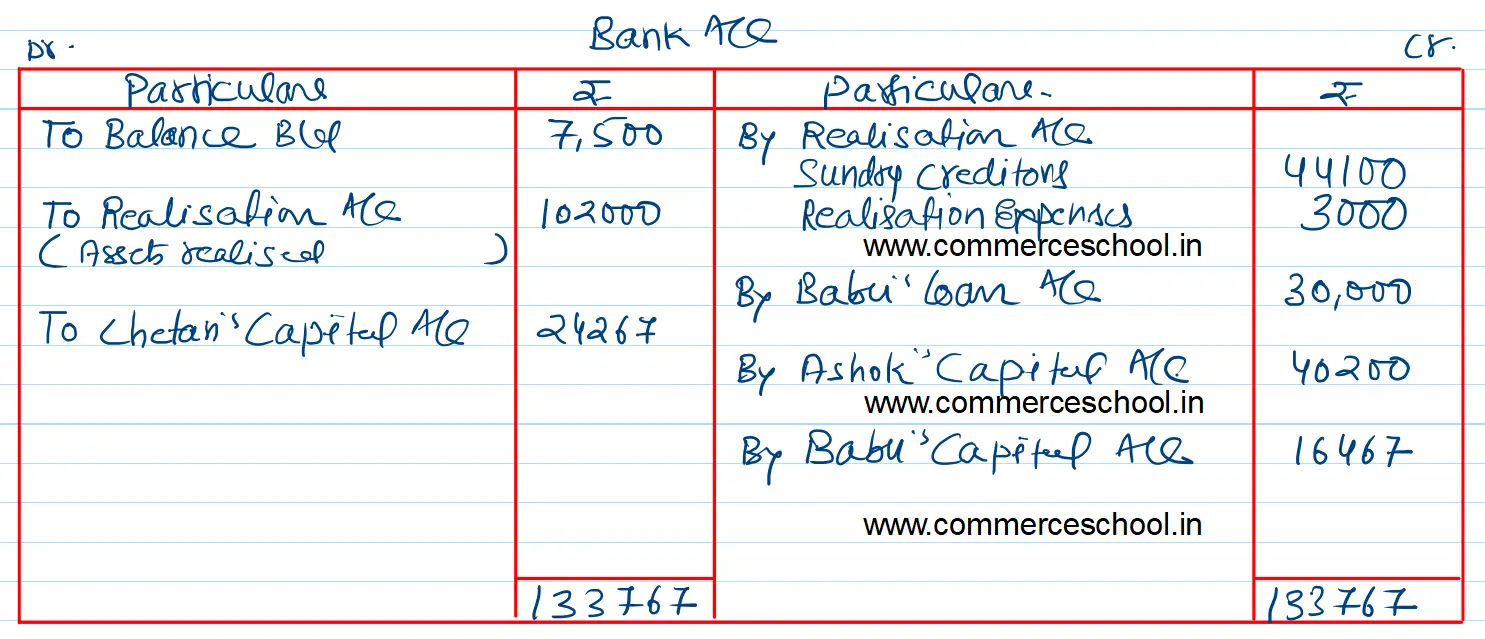

Ashok, Babu and Chetan are in partnership sharing profit in the proportion of 1/2, 1/3, 1/6 respectively. They dissolve the partnership on 31st March, 2023 when the Balance Sheet of the firm is as under:

Ashok, Babu and Chetan are in partnership sharing profit in the proportion of 1/2, 1/3, 1/6 respectively. They dissolve the partnership on 31st March, 2023 when the Balance Sheet of the firm is as under:

| Liabilities | ₹ | Assets | ₹ |

| Sundry Creditors

Loan by Babu Capital A/cs: Ashok Babu Chetan Curent A/cs: Ashok Babu Chetan |

45,500 30,000 70,000 55,000 27,000 10,000 5,000 3,000 |

Bank

Sundry Debtors Stock Machinery Investments Freehold Property |

7,500 58,000 39,500 48,000 42,000 50,500 |

| 2,45,500 | 2,45,500 |

The Machinery was taken by Babu for ₹ 45,000, Ashok took over the Investments and Freehold property was taken by Chetan at ₹ 55,000. The remaining Assets realised as follows:

Sundry Debtors ₹ 56,600 and Stock ₹ 36,500. Sundry Creditors were settled at discount of 7%. An office computer, not shown in the books of accounts realised ₹ 9,000. Realisation expenses amounted to ₹ 3,000.

Prepare Realisation Account, Partner’s Capital Accounts and Bank Account.

[Ans.: Gain (profit) on Realisation – ₹ 4,400; Final Payments; Ashok – ₹ 40,200; Babu – ₹ 16,467. Amount brought by Chetan – ₹ 24,267; Total of Bank Account – ₹ 1,33,767.]

Anurag Pathak Changed status to publish