Total of one page of the Sales Book was carried forward to the next page as ₹ 2,785 instead of ₹ 2,587.

Rectify the following errors:

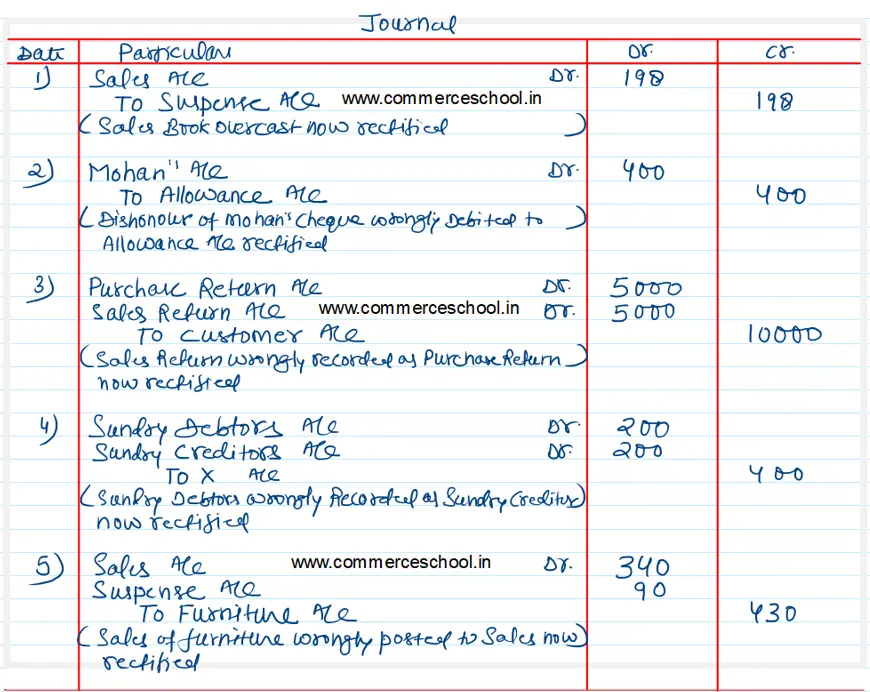

(i) Total of one page of the Sales Book was carried forward to the next page as ₹ 2,785 instead of ₹ 2,587.

(ii) A cheque of ₹ 400 received from Mohan was dishonoured and had been poted to the debit side of the ‘Allowance Account’.

(iii) Return of goods worth ₹ 5,000 by a customer was entered in the Purchases Return Book.

(iv) Sum of ₹ 200 owed by ‘X’ has been included in the list of Sundry Creditors.

(v) Sale of old furniture worth ₹ 430 was credited to the Sales Account as ₹ 340.

Anurag Pathak Changed status to publish