A and B sharing profits and losses in the ratio of 2 : 3 decide to share future profits and losses equally with effect from 1st April, 2024. An extract of their Balance Sheet as at 31st March, 2024 is as follows

A and B sharing profits and losses in the ratio of 2 : 3 decide to share future profits and losses equally with effect from 1st April, 2024. An extract of their Balance Sheet as at 31st March, 2024 is as follows:

| Liabilities | ₹ | Assets | ₹ |

| Workmen Compensation Reserve | 40,0000 |

Show the accounting treatment under the following alternative cases:

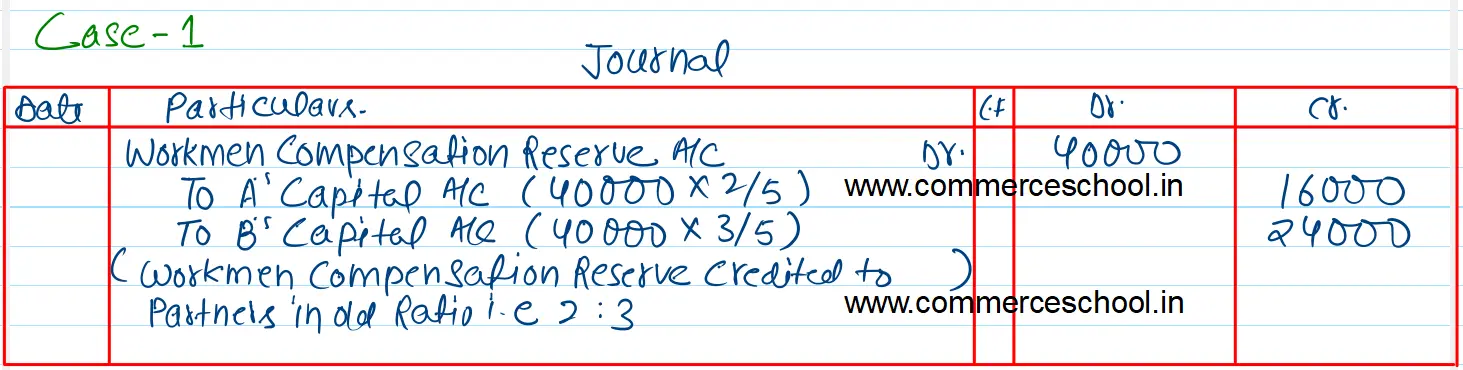

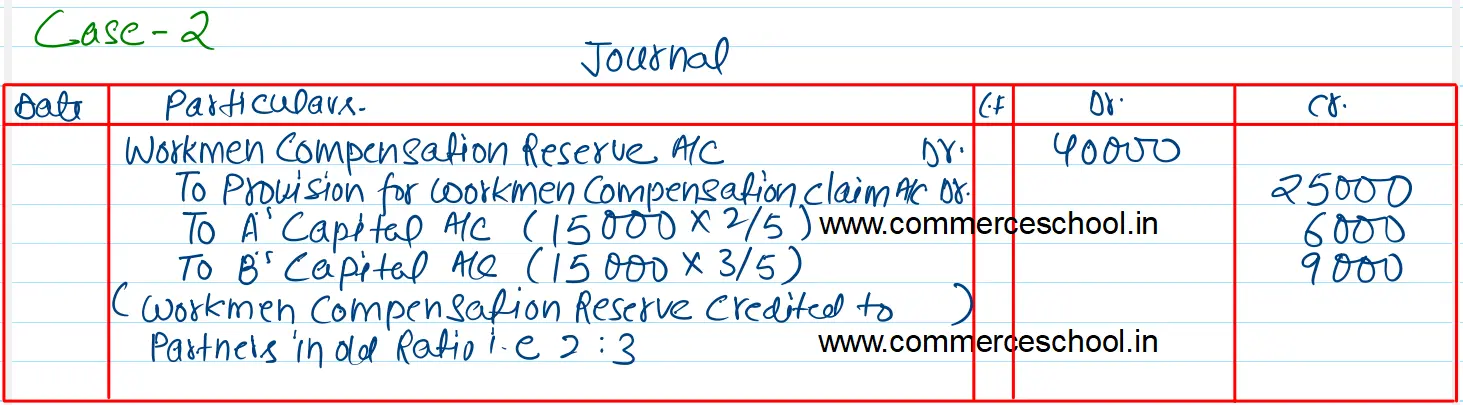

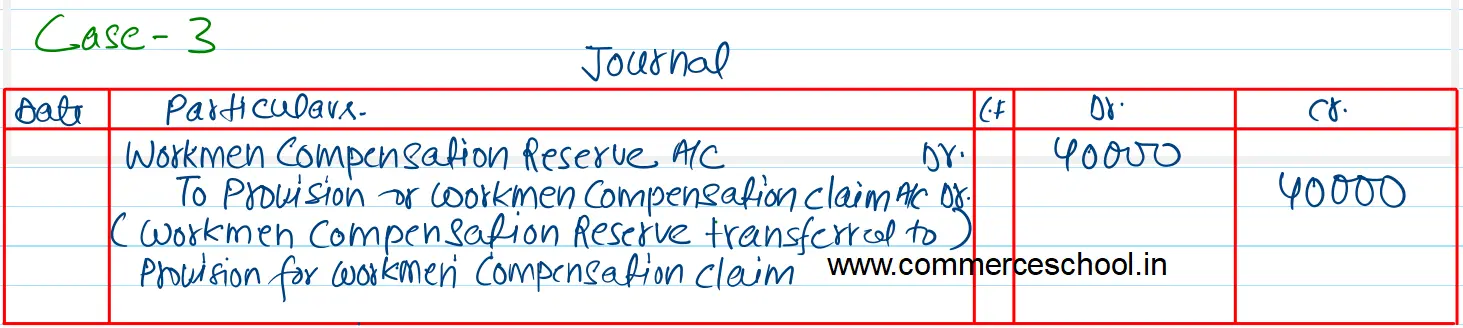

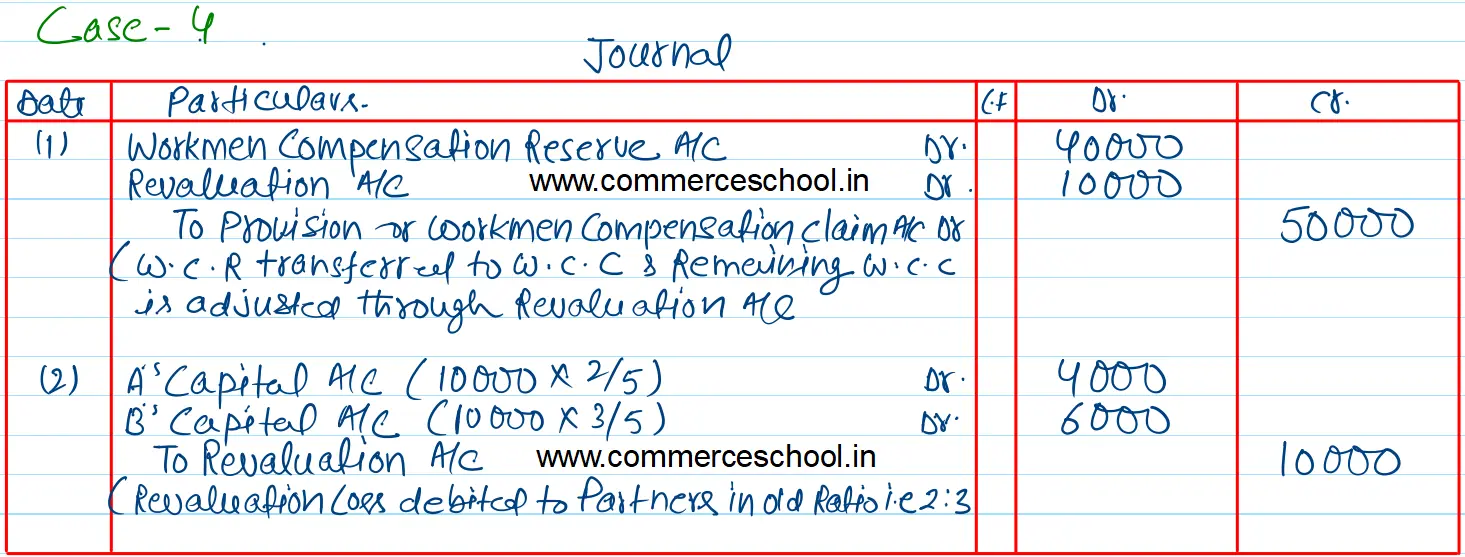

Case (i) If there is no other information. Case (ii) If a claim on account of Workmen’s Compensation is estimated at ₹ 25,000. Case (iii) If a claim on account of Workmen’s Compensation is estimated at ₹ 40,000 Case (iv) If a claim on account of Workmen’s Compensation is estimated at ₹ 50,000.

Anurag Pathak Answered question

Solution:-

In the absence of further information Workmen Compensation Reserve is credited to the partners in their old profit sharing ratio.

In the absence of further information Workmen Compensation Reserve is credited to the partners in their old profit sharing ratio after adjusting the Workmen Compensation Claim.

If the Workmen Compensation Claim is equal to the Workmen Compensation Reserve, nothing would be distributed among the partners.

If Workmen Compensation Claim is more than the Workmen Compensation Reserve, the excess is adjusted through the revaluation account.

Anurag Pathak Edited answer