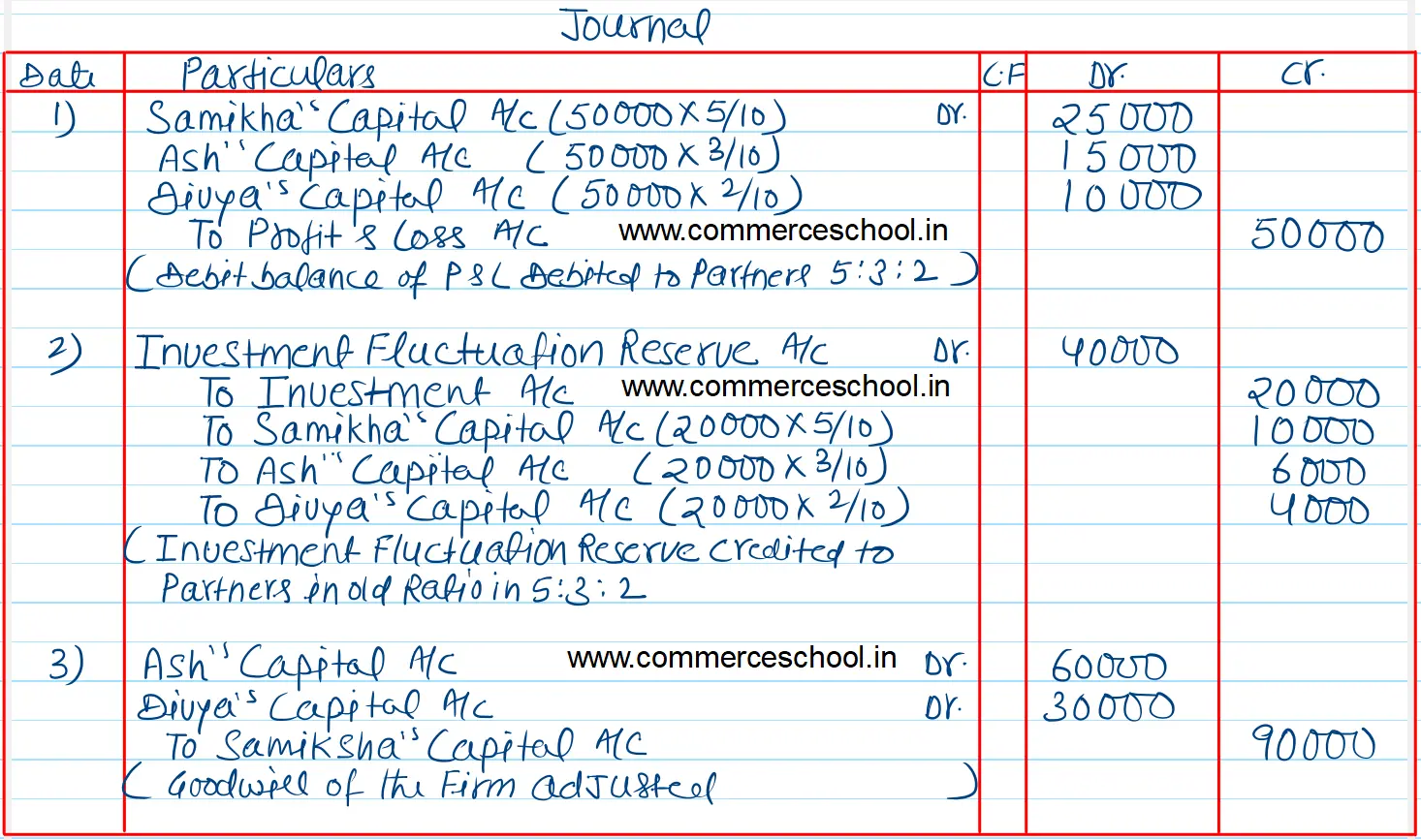

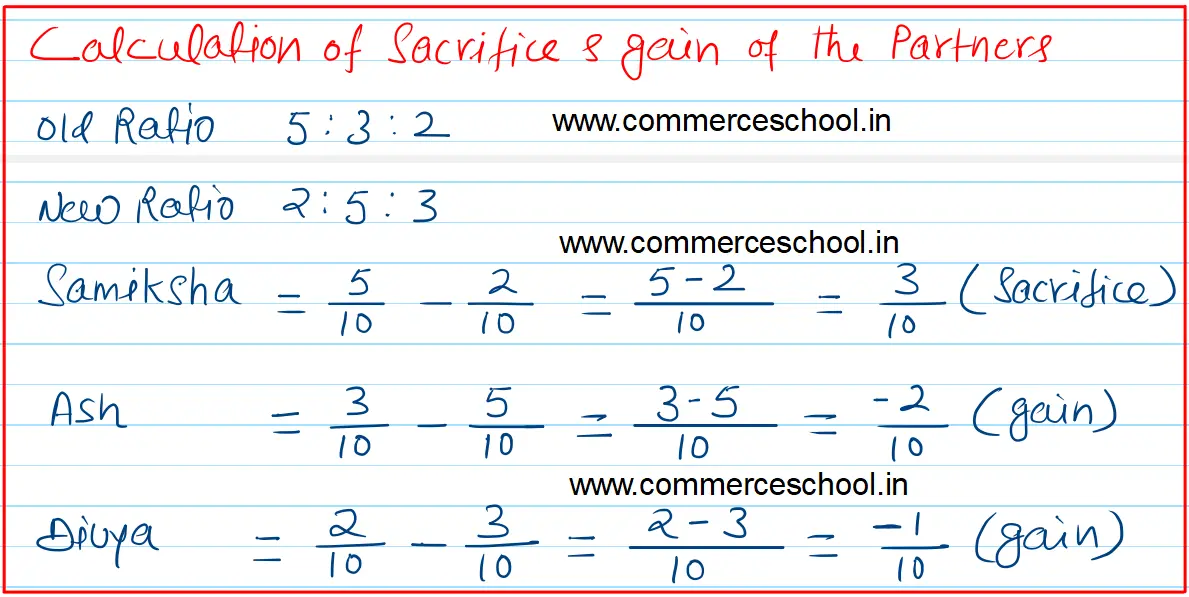

Samiksha, Ash and Divya were partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. With effect from 1st April, 2019, they agreed to share future profits and losses in the ratio of 2 : 5 : 3

Samiksha, Ash and Divya were partners in a firm sharing profits and losses in the ratio of 5 : 3 : 2. With effect from 1st April, 2019, they agreed to share future profits and losses in the ratio of 2 : 5 : 3. Their Balance Sheet showed a debit balance of ₹ 50,000 in the Profit and Loss Account and a balance of ₹ 40,000 in the Investment Fluctuation Reserve. For this purpose, It was agreed that:

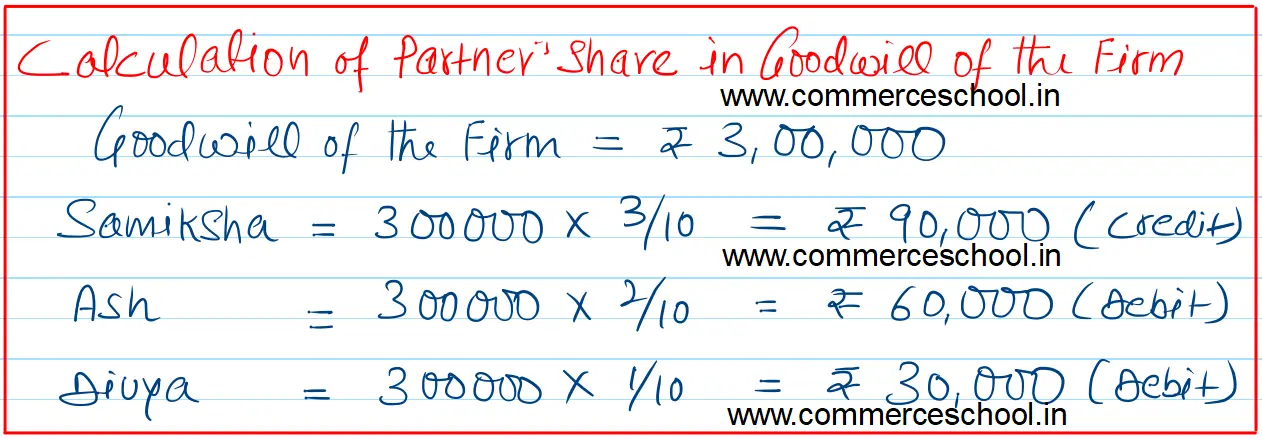

(i) Goodwill of the firm be valued at ₹ 3,00,000.

(ii) Investment of book value of ₹ 5,00,000 be valued at ₹ 4,80,000.

Pass the necessary journal entries to record the above transactions in the books of the firm.

[Ans. Excess Investment Fluctuation Reserve ₹ 20,000 credited to Partner’s Capital Accounts in old ratio. Adjustment for Goodwill : Debit Ash by ₹ 60,000 and Divya by ₹ 30,000 and Credit Samiksha by ₹ 90,000.]

Anurag Pathak Answered question