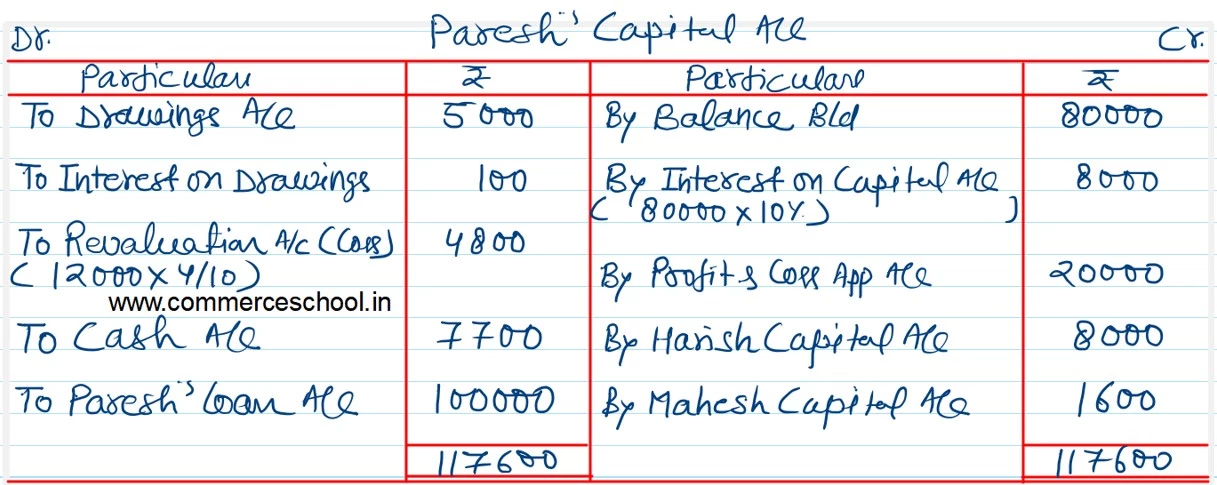

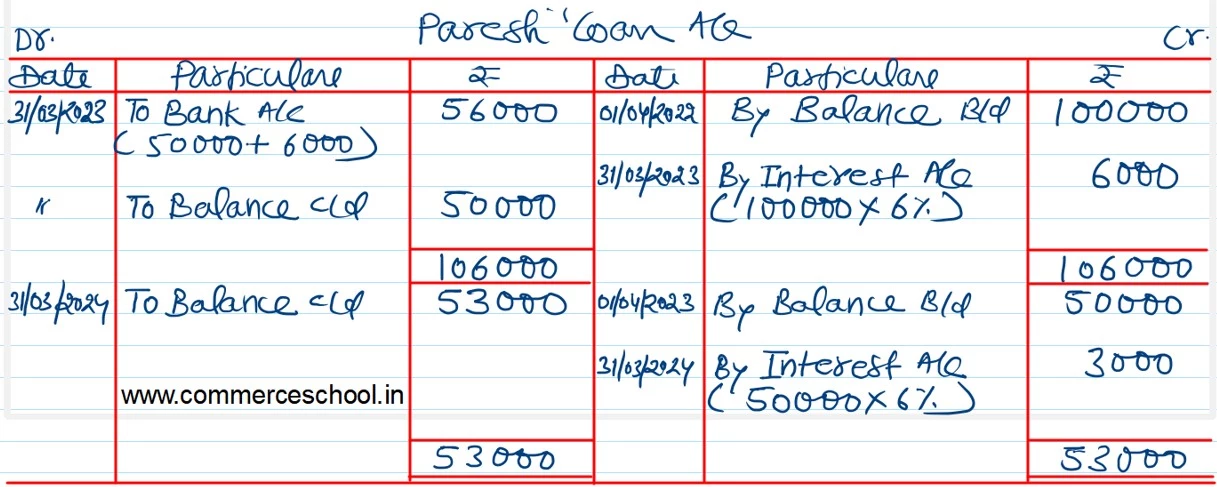

Harish, Paresh and Mahesh were three partners sharing profits and losses in the ratio of 5 : 4 : 1. Paresh retired on 31st March, 2022. His capital as on 1st April, 2021, was ₹ 80,000. During the year 2021-22, he withdrew ₹ 5,000. He was to be charged interest of ₹ 100 on drawings. The Partnership Deed provides that on the retirement of a partner, he will be entitled to: i) His share of capital. ii) Interest on capital @ 10% per annum. iii) His share of profit in the year of retirement. iv) His share of goodwill of the firm. v) His share in the profit/loss on revaluation of assets and liabilities. Additional Information: a) Paresh’s share in the profit of the firm for the year 2021-22 was ₹ 20,000. b) Goodwill of the firm was valued at ₹ 24,000. c) The firm incurred loss of ₹ 12,000 on the revaluation of assets and liabilities. d) Paresh was to be paid ₹ 7,700 in cash and the balance was to be transferred to his loan account bearing interest @ 6% p.a. Loan was to be repaid in two equal annual installments, the first installment to be paid on 31st March 2023. You are required to prepare: (i) Paresh’s Capital Account. (ii) Paresh’s Loan Account till it is finally closed. [Ans.: Paresh’s Loan – ₹ 1,00,000]

Harish, Paresh and Mahesh were three partners sharing profits and losses in the ratio of 5 : 4 : 1.

Paresh retired on 31st March, 2022. His capital as on 1st April, 2021, was ₹ 80,000. During the year 2021-22, he withdrew ₹ 5,000. He was to be charged interest of ₹ 100 on drawings.

The Partnership Deed provides that on the retirement of a partner, he will be entitled to:

i) His share of capital.

ii) Interest on capital @ 10% per annum.

iii) His share of profit in the year of retirement.

iv) His share of goodwill of the firm.

v) His share in the profit/loss on revaluation of assets and liabilities.

Additional Information:

a) Paresh’s share in the profit of the firm for the year 2021-22 was ₹ 20,000.

b) Goodwill of the firm was valued at ₹ 24,000.

c) The firm incurred loss of ₹ 12,000 on the revaluation of assets and liabilities.

d) Paresh was to be paid ₹ 7,700 in cash and the balance was to be transferred to his loan account bearing interest @ 6% p.a. Loan was to be repaid in two equal annual installments, the first installment to be paid on 31st March 2023.

You are required to prepare:

(i) Paresh’s Capital Account.

(ii) Paresh’s Loan Account till it is finally closed.

[Ans.: Paresh’s Loan – ₹ 1,00,000]

Anurag Pathak Changed status to publish