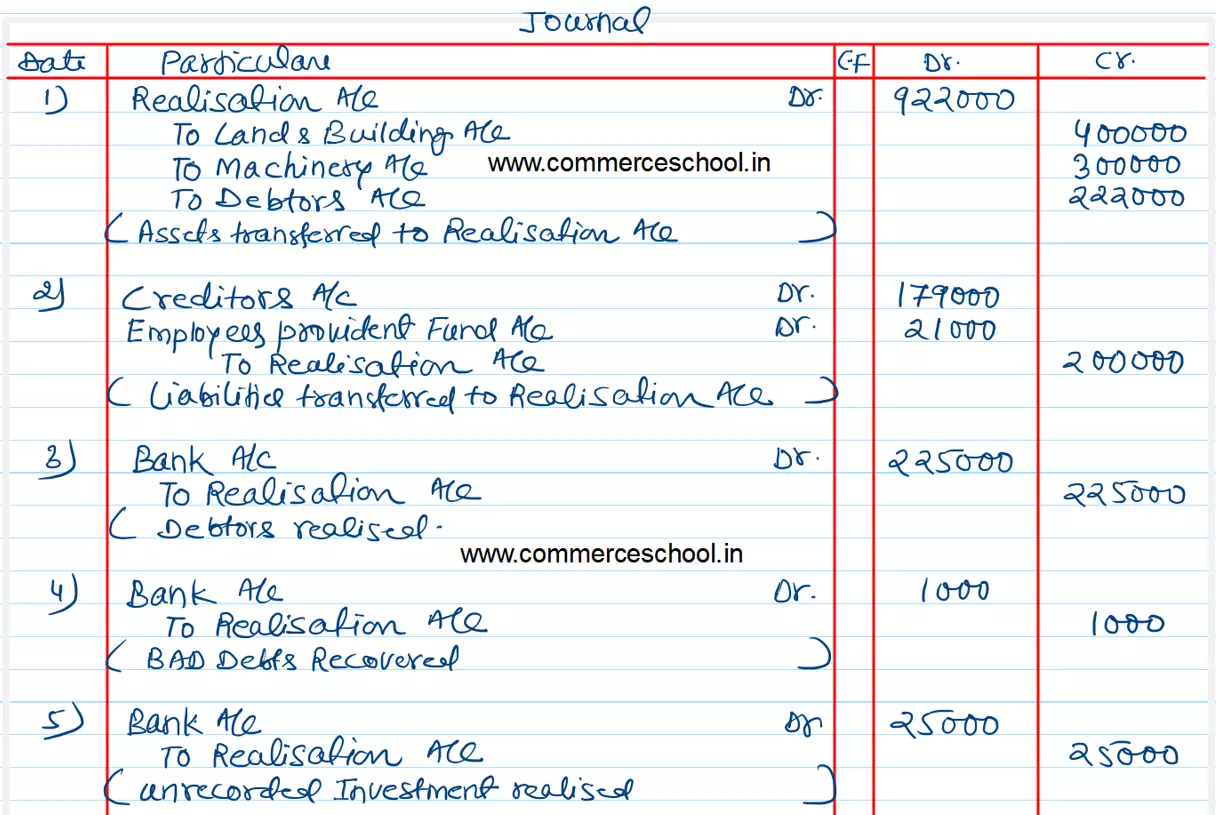

Achal and Vichal were partners in a firm sharing profits in the ratio of 3 : 5. On 31st March, 2023, their Balance Sheet was as follows:

Achal and Vichal were partners in a firm sharing profits in the ratio of 3 : 5. On 31st March, 2023, their Balance Sheet was as follows:

| Liabilities | ₹ | Assets | ₹ |

| Capital A/cs:

Achal Vichal Creditors Employee’s Provident Fund |

3,00,000

5,00,000 1,79,000 21,000 |

Land and Building

Machinery Debtors Cash at Bank |

4,00,000

3,00,000 2,22,000 78,000 |

| 10,00,000 | 10,00,000 |

The firm was dissolved on 1st April, 2023 and the assets and liabilities were settled as follows:

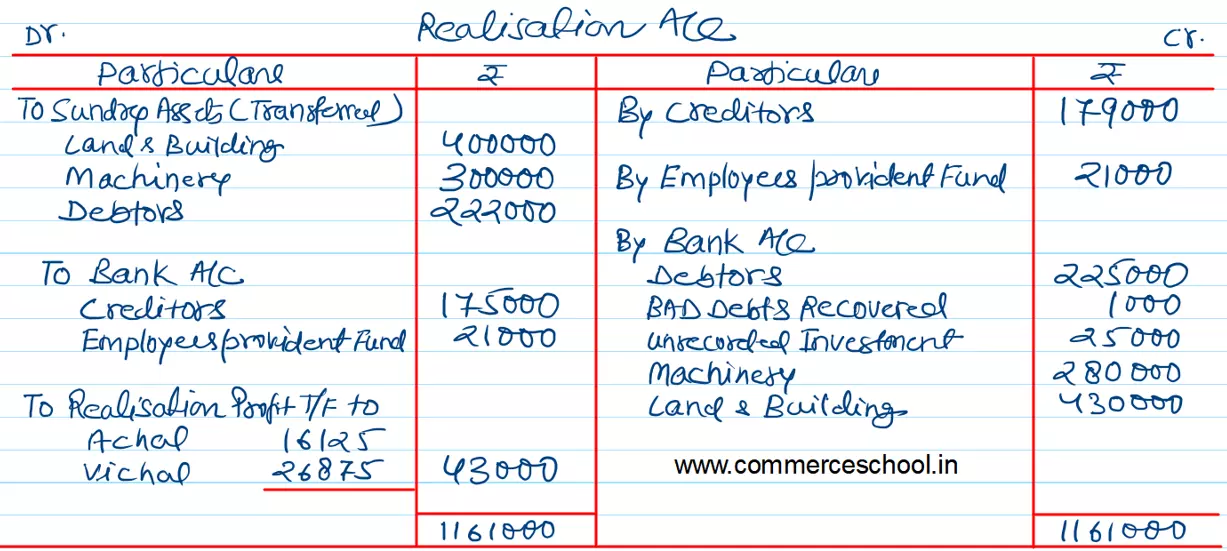

(a) Land and Building realised ₹ 4,30,000.

(b) Debtors realised ₹ 2,25,000 (with interest) and ₹ 1,000 were recovered for Bad Debts written off last year.

(c) There was an unrecorded Investment which was sold for ₹ 25,000.

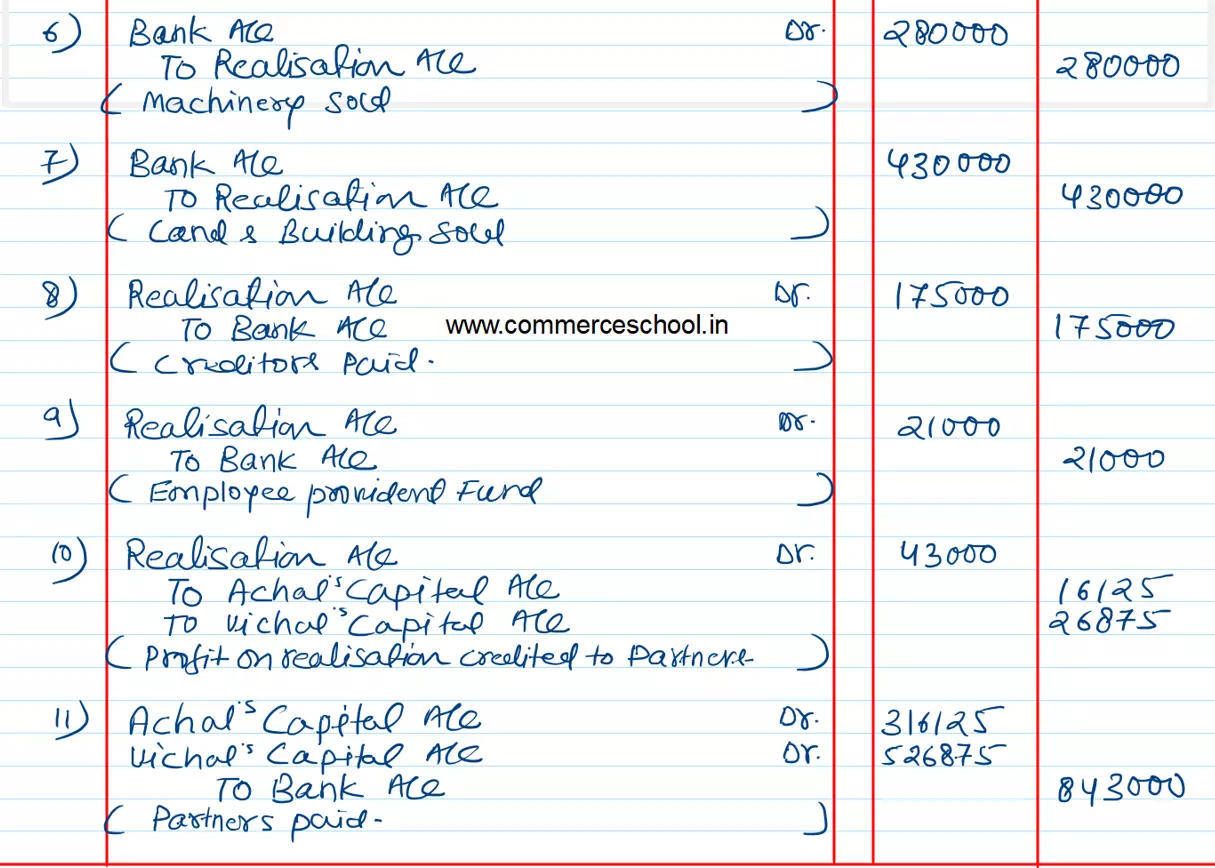

(d) Vichal took over machinery at ₹ 2,80,000 for cash.

(e) 50% of the Creditors were paid ₹ 4,000 less in full settlement and the reamining Creditors were paid full amount.

Pass necessary Journal entries for dissolution of the firm.

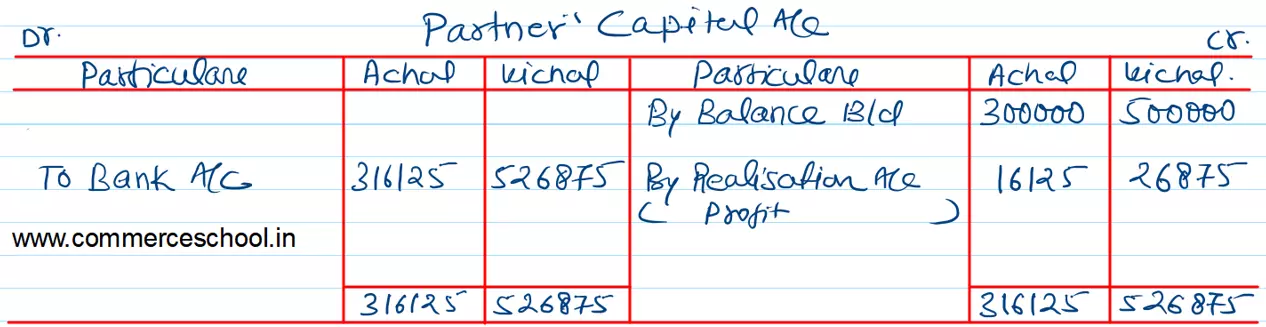

[Ans.: Gain (Profit) on Realistion – ₹ 43,000; Final Payments: Achal – ₹ 3,16,125; Vichal – ₹ 5,26,875.]

Anurag Pathak Changed status to publish