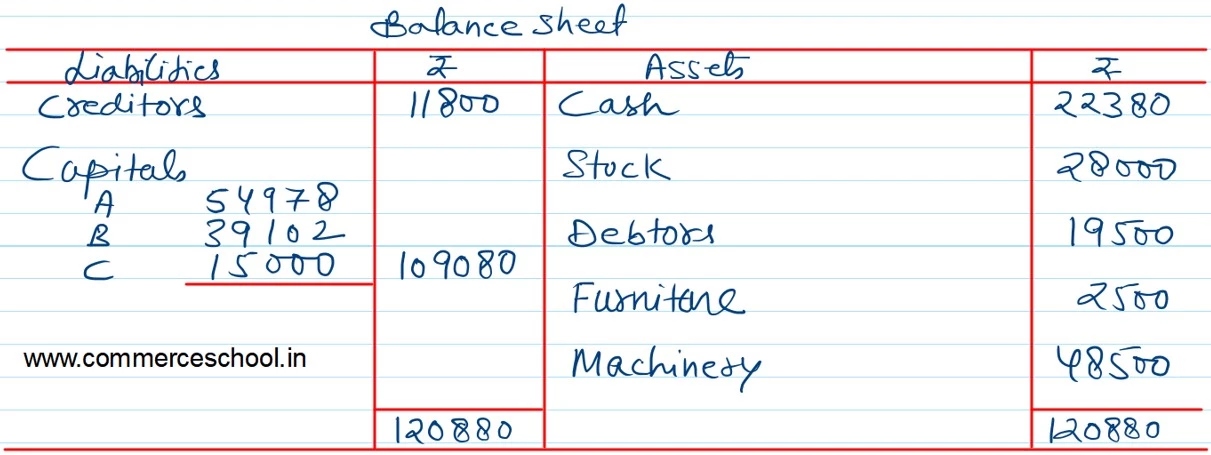

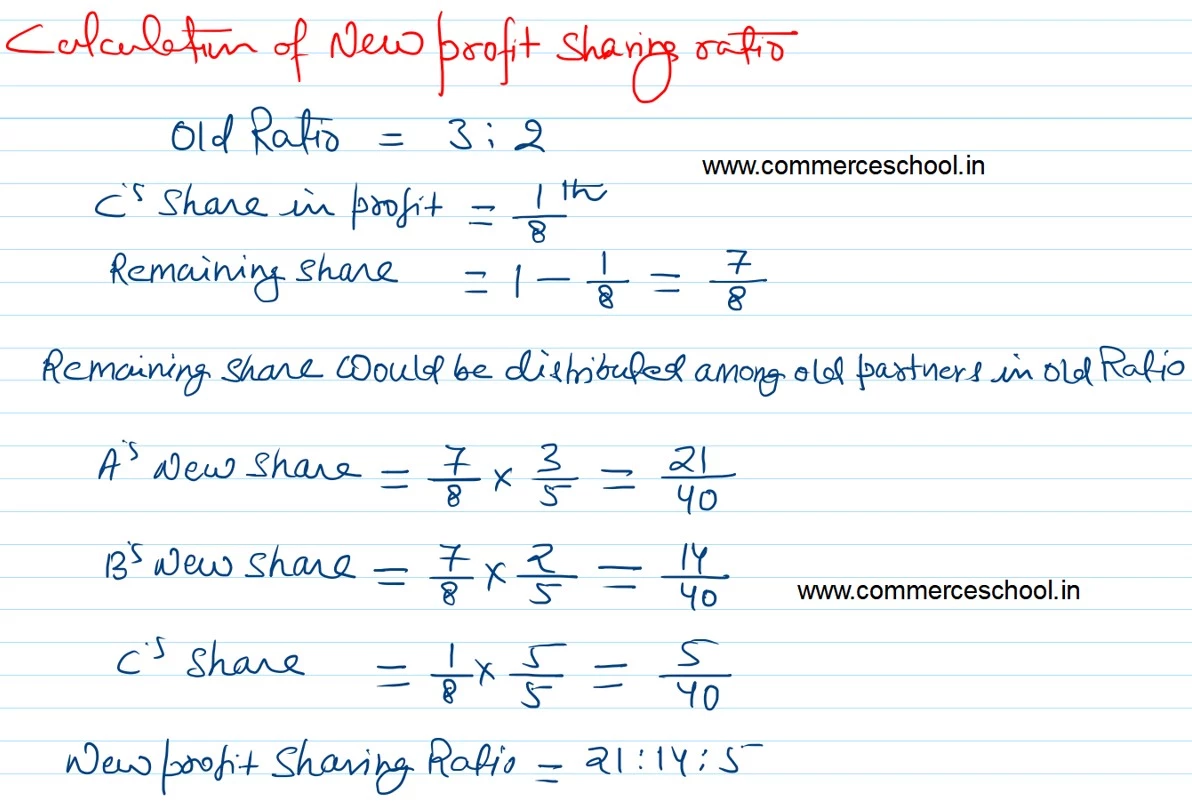

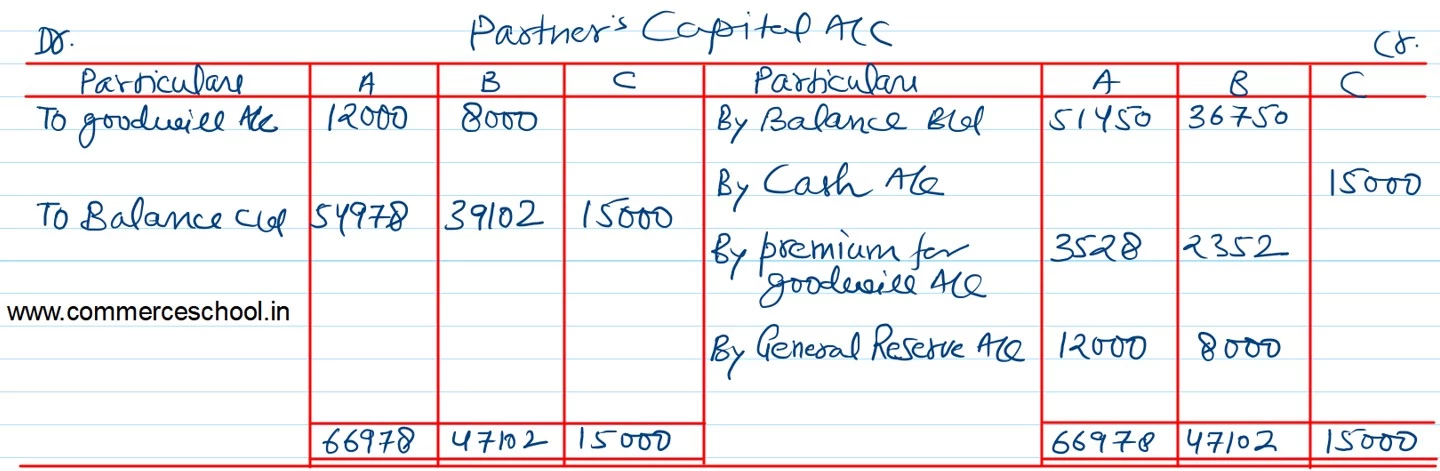

A and B are carrying on business in partnership and sharing profits and losses in the ratio of 3 : 2. Their Balance Sheet as at 31st March, 2023 stood as:

A and B are carrying on business in partnership and sharing profits and losses in the ratio of 3 : 2. Their Balance Sheet as at 31st March, 2023 stood as:

| Liabilities | ₹ | Assets | ₹ |

| Creditors

General Reserve A’s Capital B’s Capital |

11,800 20,000 51,450 36,750 |

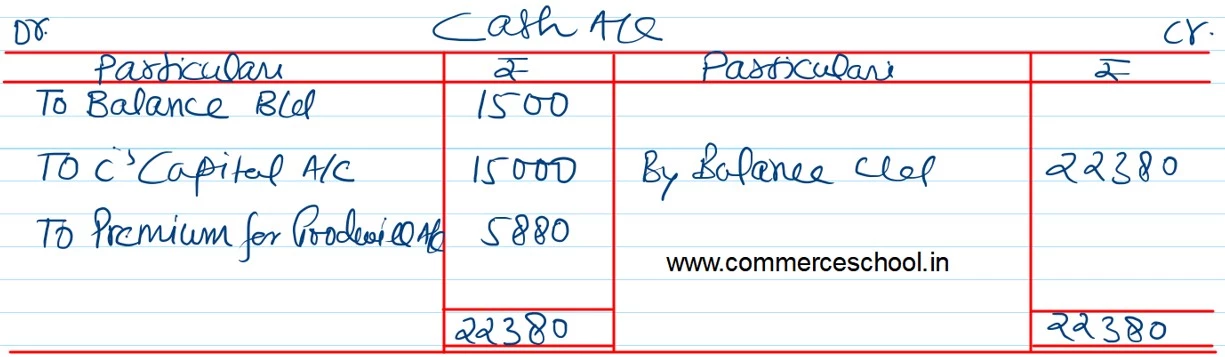

Cash

Stock Debtors Furniture Machinery Goodwill |

1,500 28,000 19,500 2,500 48,500 20,000 |

| 1,20,000 | 1,20,000 |

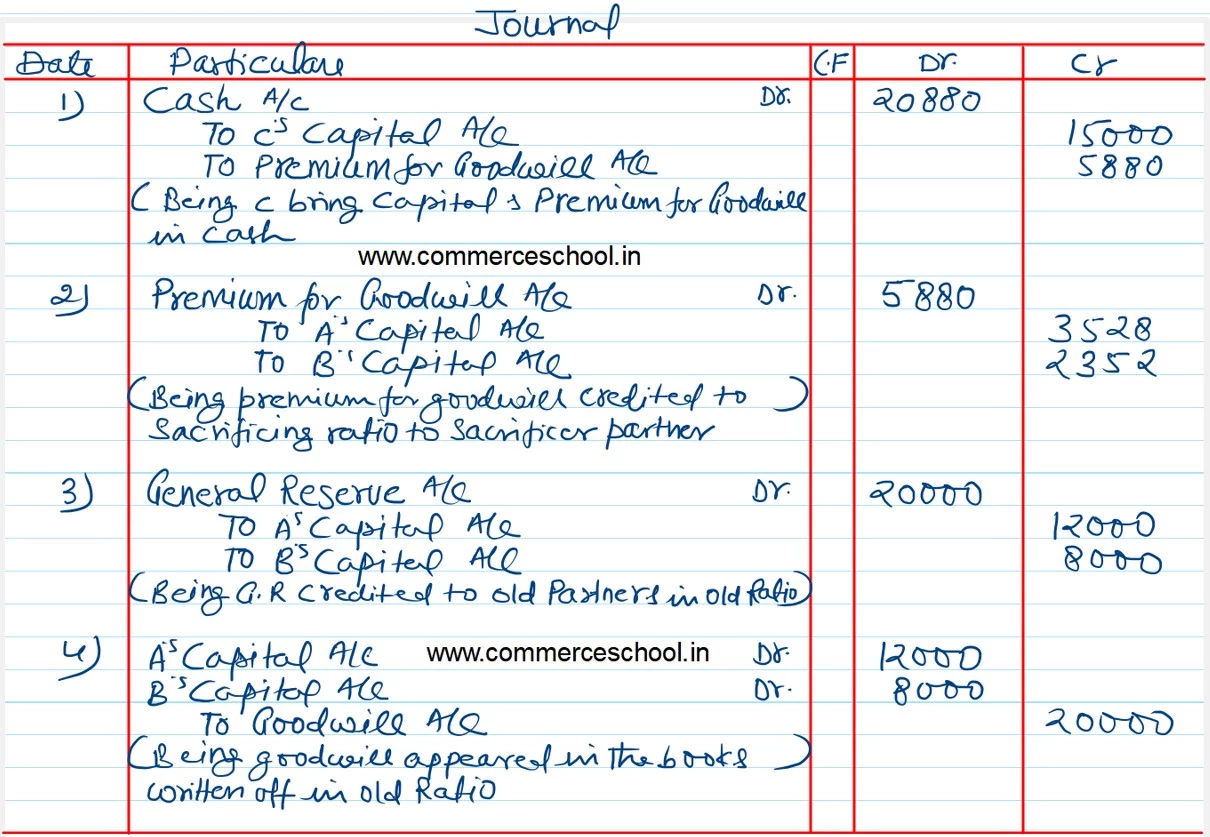

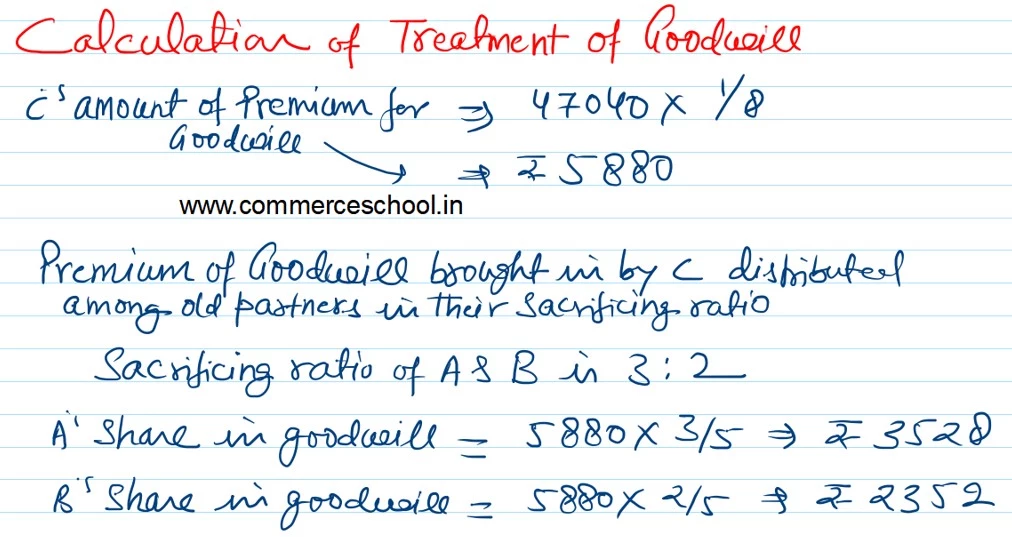

They admit C into partnership on 1st April, 2023 and give him 1/8th share in future profits on the following terms:

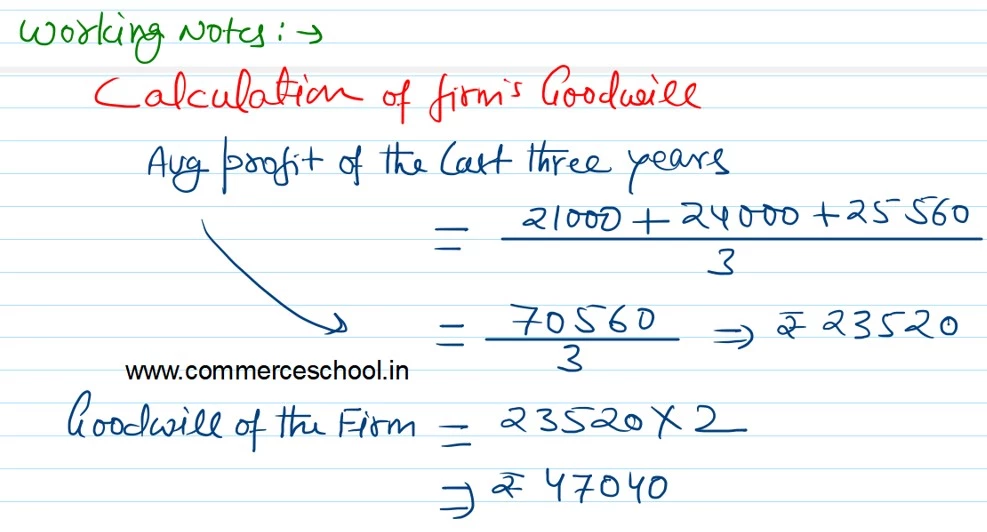

a) Goodwill of the firm be valued at twice the average of the last three year’s profits which amounted to ₹ 21,000; ₹ 24,000 and ₹ 25,560.

b) C is to bring cash for the amount of his share of goodwill.

c) C is to bring cash ₹ 15,000 as his capital.

Pass Journal entries recording these transactions, draw out the Balance Sheet of the new firm and determine new profit sharing ratio.

Anurag Pathak Changed status to publish