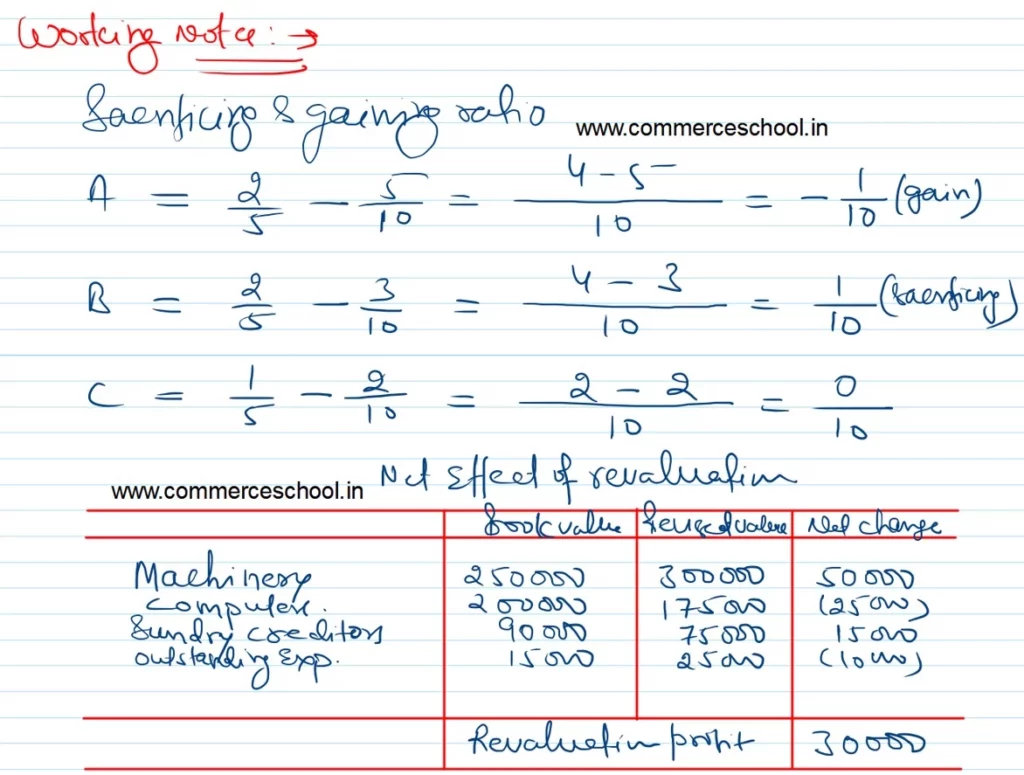

A, B and C are sharing profits and losses in the ratio of 2 : 2 : 1. They decided to share profit w.e.f 1st April, 2023 in the ratio of 5 ; 3 : 2. They also decided not to change the values of assets and liabilities in the books of account. The book values and revised values of asset and liabilities as on the date of change were as follows:

A, B and C are sharing profits and losses in the ratio of 2 : 2 : 1.

They decided to share profit w.e.f 1st April, 2023 in the ratio of 5 ; 3 : 2.

They also decided not to change the values of assets and liabilities in the books of account.

The book values and revised values of asset and liabilities as on the date of change were as follows:

| Book Values (₹) | Revised Values (₹) | |

| Machinery | 2,50,000 | 3,00,000 |

| Computers | 2,00,000 | 1,75,000 |

| Sundry Creditors | 90,000 | 75,000 |

| Outstanding Expenses | 15,000 | 25,000 |

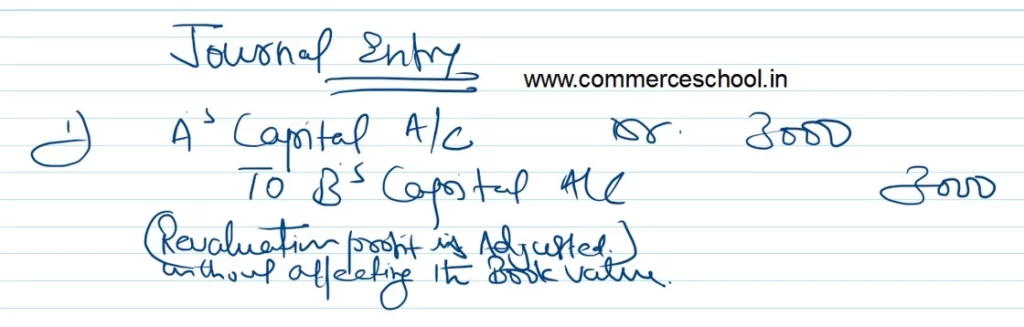

Pass an adjustment entry.

Anurag Pathak Changed status to publish