A, B and C sharing profits and losses in the ratio of 4 : 3 : 2, decide to share profits and losses in the ratio of 2 : 3 : 4 with effect from 1st April, 2024. Following is an extract of their Balance Sheet as at 31st March, 2024

A, B and C sharing profits and losses in the ratio of 4 : 3 : 2, decide to share profits and losses in the ratio of 2 : 3 : 4 with effect from 1st April, 2024. Following is an extract of their Balance Sheet as at 31st March, 2024 :

Show the accounting treatment under the following alternative cases:

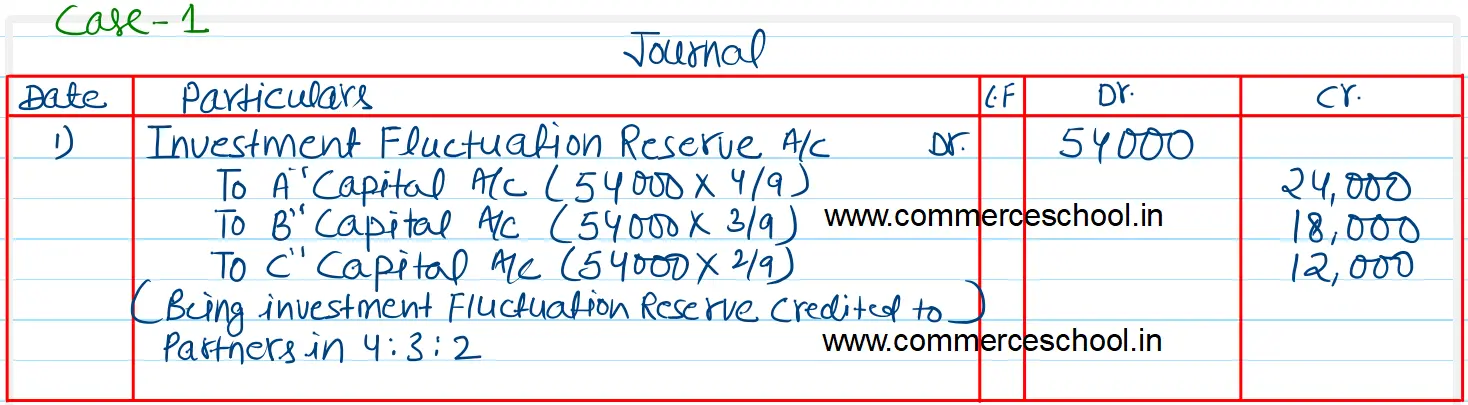

Case (i) If there is no other information.

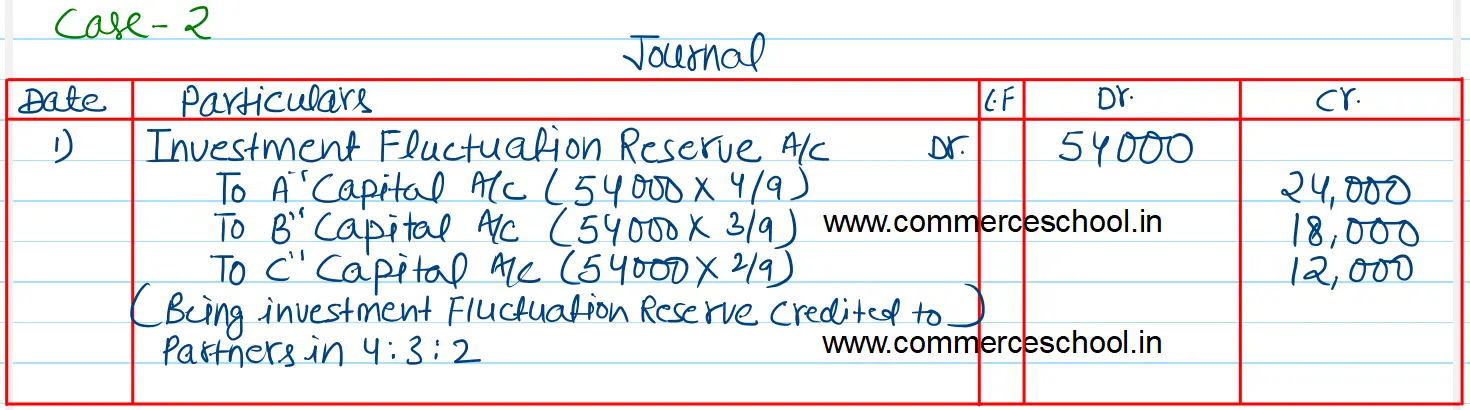

Case (ii) If the market value of Investments is ₹ 6,00,000.

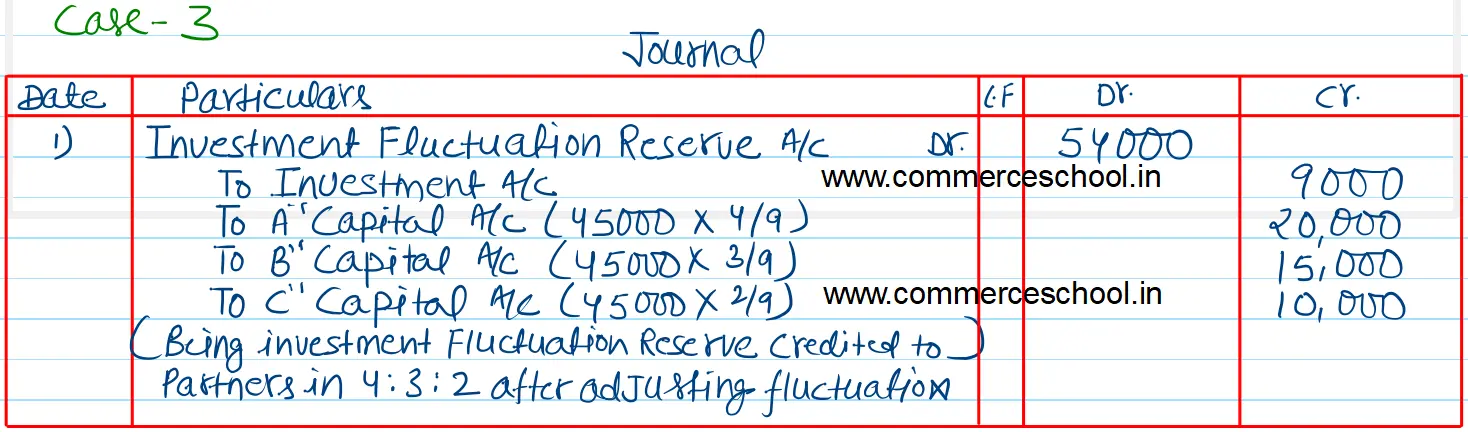

Case (iii) If the market value of Investments is ₹ 5,91,000.

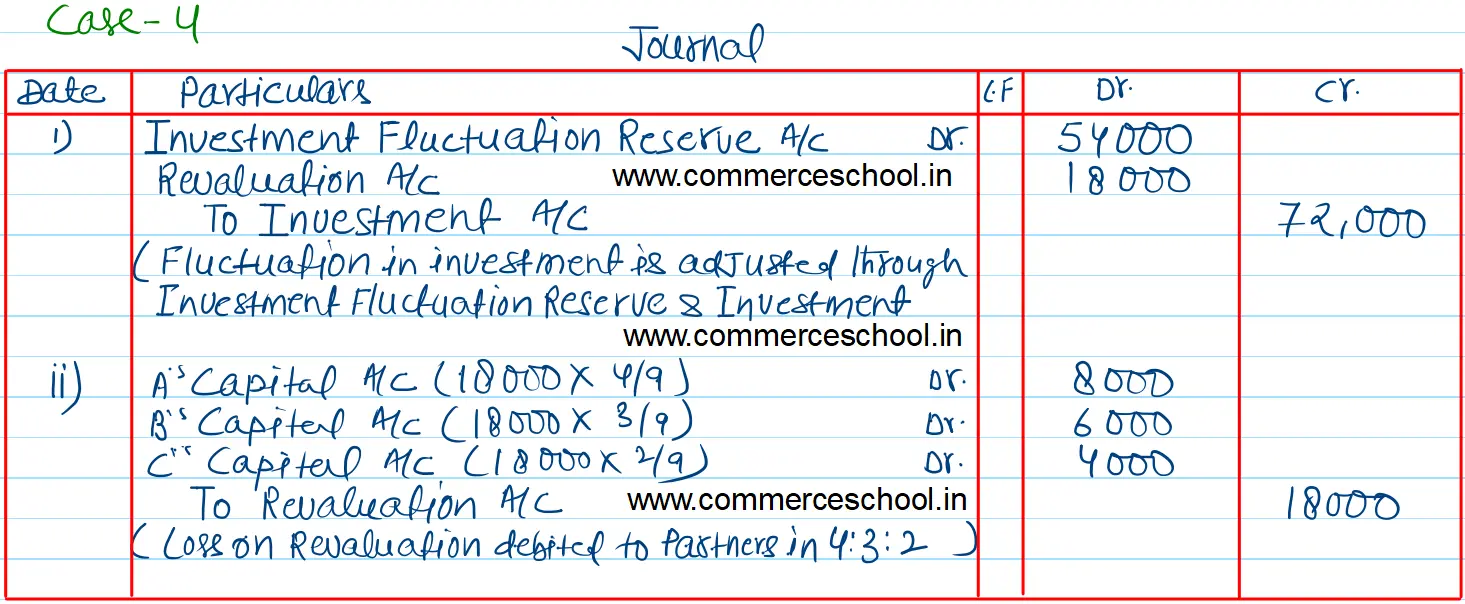

Case (iv) If the market value of Investments is ₹ 5,28,000.

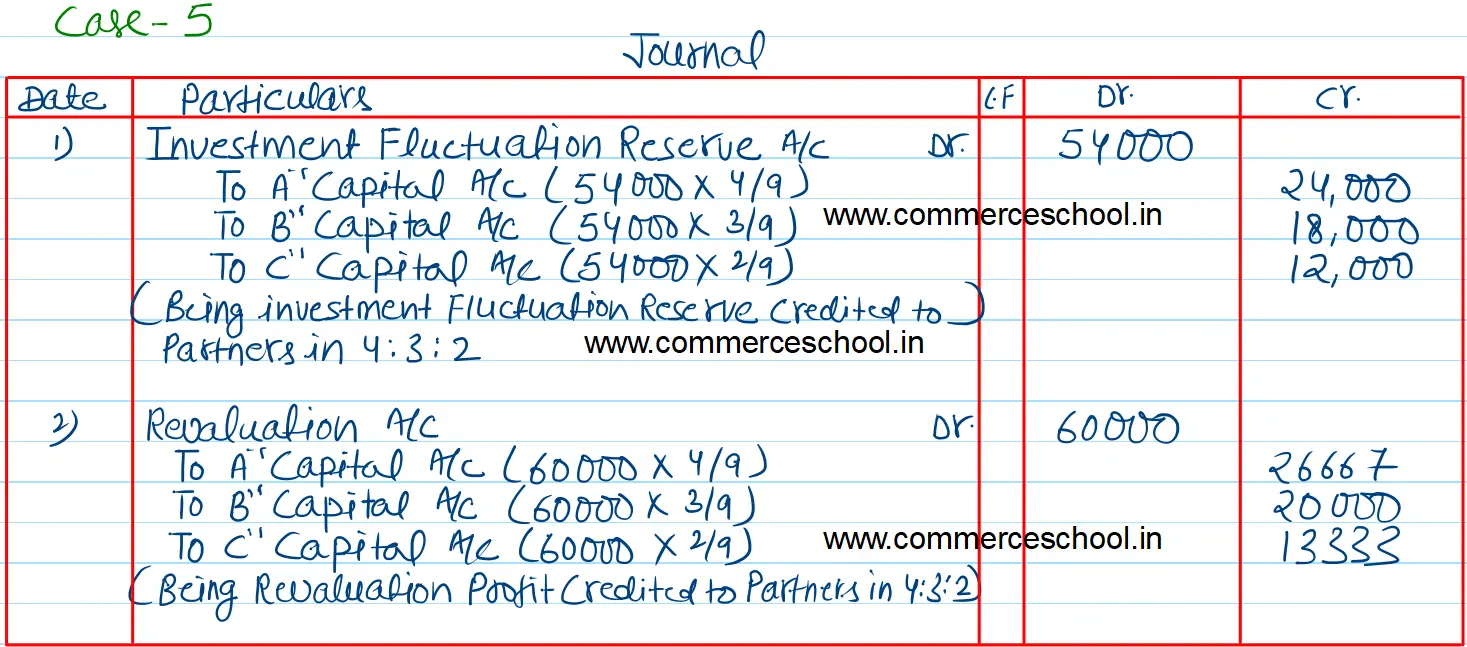

Case (v) If the market value of Investments is ₹ 6,60,000.

| Liabilities | ₹ | Assets | ₹ |

| Investment Fluctuation Reserve | 54,000 | Investment (at cost) | 6,00,000 |

Anurag Pathak Answered question

Solution:-

In the absence of no fluctuation in Investment, the investment fluctuation reserve is credited to partners in old ratio.

In the absence of no fluctuation in Investment, the investment fluctuation reserve is credited to partners in old ratio.

The remaining Investment Fluctuation Reserve is credited to partners in the old ratio after adjusting the fluctuation in investment.

The fluctuation in investment is adjusted through the investment fluctuation reserve and revaluation account and loss on revaluation is debited to the partners in the old ratio.

When the value of the investment is rising, the whole investment fluctuation reserve is credited to the partners in the old ratio. and the rise in investment is transferred to the revaluation account.

Anurag Pathak Answered question