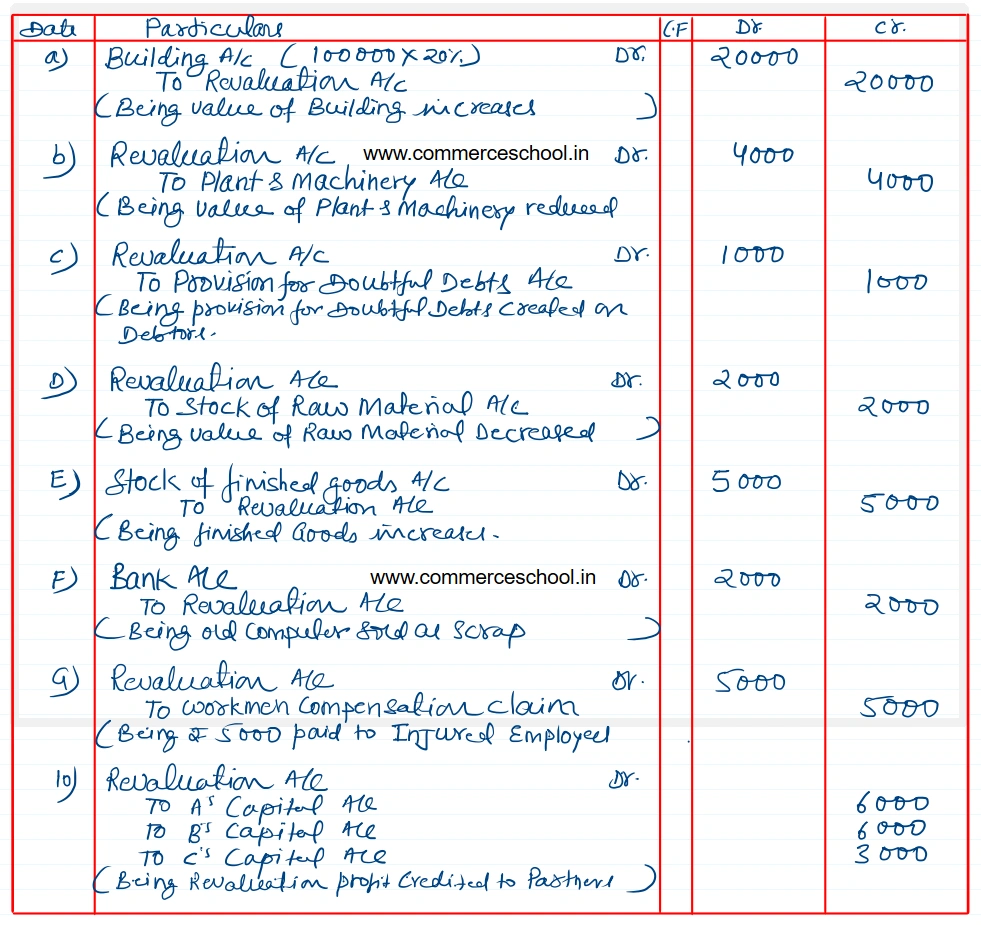

A, B and C were partners, sharing profits and losses in the ratio of 2 : 2 : 1. B retired on 31st March, 2023. on the date of his retirement, some of the assets and liabilities appeared in the books as follows: Creditors ₹ 70,000; Building ₹ 1,00,000; Plant and Machinery ₹ 40,000; Stock of Raw Materials ₹ 20,000; Stock of Finished Goods ₹ 30,000 and Debtors ₹ 20,000.

A, B and C were partners, sharing profits and losses in the ratio of 2 : 2 : 1. B retired on 31st March, 2023. on the date of his retirement, some of the assets and liabilities appeared in the books as follows:

Creditors ₹ 70,000; Building ₹ 1,00,000; Plant and Machinery ₹ 40,000; Stock of Raw Materials ₹ 20,000; Stock of Finished Goods ₹ 30,000 and Debtors ₹ 20,000.

Following was agreed among the partners on B’s retirement:

a) Building to be appreciated by 20%

b) Plant and Machinery to be reduced by 10%.

c) A Provision of 5% on Debtors to be created for Doubtful Debts.

d) Stock of Raw Materials to be valued at ₹ 18,000 and Finished Goods at ₹ 35,000.

e) An old Computer previously written off was sold for ₹ 2,000 as scrap.

f) Firm had to pay ₹ 5,000 to an injured employee.

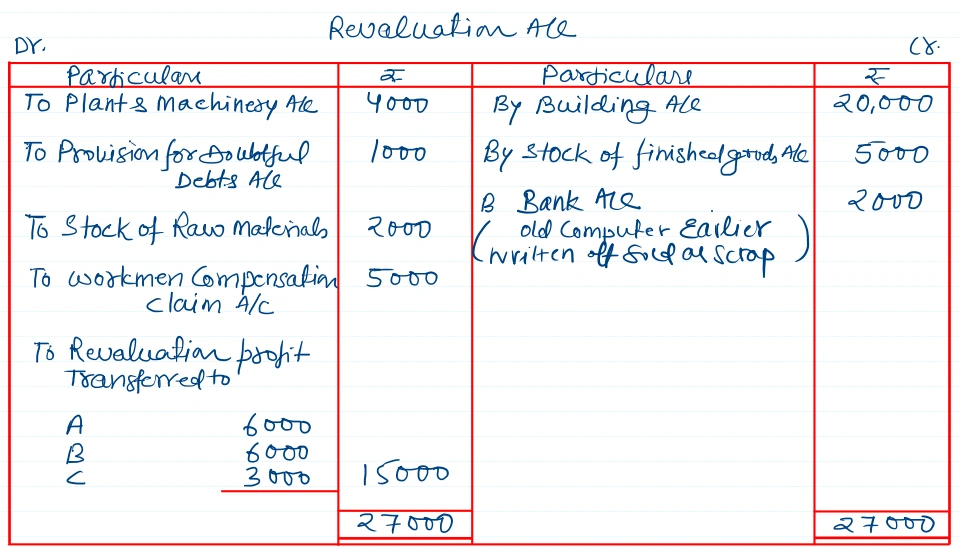

Pass necessary Journal entries to record the above adjustments and prepare the Revaluation Account.

Anurag Pathak Changed status to publish