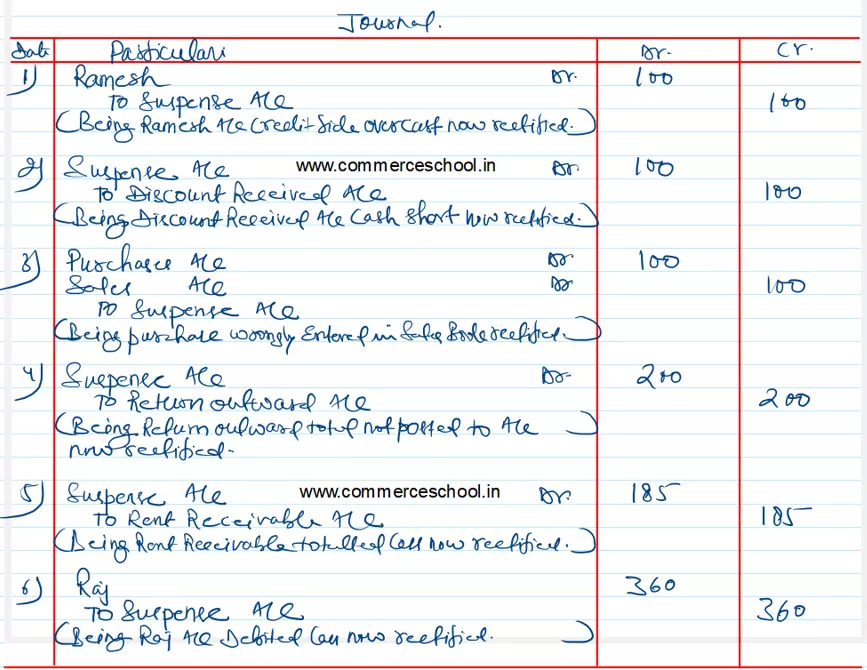

A book keeper failed to balance his Trial Balance, the credit side exceeding the debit side by ₹ 175. This amount was entered in a Suspense Account

A book keeper failed to balance his Trial Balance, the credit side exceeding the debit side by ₹ 175. This amount was entered in a Suspense Account. Later, the following errors were discovered:

(i) Total of the credit side of Ramesh account was overcast by ₹ 100.

(ii) Discount Received Account had been cast short by ₹ 100.

(iii) Goods worth ₹ 100 purchased from Chandra were wrongly entered in the Sales Book. The account of Chandra was correctly credited.

(iv) Total of the Returns Outward Book amounting to ₹ 200 was not posted to the Ledger.

(v) A credit balance of ₹ 755 of the Rent Receivable Account was shown as ₹ 570.

(vi) Goods worth ₹ 620 sold to Raj were correctly entered in the Sales Book but posted to Raj’s Account as ₹ 260.

Anurag Pathak Changed status to publish