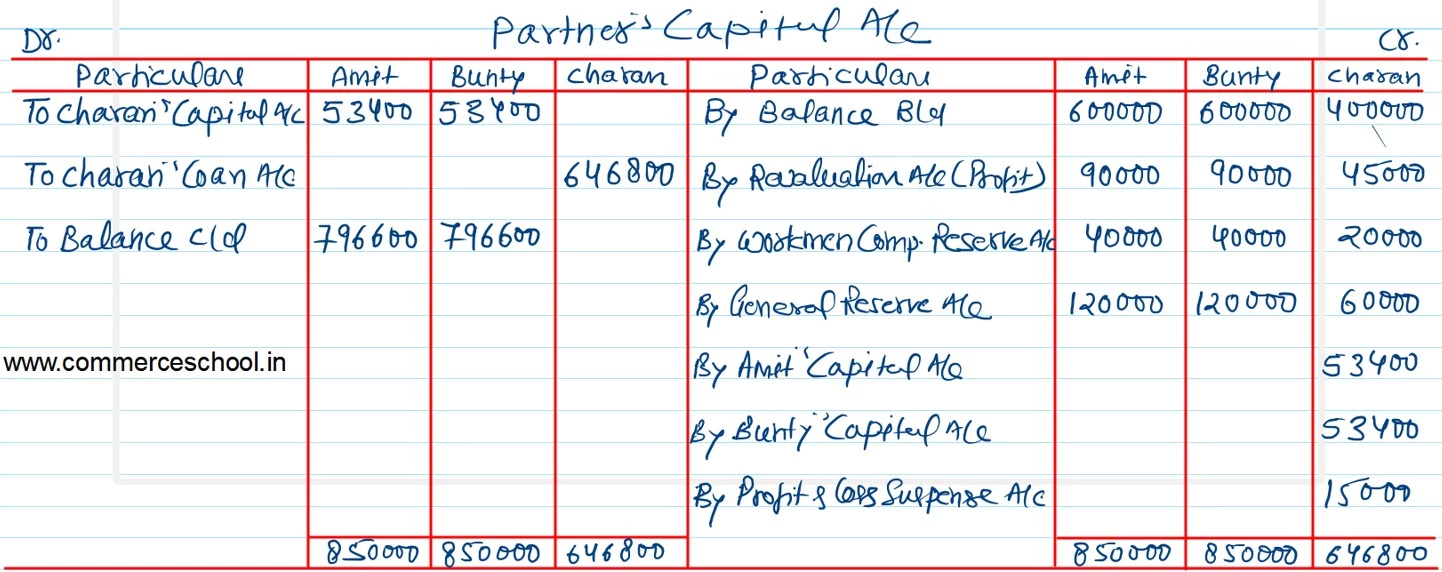

Amit, Bunty and Charan are partners sharing profits and losses in the ratio of 2 : 2 : 1. Charan retired on 30th June, 2023. The Balance Sheet of the firm on 31st March, 2023 was as follows:

Amit, Bunty and Charan are partners sharing profits and losses in the ratio of 2 : 2 : 1. Charan retired on 30th June, 2023. The Balance Sheet of the firm on 31st March, 2023 was as follows:

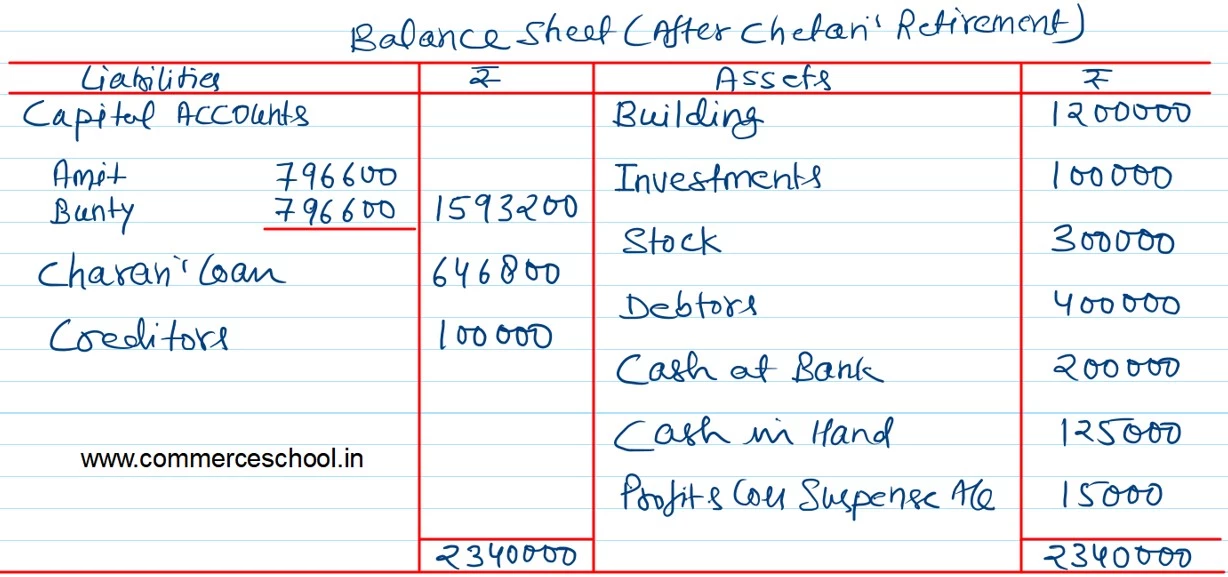

| Liabilities | ₹ | Assets | ₹ |

| Capital Accounts:

Amit Bunty Charan Employee’s Compensation Reserve General Reserve Creditors |

6,00,000

6,00,000 4,00,000 1,00,000 3,00,000 1,00,000 |

Building

Investments Stock Debtors Cash at bank Cash in Hand |

10,00,000

1,25,000 2,50,000 4,00,000 2,00,000 1,25,000 |

| 21,00,000 | 21,00,000 |

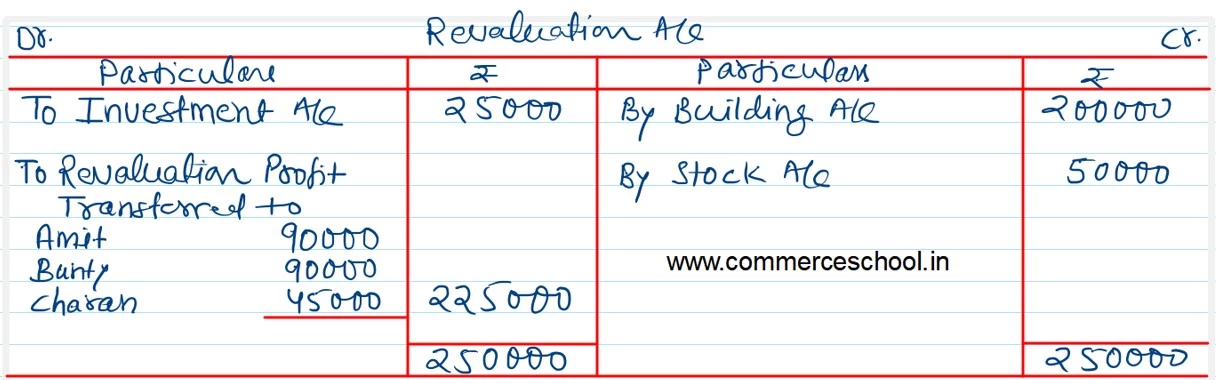

It was agreed that amount payable to Charan will be determined by making following adjustments:

a) Building be valued at ₹ 12,00,000.

b) Investment be valued at ₹ 1,00,000.

c) Stock to be valued at ₹ 3,00,000.

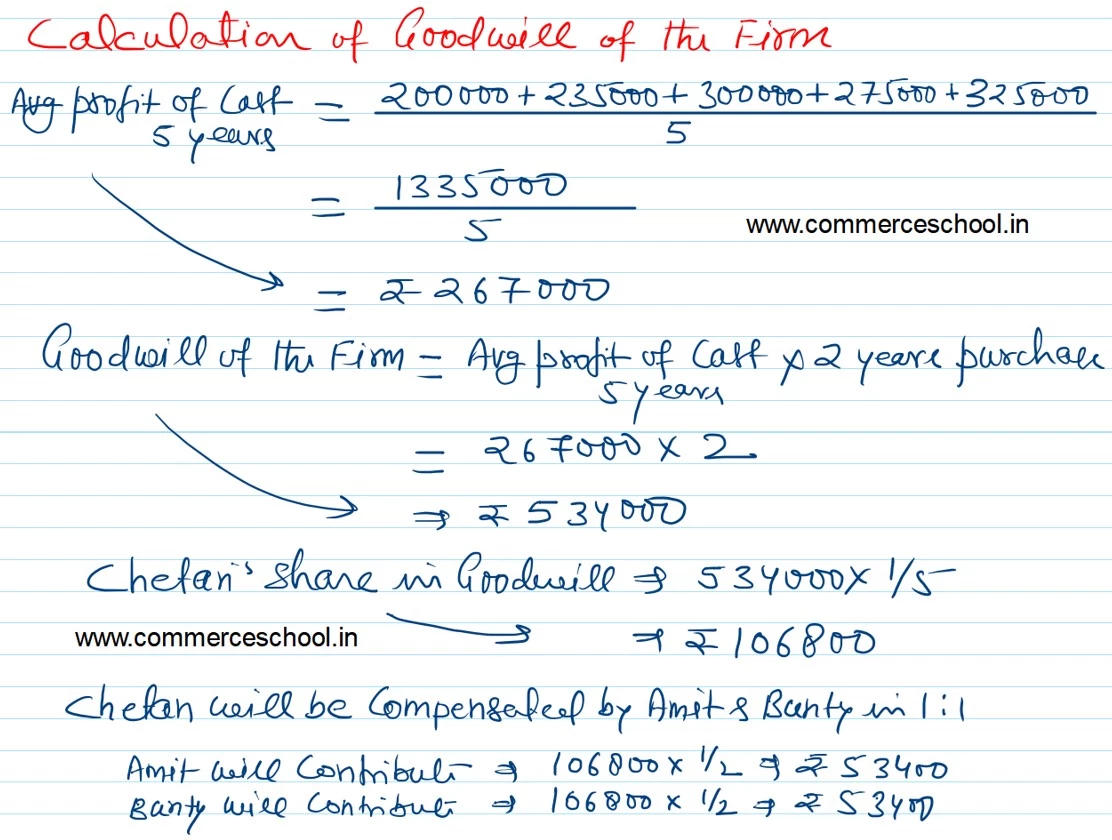

d) Goodwill of the firm be valued at 2 year’s purchase of average profit of last 5 years.

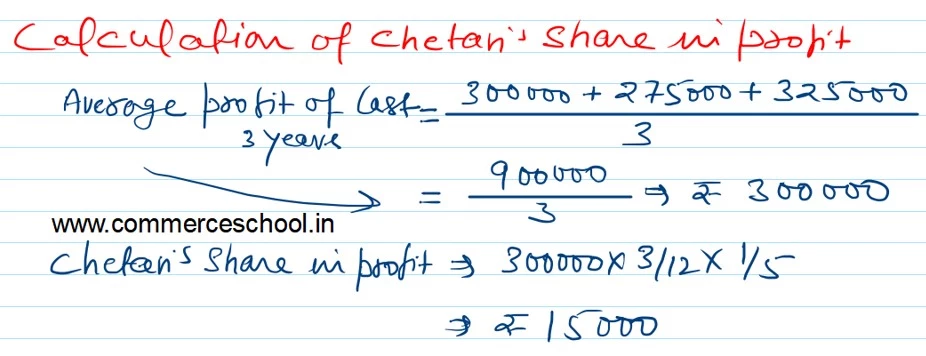

e) Charan’s share of profit up to the date of retirement be calculated on the basis of average profit of the preceding three years

Profits of the preceding five years were as under:

| Year’s | 2018 – 19 (₹) | 2019 – 20 (₹) | 2020 – 21 (₹) | 2021 – 22 (₹) | 2022 – 23 (₹) |

| Profit | 2,00,000 | 2,35,000 | 3,00,000 | 2,75,000 | 3,25,000 |

Prepare: i) Revaluation Account, ii) Partner’s Capital Accounts and iii) Balance Sheet after Charan’s retirement.

[Ans.: Profit on Revaluation = ₹ 2,25,000; Partner’s Capital Accounts: Amit = ₹ 7,96,600; Bunty = ₹ 7,96,600; Charan’s Loan A/c = ₹ 6,46,80; Total of Balance Sheet = ₹ 23,40,000.]

Anurag Pathak Changed status to publish