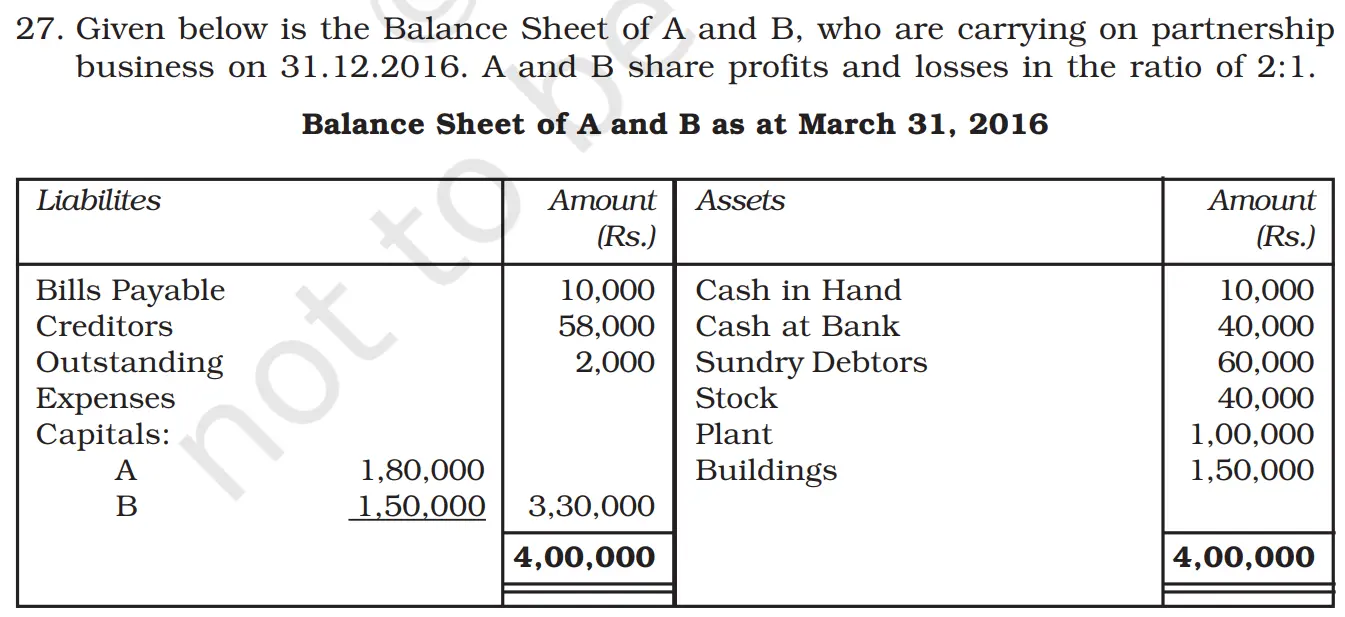

Given below is the Balance Sheet of A and B, who are carrying on partnership business on 31.12.2016. A and B share profits and losses in the ratio of 2 : 1

Given below is the Balance Sheet of A and B, who are carrying on partnership business on 31.12.2016. A and B share profits and losses in the ratio of 2 : 1.

Balance Sheet of A and B as at March 31, 2016

| Liabilities | ₹ | Assets | ₹ |

| Bills Payable | 10,000 | Cash in Hand | 10,000 |

| Creditors | 58,000 | Cash at Bank | 40,000 |

| Outstanding Expenses | 2,000 | Sundry Debtors | 60,000 |

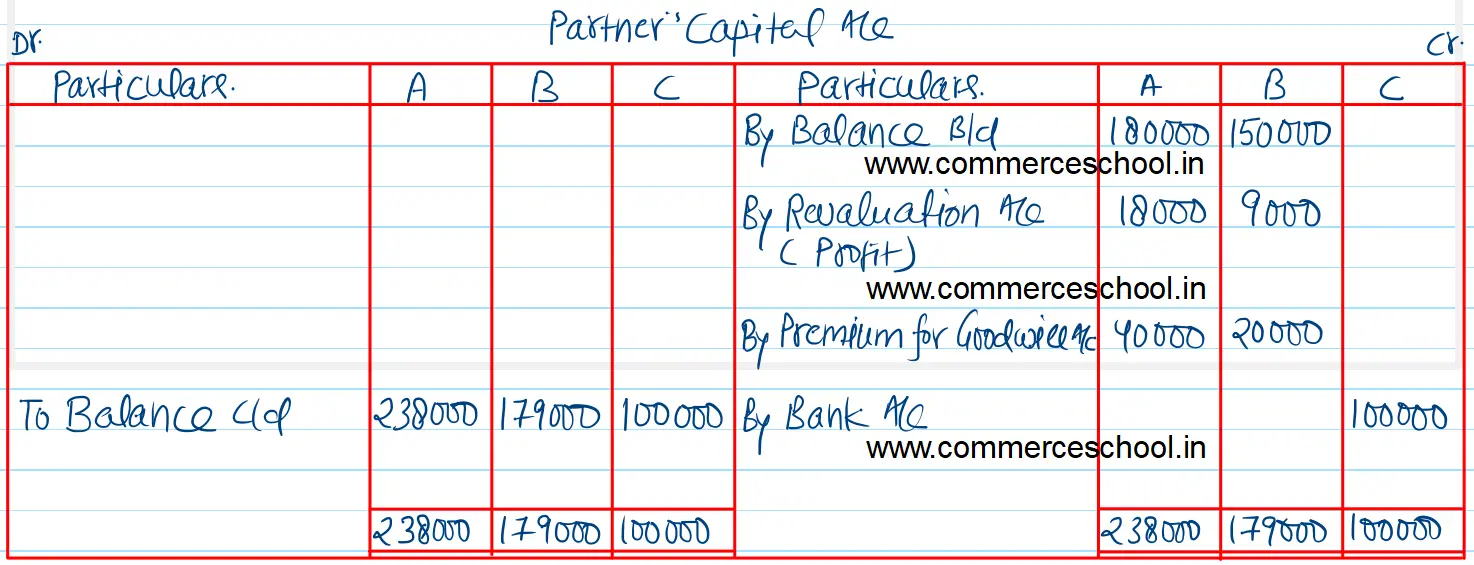

| Capitals: A B | 1,80,000 1,50,000 | Stock | 40,000 |

| Plant | 1,00,000 | ||

| Buildings | 1,50,000 | ||

| 4,00,000 | 4,00,000 |

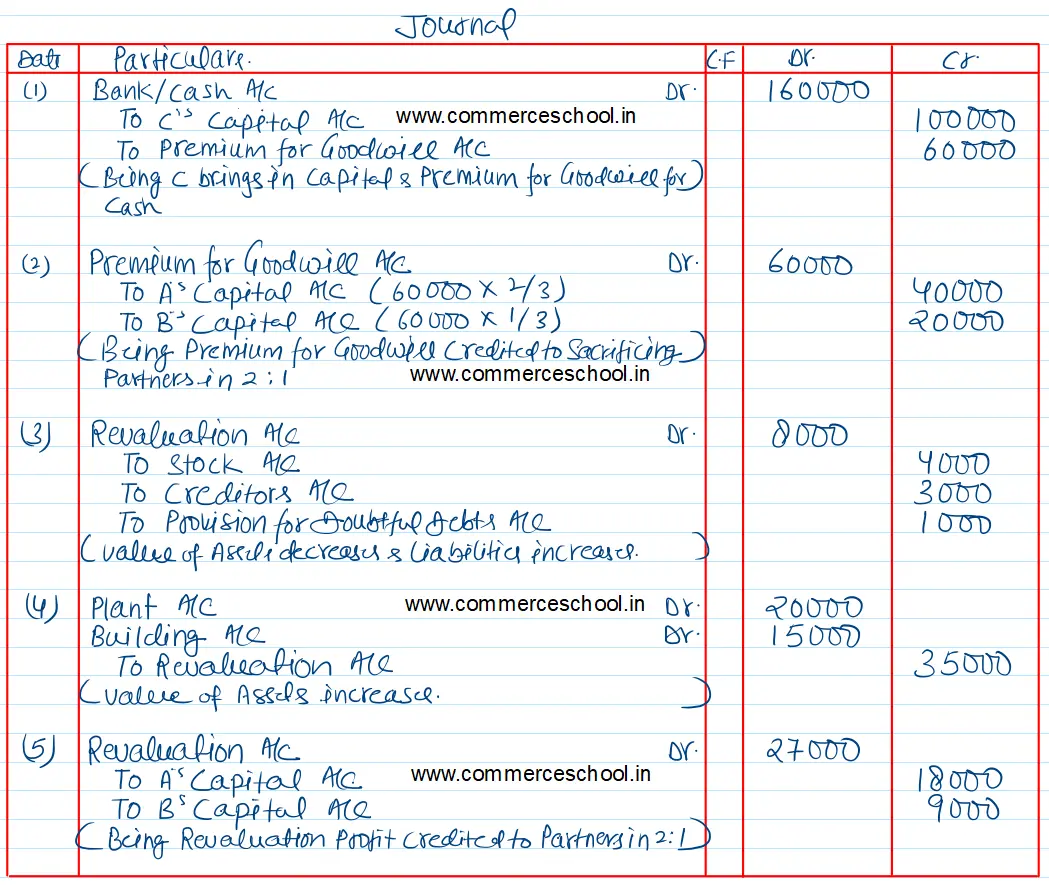

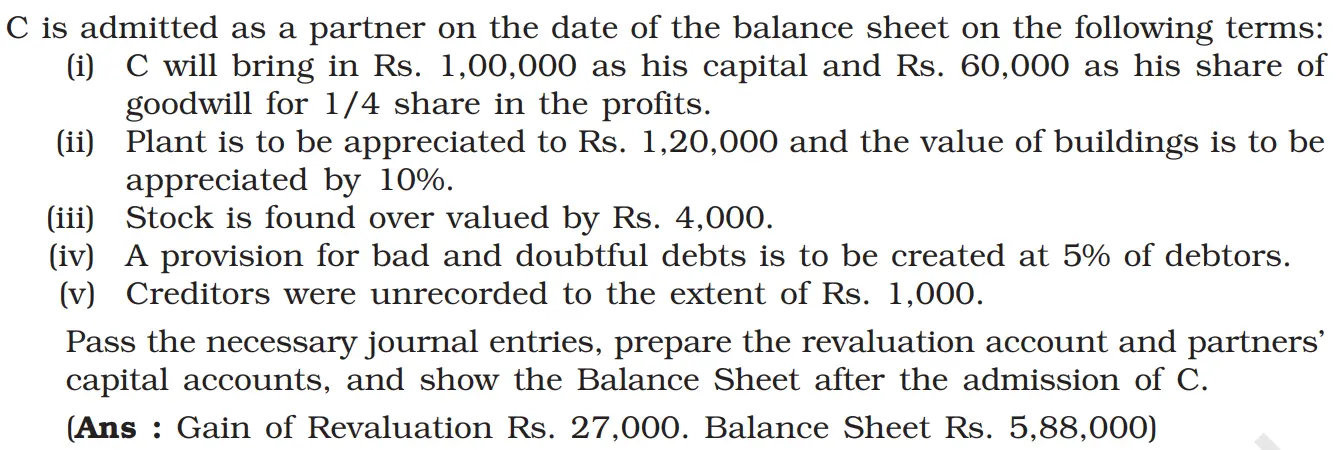

C is admitted as a partner on the date of the balance sheet on the following terms:

(I) C will bring in Rs. 1,00,000 as his capital and Rs. 60,000 as his share of goodwill for 1/4 share in the profits.

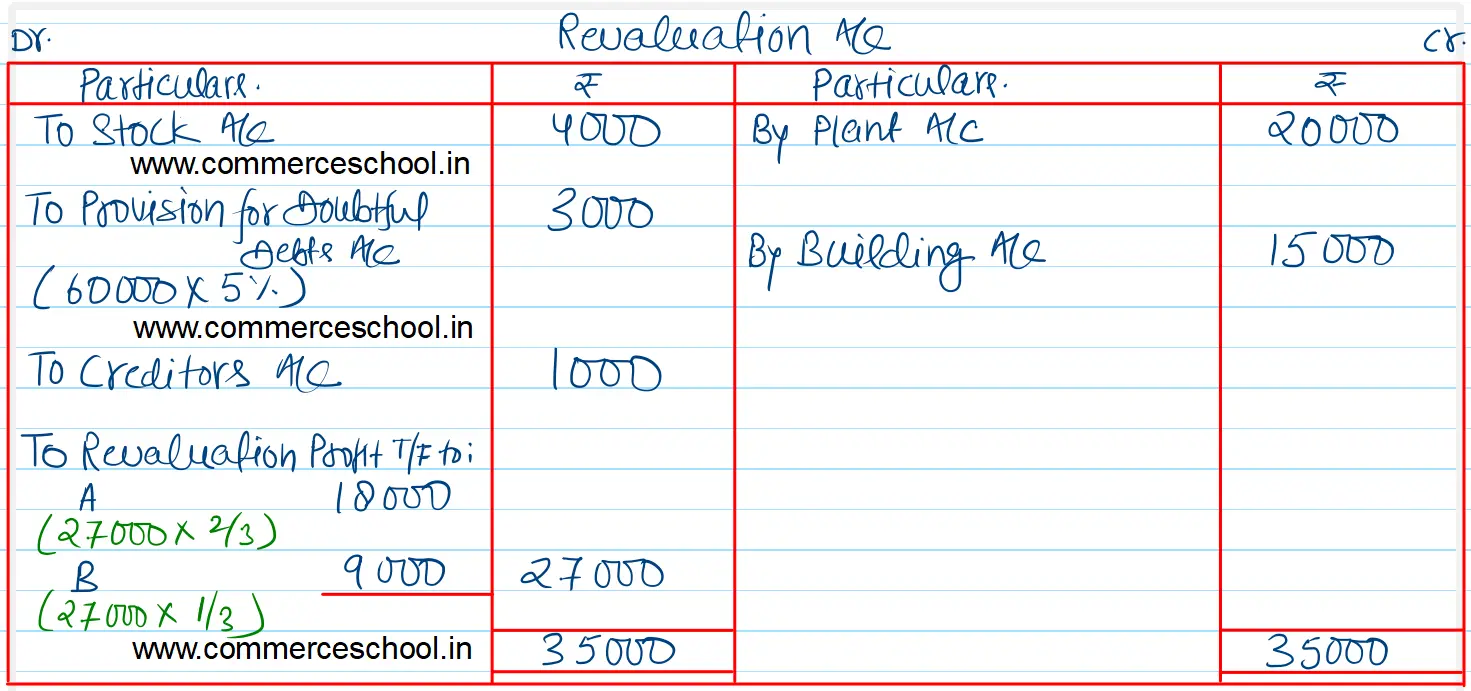

(ii) Plant is to be appreciated to Rs. 1,20,000 and the value of buildings is to be appreciated by 10%.

(iii) Stock is found over valued by Rs. 4,000.

(iv) A provision for bad and doubtful debts is to be created at 5% of debtors.

(v) Creditors were unrecorded to the extent of Rs. 1,000.

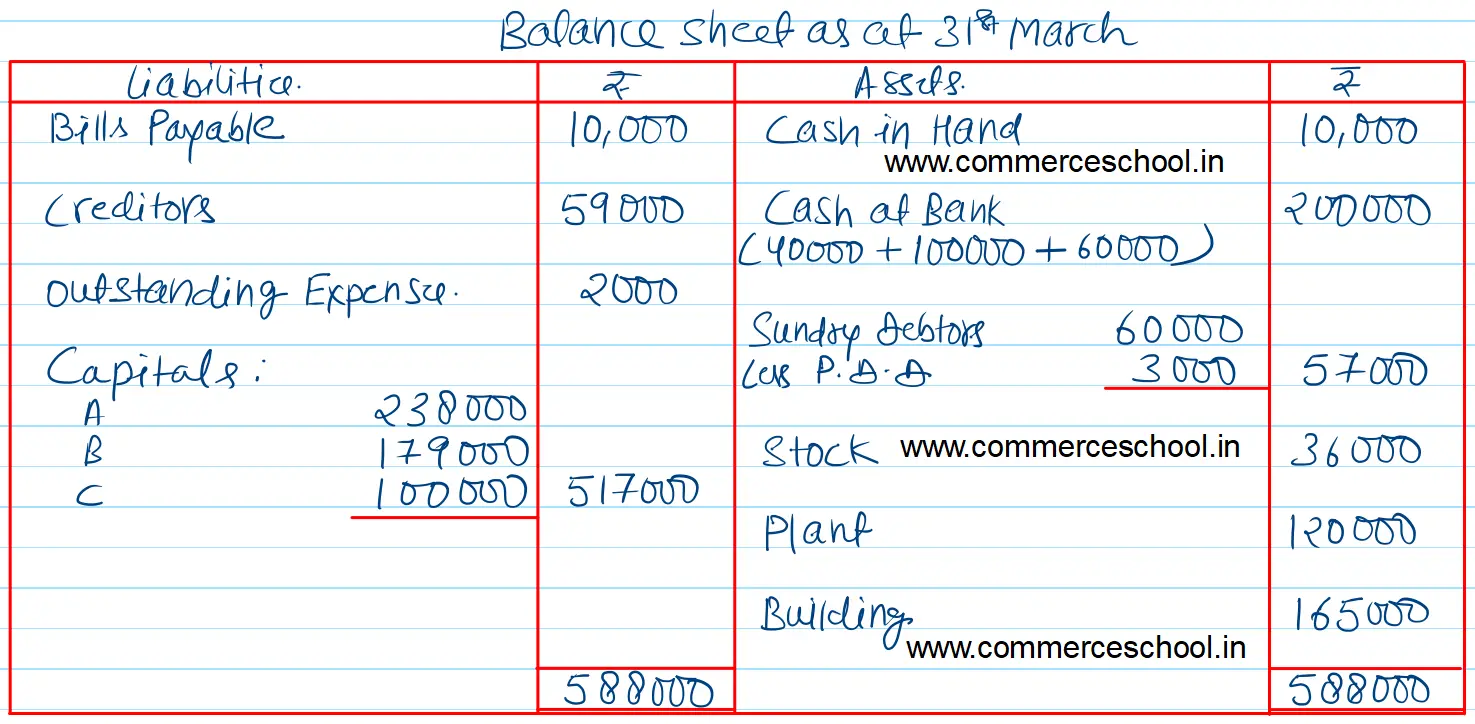

Pass the necessary journal entries, prepare the revaluation account and partner’s capital accounts, and show the Balance Sheet after the admission of C.

[Ans : Gain of Revaluation Rs. 27,000. Balance Sheet Rs. 5,88,000)

Anurag Pathak Changed status to publish