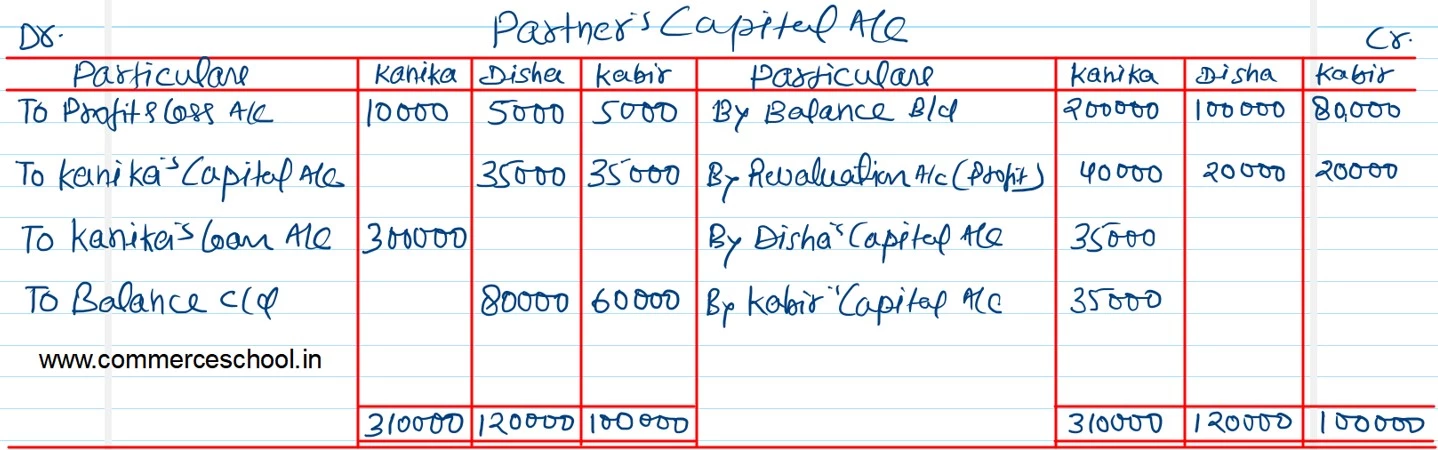

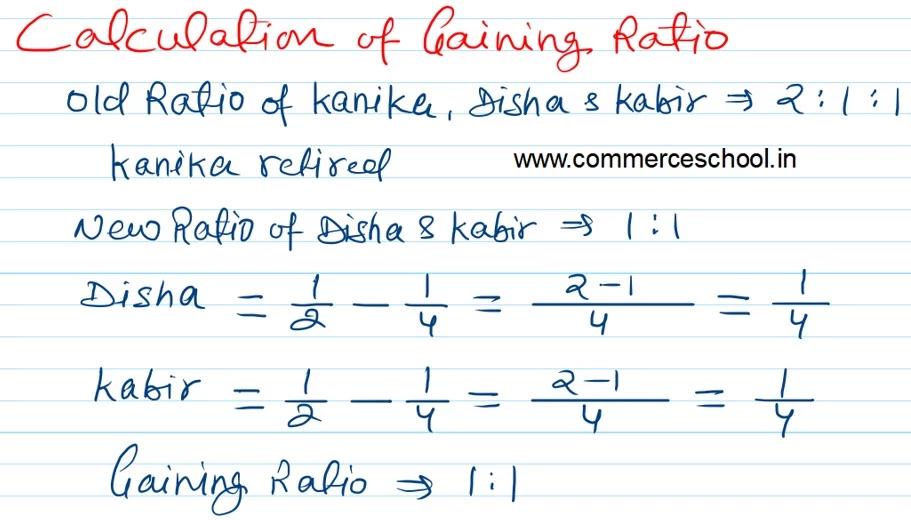

Kanika, Disha and Kabir were partners sharing profits in the ratio of 2 : 1 : 1. On 31st March, 2016, their Balance Sheet was as under:

Kanika, Disha and Kabir were partners sharing profits in the ratio of 2 : 1 : 1. On 31st March, 2016, their Balance Sheet was as under:

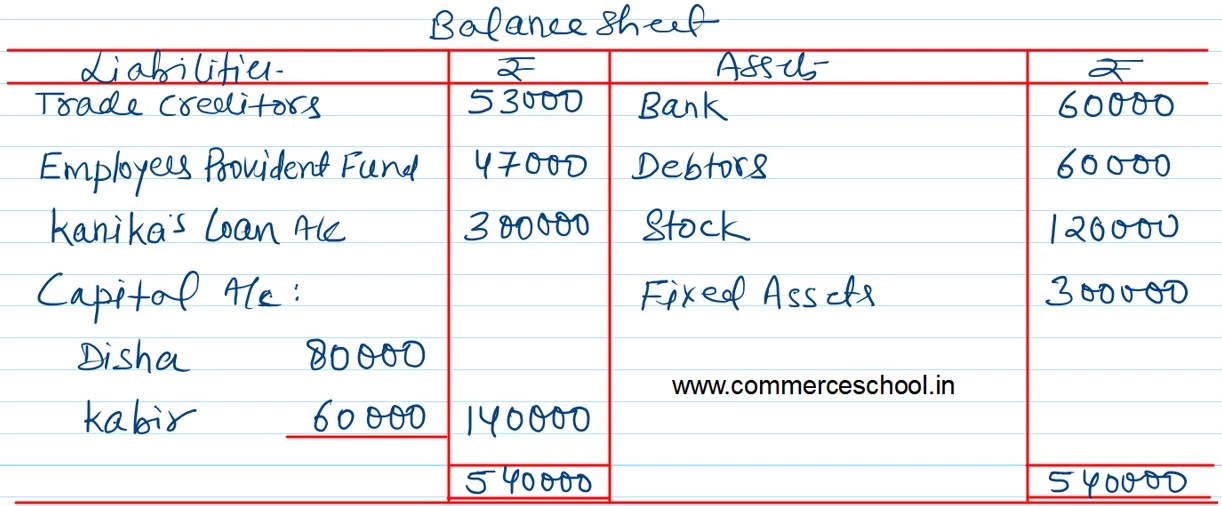

| Liabilities | ₹ | Assets | ₹ |

| Trade Creditors

Employee’s Provident Fund Kanika’s Capital Disha’s Capital Kabir’s Capital |

53,000 47,000 2,00,000 1,00,000 80,000 |

Bank

Debtors Stock Fixed Assets Profit & Loss A/c |

60,000 60,000 1,00,000 2,40,000 20,000 |

| 4,80,000 | 4,80,000 |

Kanika retired on 1st April, 2016. For this purpose, the following adjustments were agreed upon:

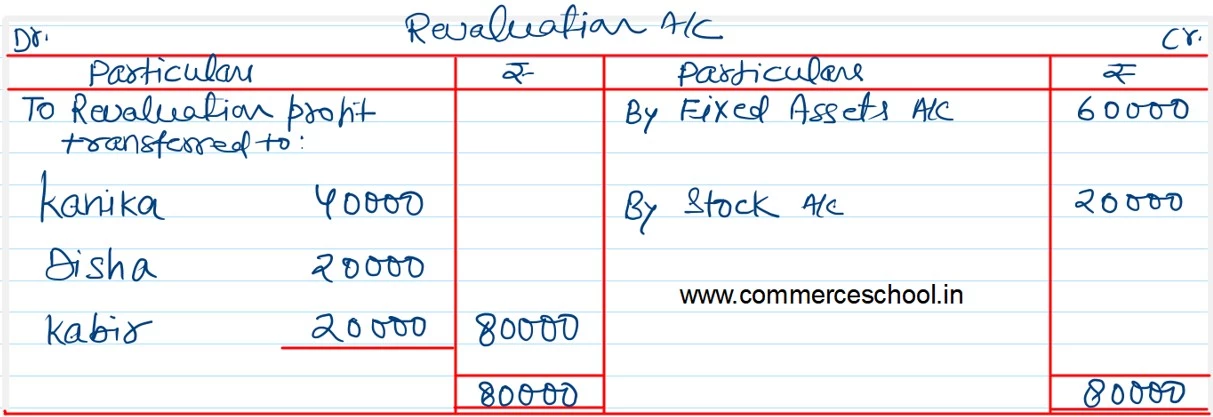

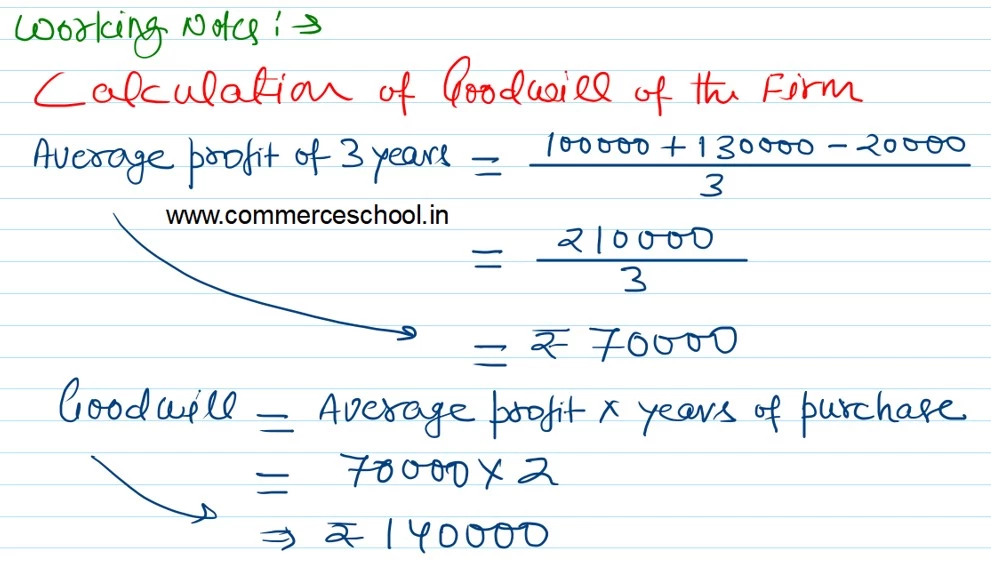

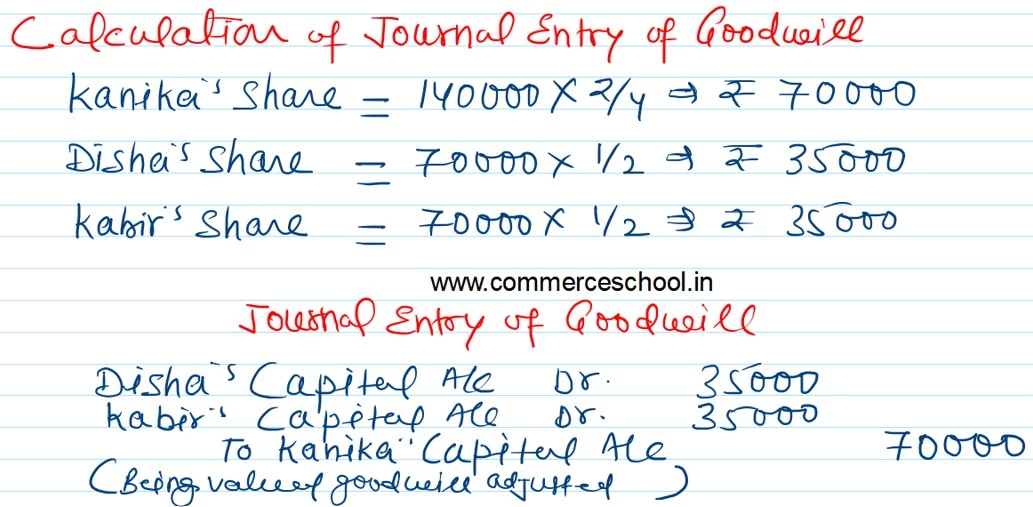

a) Goodwill of the firm was valued at 2 year’s purchase of average profits of three completed years preceding the date of retirement. The profits for the year: 2013 – 14 were ₹ 1,00,000 and for 2014 – 15 were ₹ 1,30,000.

b) Fixed Assets were to be increased to ₹ 3,00,000.

c) Stock was to be valued at 120%.

d) The amount payable to Kanika was transferred to her Loan Account.

Prepare Revaluation Account, Capital Accounts of the partners and the Balance Sheet of the reconstituted firm.

Anurag Pathak Changed status to publish