L, M and N were partners sharing profits and losses in the ratio of 5 : 3 : 2. Their Balance Sheet as at 1.4.2022 was as under:

Liabilities

₹

Assets

₹

Sundry Creditors

20,000

Cash at Bank

28,000

Reserves

9,000

Debtors

22,000

Capitals:

L

M

N

50,000

30,000

20,000

Stock

20,000

Machinery

47,000

Investments

12,000

1,29,000

1,29,000

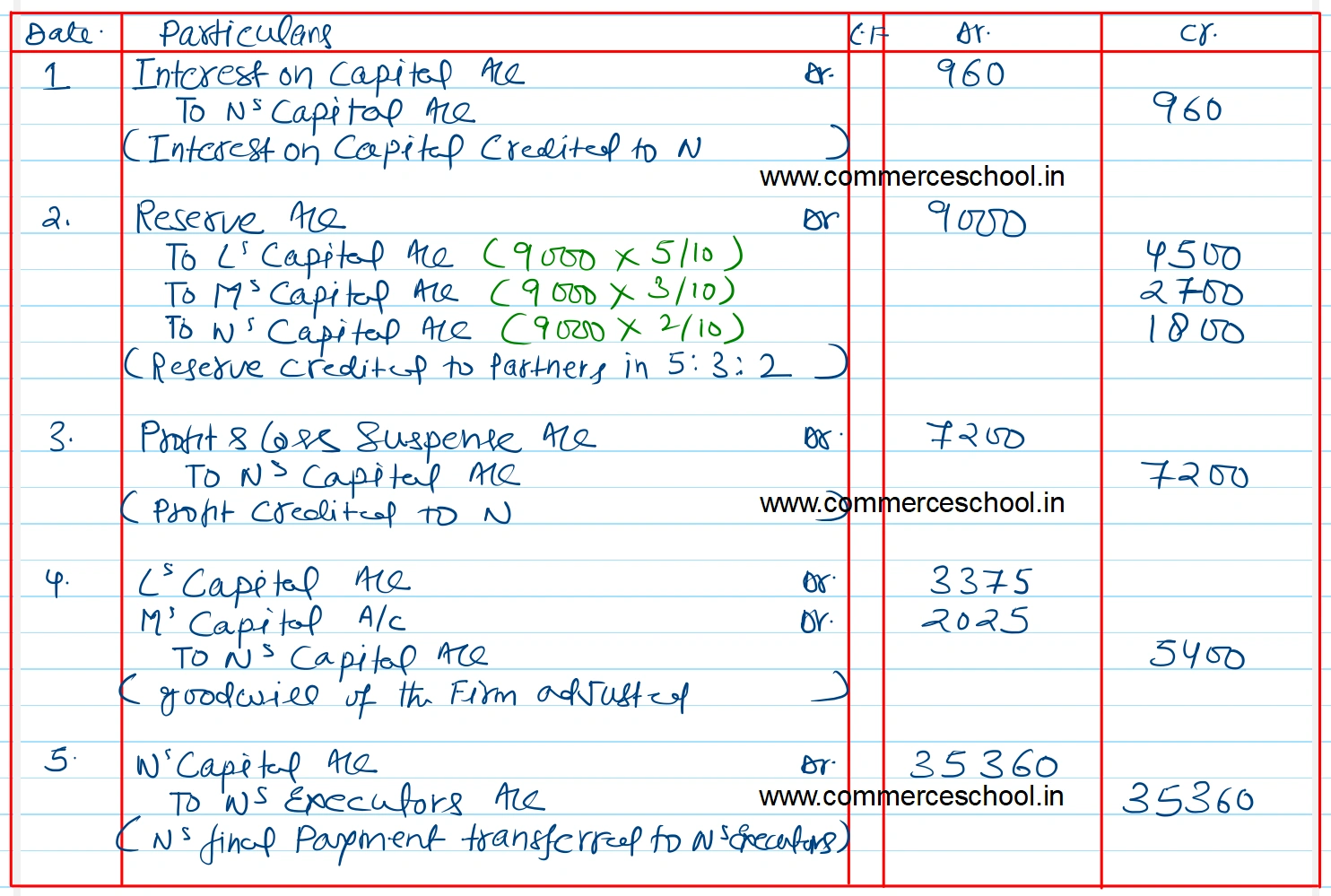

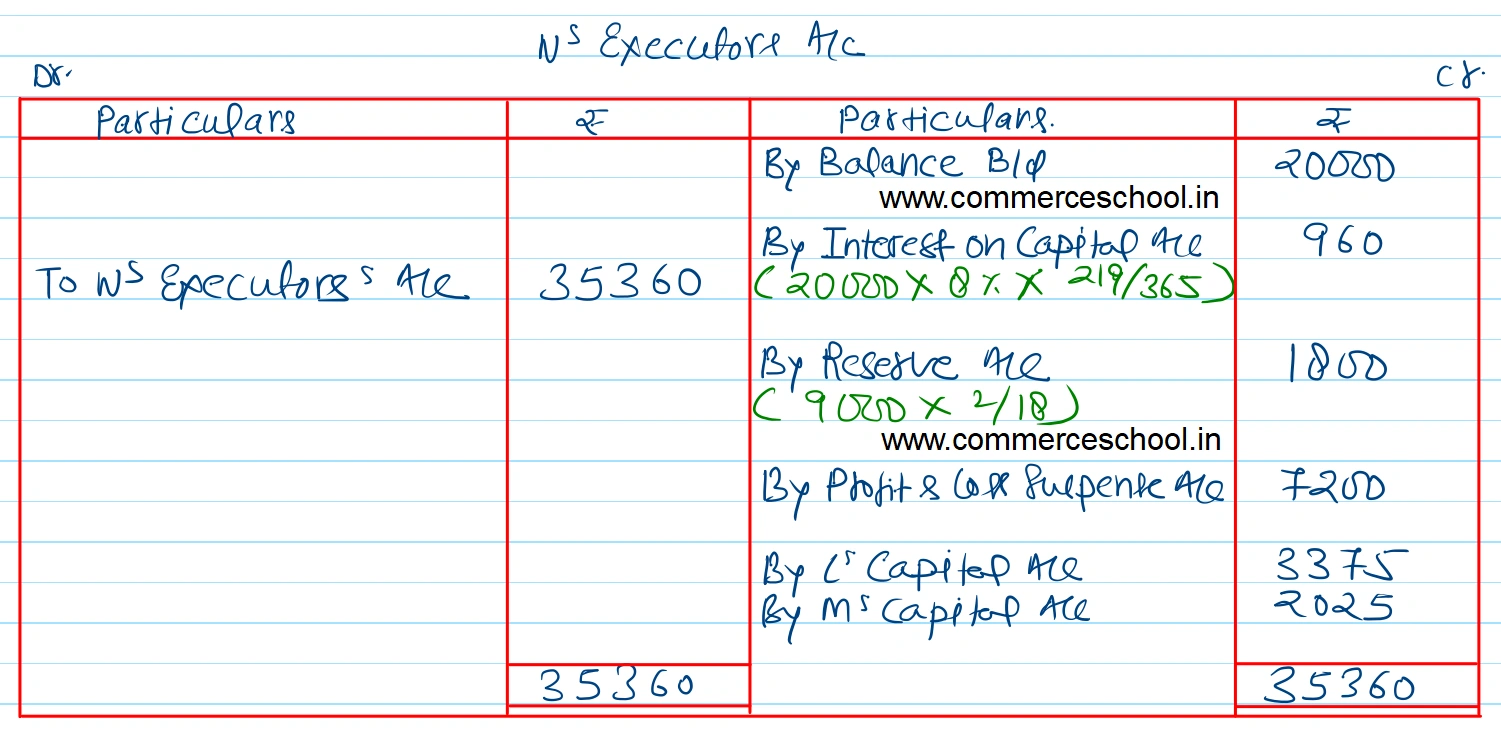

N died on 5th November, 2022 and according to the partnership deed his executors were entitled to be paid as under:

(a) The capital to his credit at the time of his death and interest thereon @ 8% per annum.

(b) His share of Reserves.

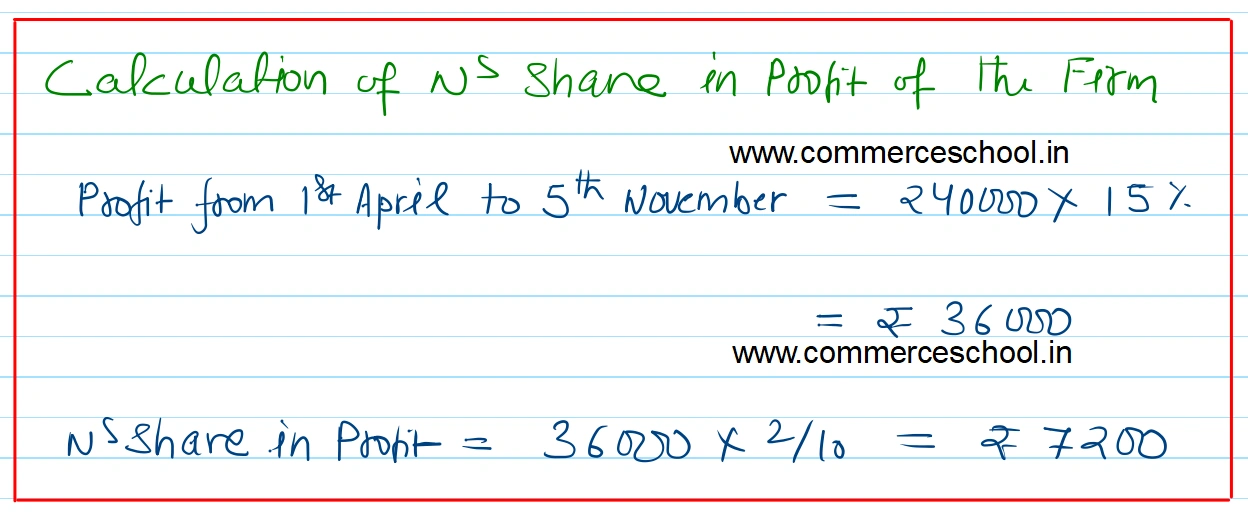

(c) His share of profits for the intervening period will be based on the sales during that period, which were calculated as ₹ 2,40,000. The rate of profit during past 4 years had been 15% on sales.

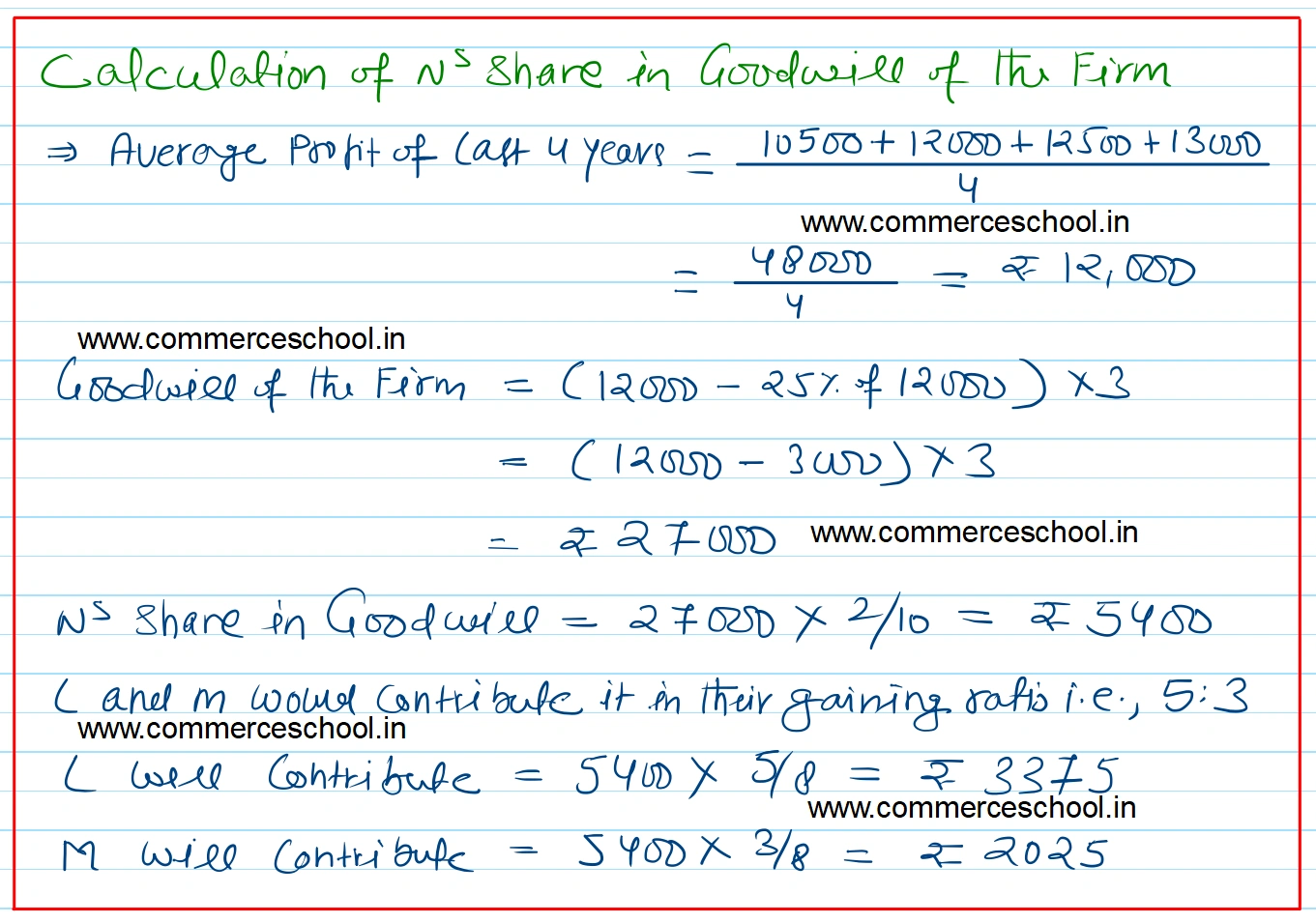

(d) Goodwill according to his share of profit to be calculated by taking thrice the amount of the average profit of the last four years less 25%. The profits of the previous years were:

2019

₹ 10,500

2020

₹ 12,000

2021

₹ 12,500

2022

₹ 13,000

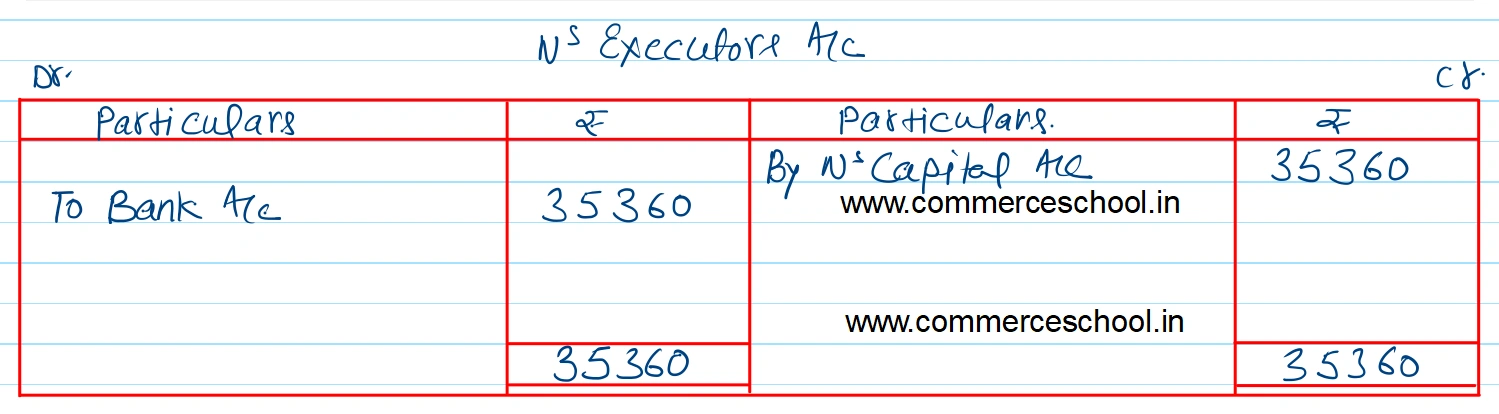

The investments were sold at par and his executors were paid out. Pass the necessary journal entries and write the account of the executors of N.

[Ans. Amount paid to N’s executors ₹ 35,360.]

Hint:

Interest on Capital : 20,000 x 8/100 x 219/365 = ₹ 960.

Anurag Pathak is an academic teacher. He has been teaching Accountancy and Economics for CBSE students for the last 18 years. In his guidance, thousands of students have secured good marks in their board exams and legacy is still going on. You can subscribe his youtube channel and can download the Android & ios app for free lectures.