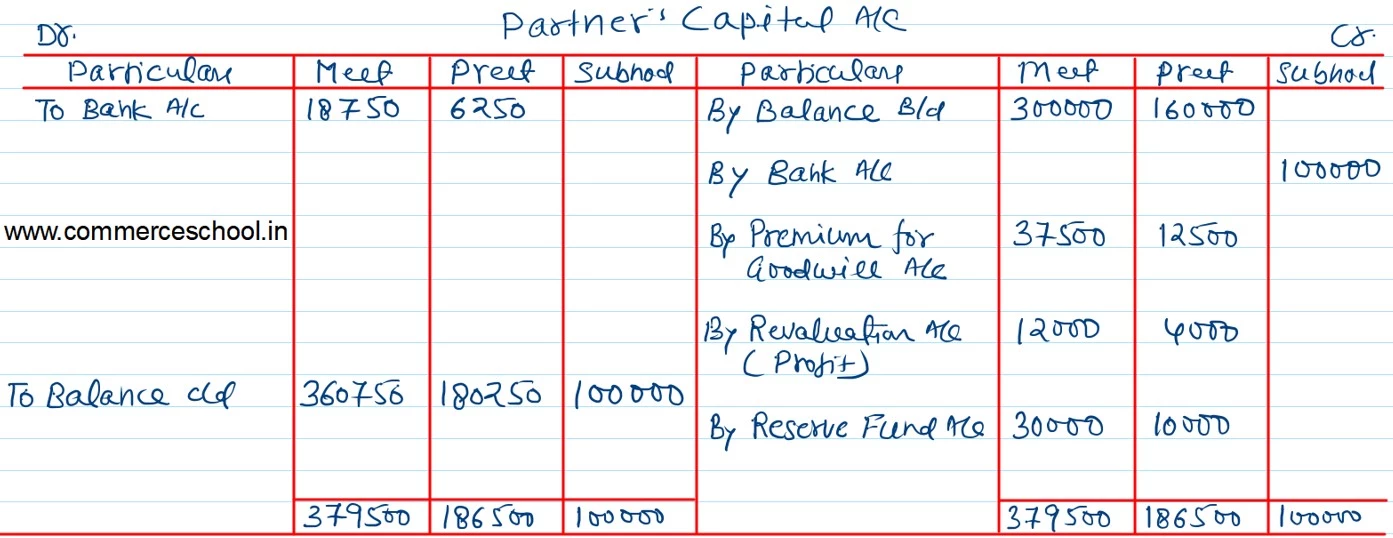

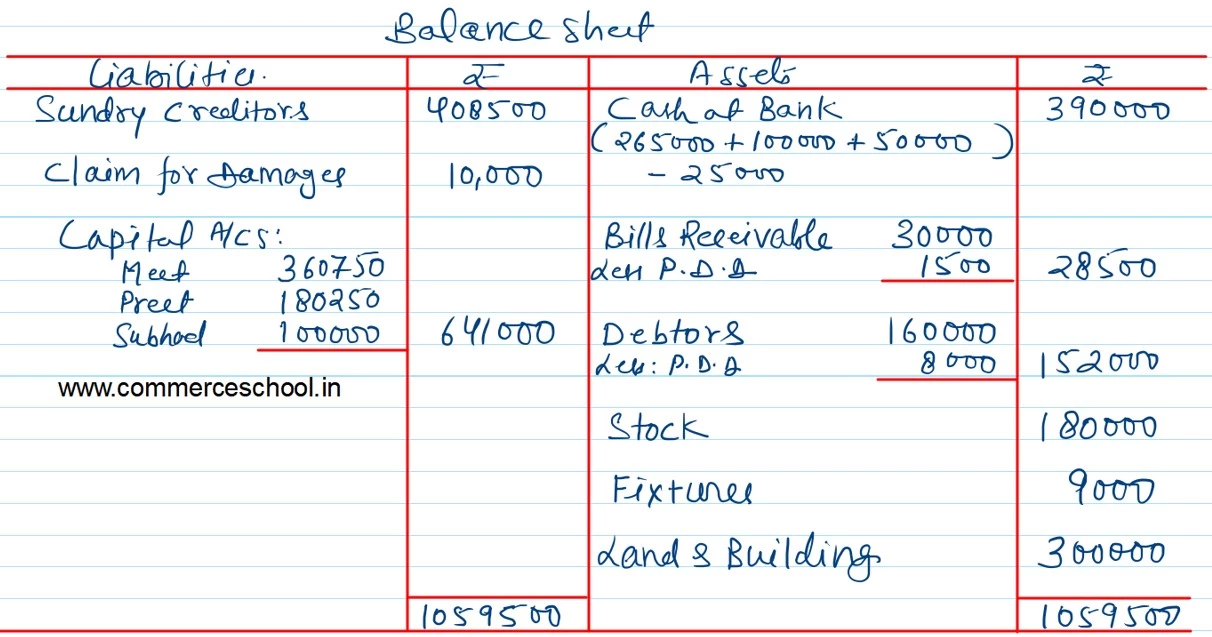

Meet and Preet share profits in the proportion of 3/4th and 1/4th. Their Balance Sheet as at 31st March, 2023 was as follows:

Meet and Preet share profits in the proportion of 3/4th and 1/4th. Their Balance Sheet as at 31st March, 2023 was as follows:

| Liabilities | ₹ | Assets | ₹ |

| Sundry Creditors

Reserve Fund Capital A/cs: Meet Preet |

4,15,000

40,000 3,00,000 1,60,000 |

Cash at Bank

Bill Receivable Debtors Stock Fixtures Land and Building |

2,65,000

30,000 1,60,000 2,00,000 10,000 2,50,000 |

| 9,15,000 | 9,15,000 |

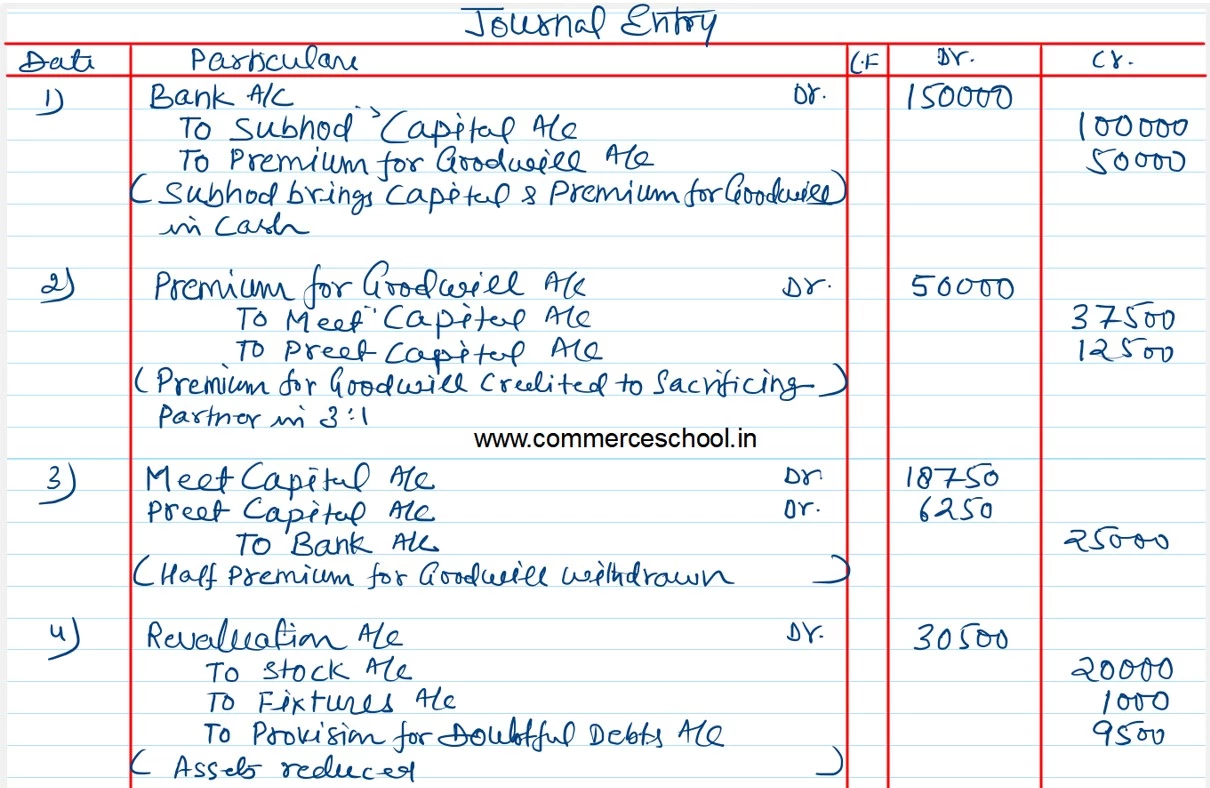

On 1st April, 2023, Subhod was admitted into partnership for 1/5th share on the following terms:

(i) Subhod pays ₹ 1,00,000 as his Capital.

(ii) Subhod pays ₹ 50,000 for Goodwill. Half of this sum is to be withdrawn by Meet and Preet.

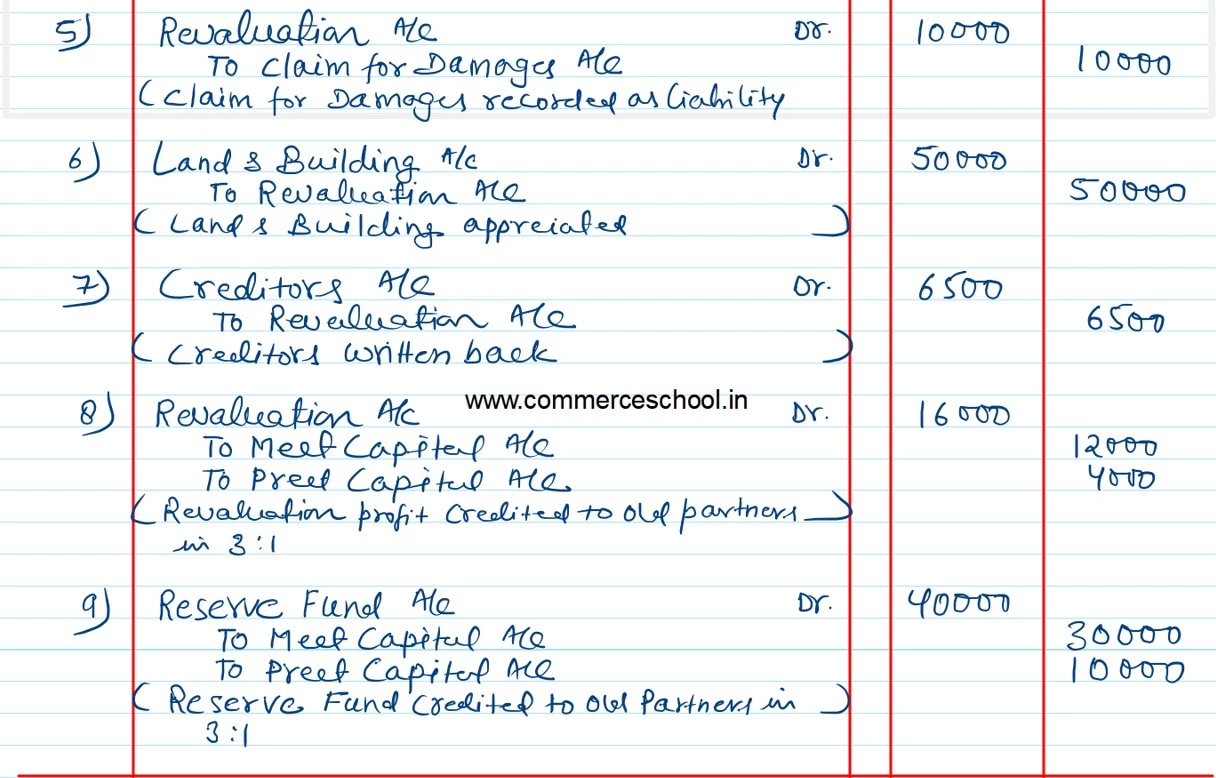

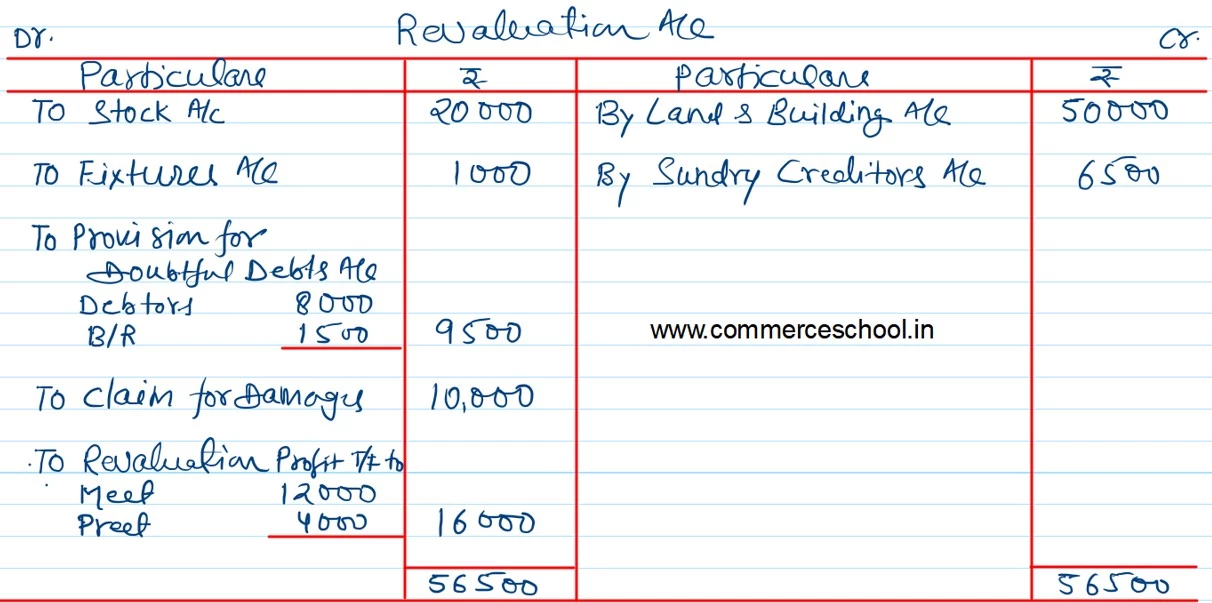

(iii) Stock and Fixtures be reduced by 10% and 5% provision for Doubtful Debts be created on Sundry Debtors and Bills Receivable.

(iv) Value of Land and Building be appreciated by 20%.

(v) Claim against the firm for damages, liability to the extent of ₹ 10,000 should be created.

(vi) Sundry Creditors ₹ 6,500, which is not likely to be claimed and hence should be written back.

(vii) Sikka, an old customer, whose account was written off as bad, has promised to pay ₹ 17,500 in settlement of hte full claim.

Record the above transactions (Journal entries) in the books of the firm assuming that the profit sharing ratio between Meet and Preet has not changed. Prepare new Balance Sheet after the admission of Subhod.

Anurag Pathak Changed status to publish