On 31st March, 2019 the Balance Sheet of Madan and Mohan who share profits and losses in the ratio of 3 : 2 was as follows:

On 31st March, 2019 the Balance Sheet of Madan and Mohan who share profits and losses in the ratio of 3 : 2 was as follows:

Balance Sheet of Madan and Mohan as at 31st March, 2019

| Liabilities | ₹ | Assets | ₹ |

| Creditors | 28,000 | Cash at Bank | 10,000 |

| General Reserve | 10,000 |

Debtors 65,000 Less: Provision 5,000 |

60,000 |

| Employees Provident Fund | 22,000 | Stock | 33,000 |

|

Captials: Madan Mohan |

60,000 40,000 | Patents | 57,000 |

| 1,60,000 | 1,60,000 |

They decided to admit Gopal on 1st April, 2019 for 1/5th share which Gopal acquired wholly from Mohan on the following terms:

(i) Gopal shall bring ₹ 10,000 as his share of premium for Goodwill.

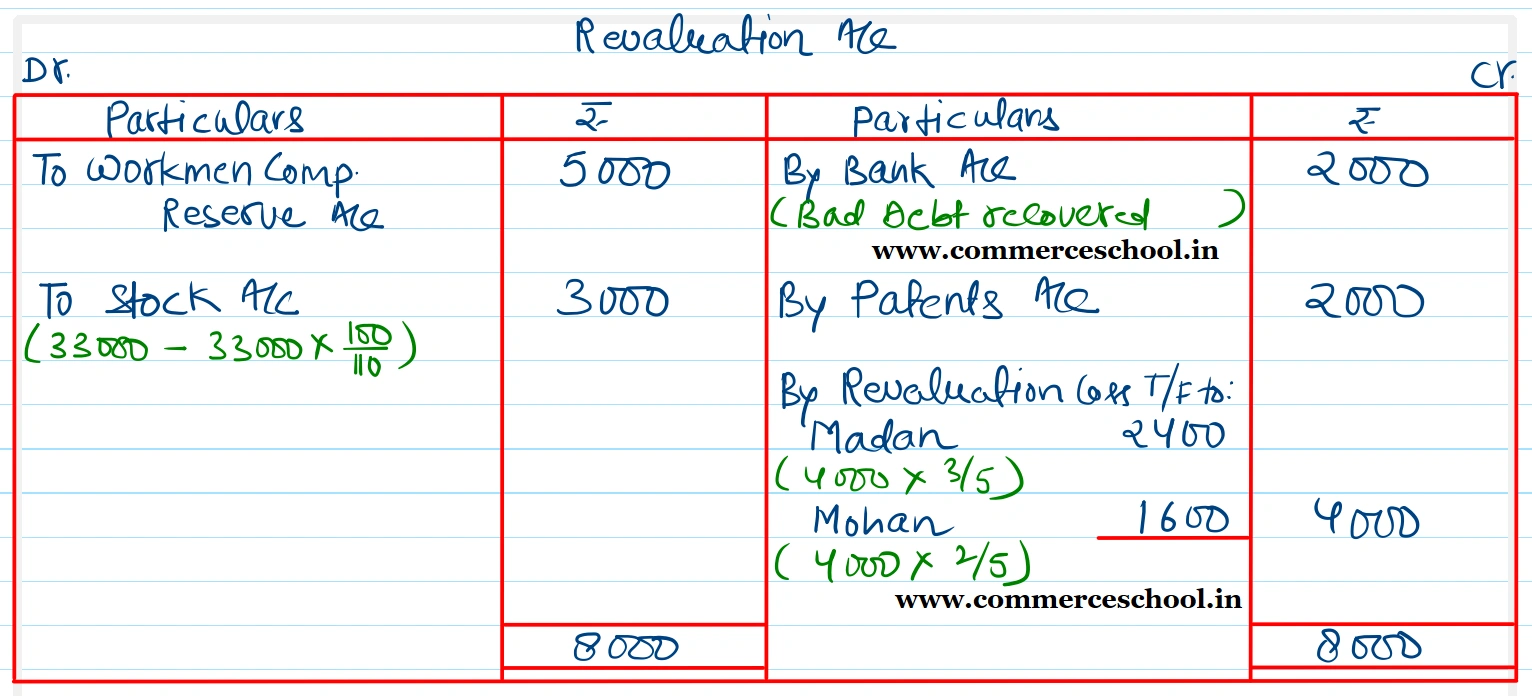

(ii) A debtor whose dues of ₹ 3,000 were written off as bad debt paid ₹ 2,000 in full settlement.

(iii) A claim of ₹ 5,000 on account of workmen’s compensation was to be provided for.

(iv) Patents were undervalued by ₹ 2,000. Stock in the books was valued 10% more than its market value.

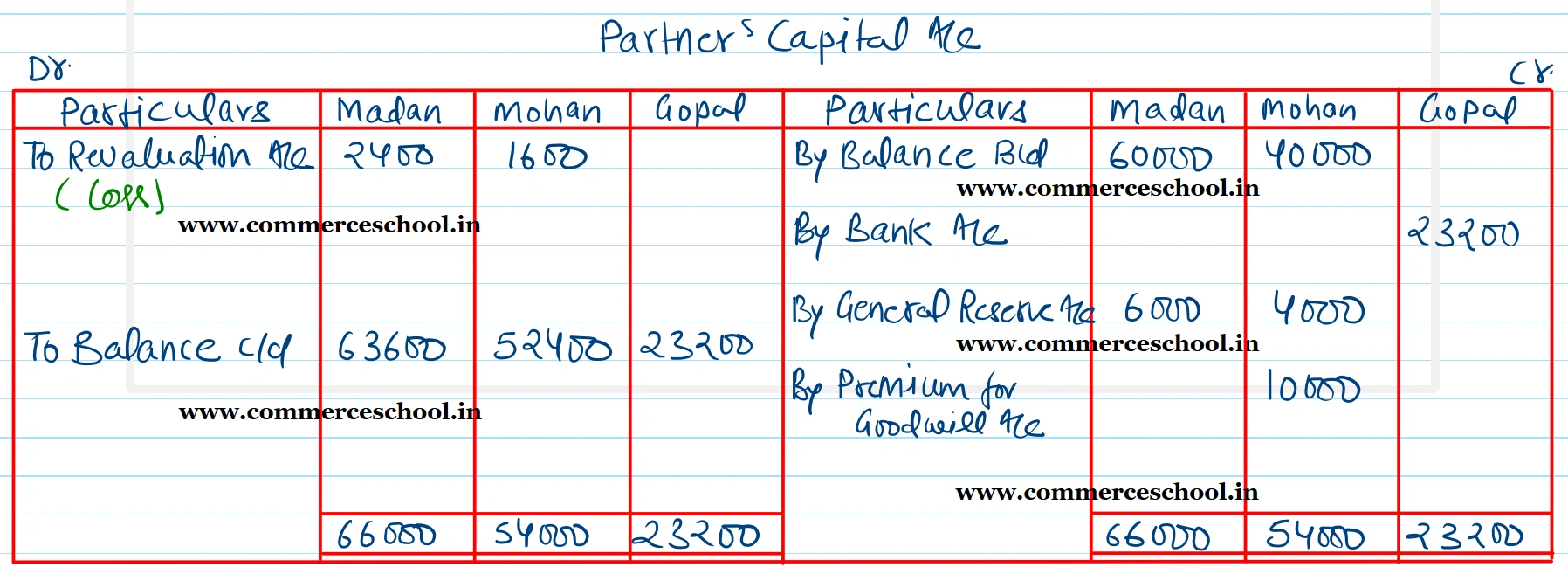

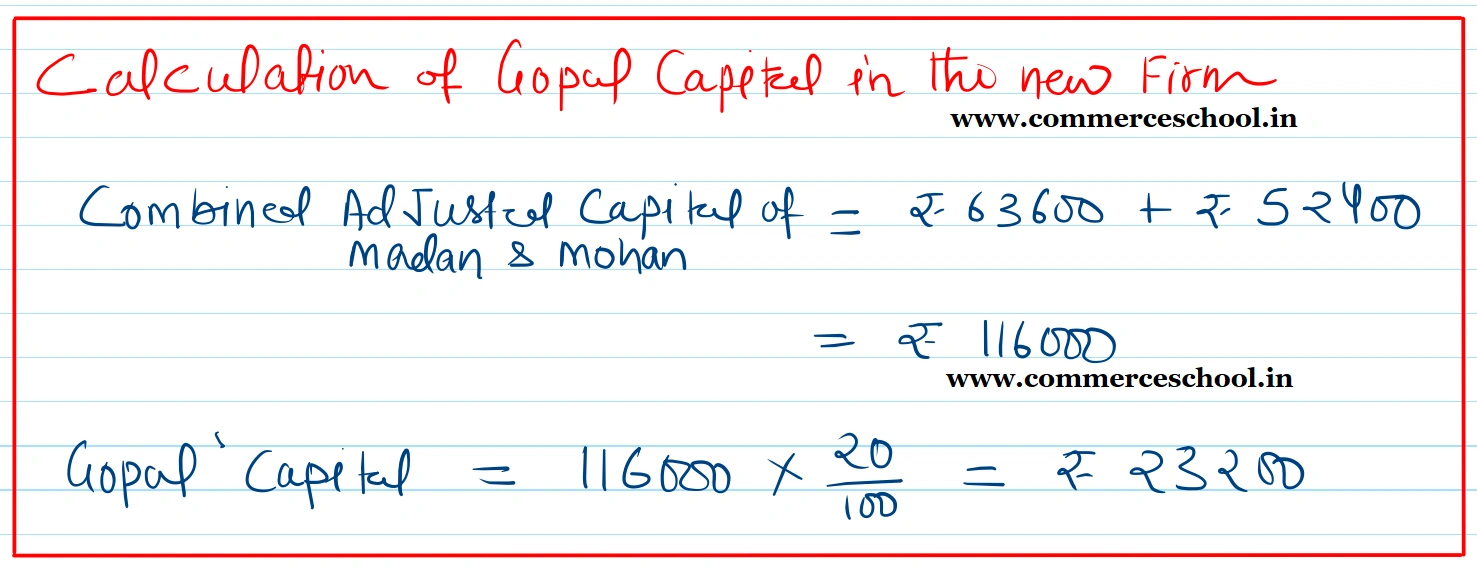

(v) Gopal was to bring in capital equal to 20% of the combined capitals of Madan and Mohan after all adjustments.

Prepare Revaluation Account, Capital Accounts of the partners and th Balance Sheet of the new firm.

[Ans. Loss on Revaluation ₹ 4,000; Capitals : Madan ₹ 63,600; Mohan ₹ 52,400 and Gopal ₹ 23,200; Bank Balance ₹ 45,200; Balance Sheet Total ₹ 1,94,200.]

Anurag Pathak Answered question