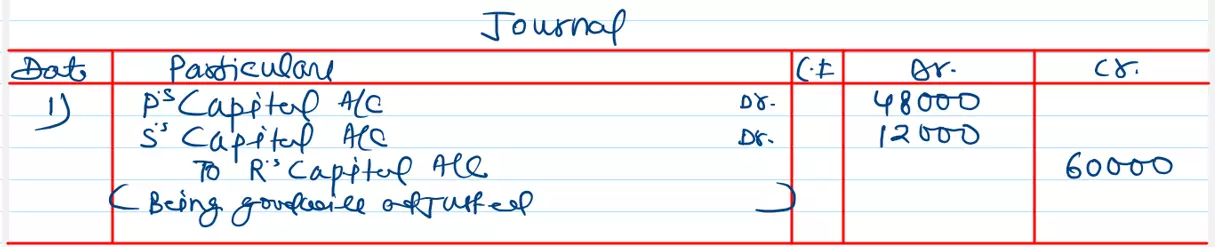

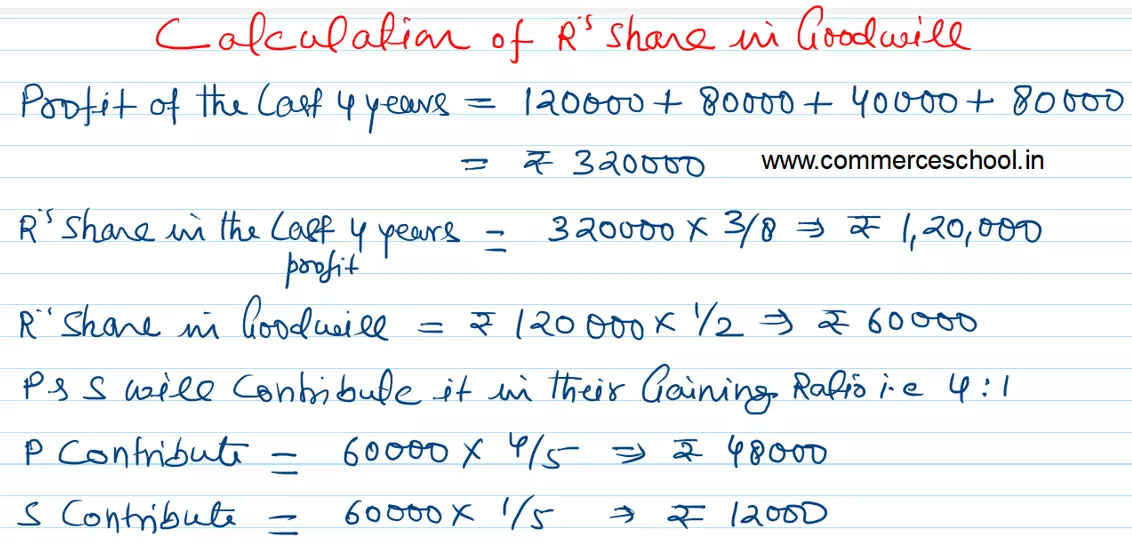

P, R and S are in partnership sharing profits 4/8, 3/8 and 1/8 respectively. It is provided in the partnership deed that on the death of any partner his share of goodwill is to be valued at one half of the net profit credited to his account during the last four completed years.

P, R and S are in partnership sharing profits 4/8, 3/8 and 1/8 respectively. It is provided in the partnership deed that on the death of any partner his share of goodwill is to be valued at one half of the net profit credited to his account during the last four completed years.

R died on 1st April, 2023. The firm’s profits for the last four years ended 31st March, were as:

2020 – ₹ 1,20,000; 2021 – ₹ 80,000; 2022 – ₹ 40,000; 2023 – ₹ 80,000.

(a) Determine the amount that should be credited to R in respect of his share of Goodwill.

(b) Pass Journal entry for adjustment of Goodwill.

Anurag Pathak Changed status to publish