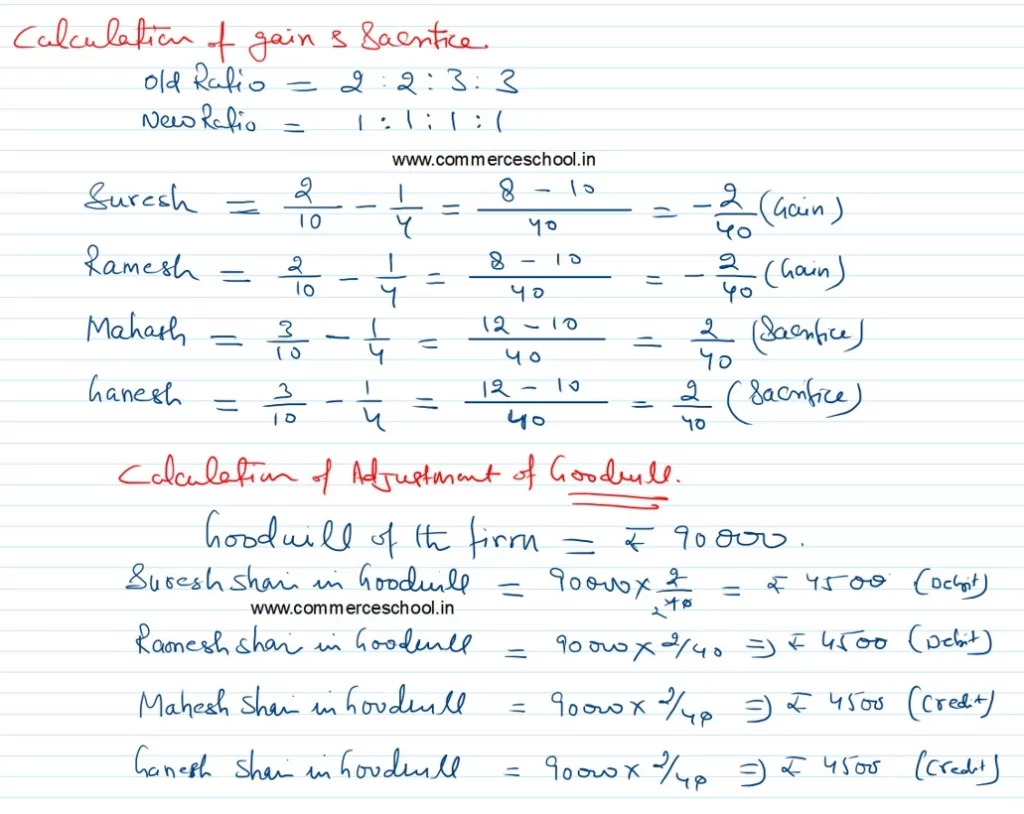

Suresh, Ramesh, Mahesh and Ganesh were partners in a firm sharing profits in the ratio of 2 : 2 : 3 : 3. On 1st April, 2016, their Balance Sheet was as follows:

Suresh, Ramesh, Mahesh and Ganesh were partners in a firm sharing profits in the ratio of 2 : 2 : 3 : 3. On 1st April, 2016, their Balance Sheet was as follows:

| Liabilities | ₹ | Assets | ₹ |

| Capital A/cs

Suresh Ramesh Mahesh Ganesh Workmen Compensation Reserve Sundry Creditors |

1,00,000 1,50,000 2,00,000 2,50,000 75,000 1,70,000 |

Fixed Assets

Current Assets |

6,00,000 3,45,000 |

| 9,45,000 | 9,45,000 |

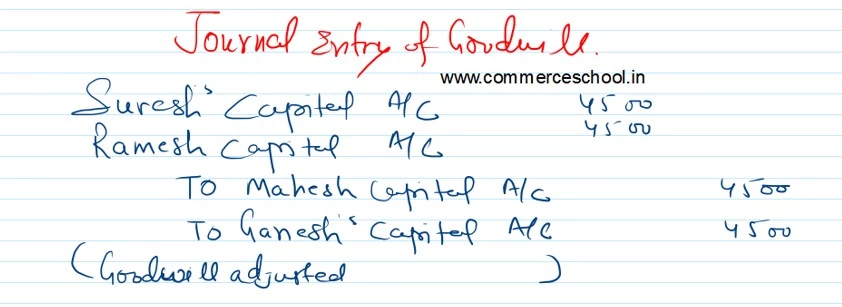

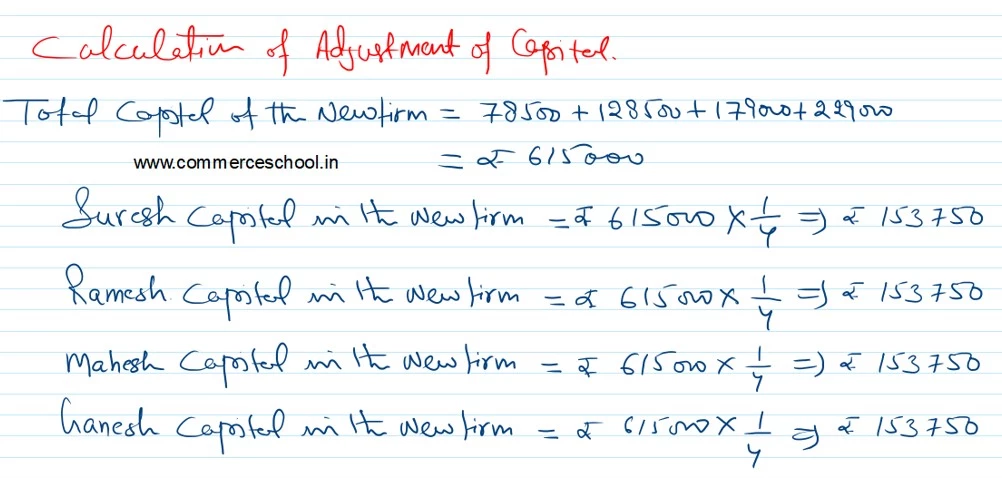

From the above date, the partners decided to share the future profits equally. For this purpose, the goodwill of the firm was valued at ₹ 90,000. It was also agreed that:

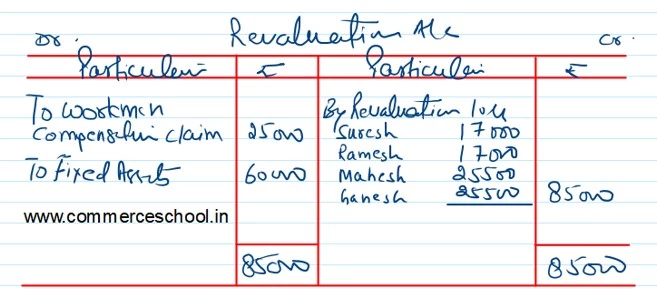

a) Claim against Workmen Compensation Reserve will be estimated at ₹ 1,00,000 and fixed assets will be depreciated by 10%.

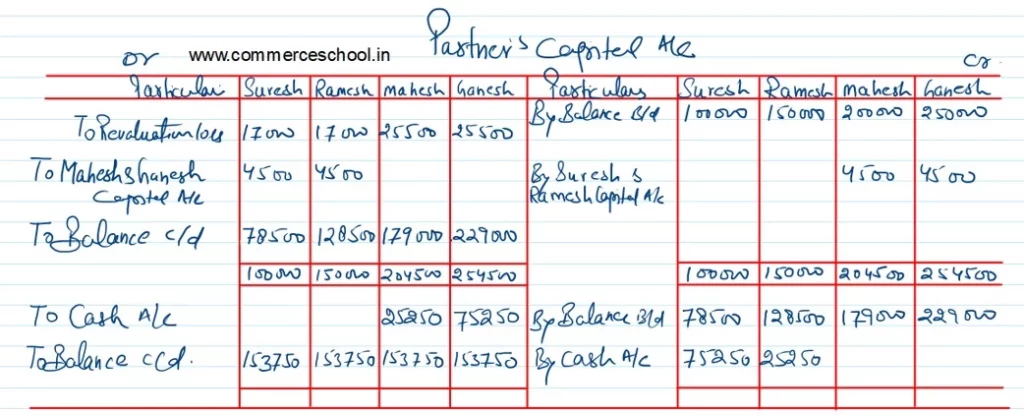

b) The Capitals of the partners will be adjusted according to the new profit sharing ratio.

For this, necessary cash will be brought or paid by the partners as the case may be.

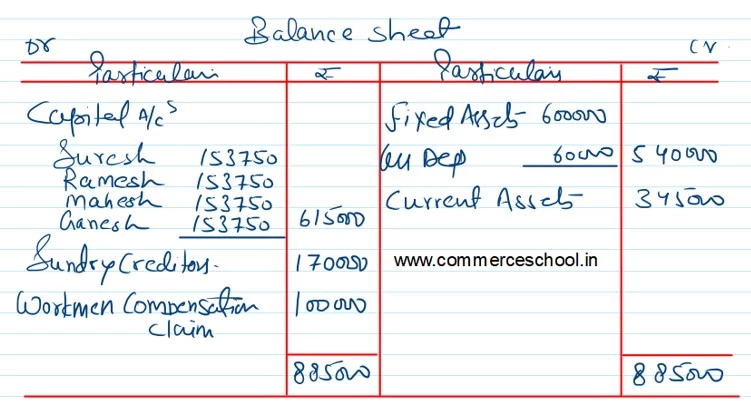

Prepare the Revaluation Account, Partner’s Capital Accounts and the Balance Sheet of the reconstituted firm.

Anurag Pathak Changed status to publish