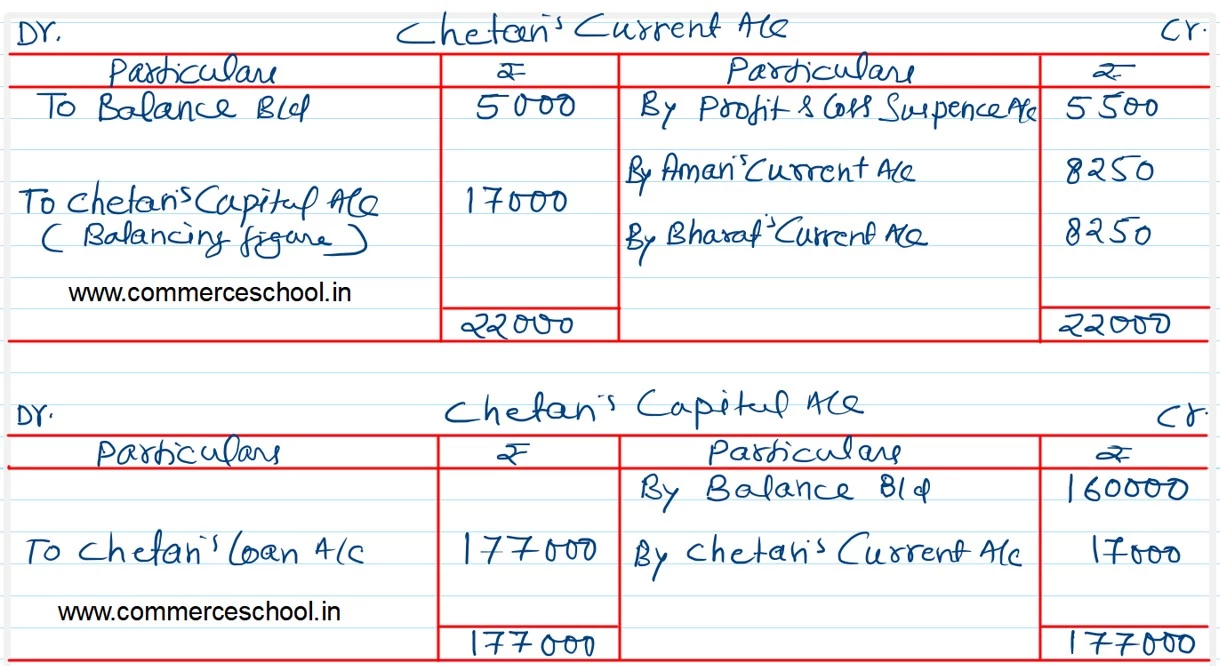

The Partnership Deed of Aman, Bharat and Chetan has a clause that any partner may retire from the firm on the following terms by giving six months’ notice in writing. The retiring partner shall be paid

The Partnership Deed of Aman, Bharat and Chetan has a clause that any partner may retire from the firm on the following terms by giving six months’ notice in writing. The retiring partner shall be paid:

a) The amount standing to the credit of his Capital Account and Current Account.

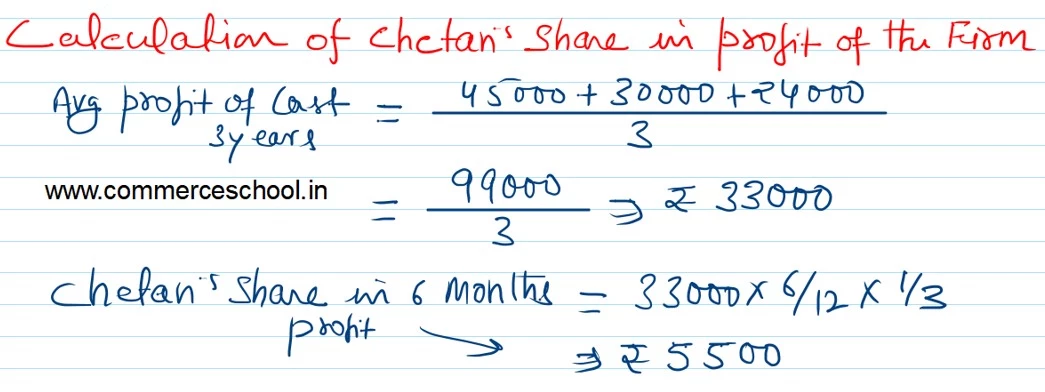

b) His share of profit to the date of retirement, calculated on the basis of the average profit of the three preceding completed years, if he retires in between the year.

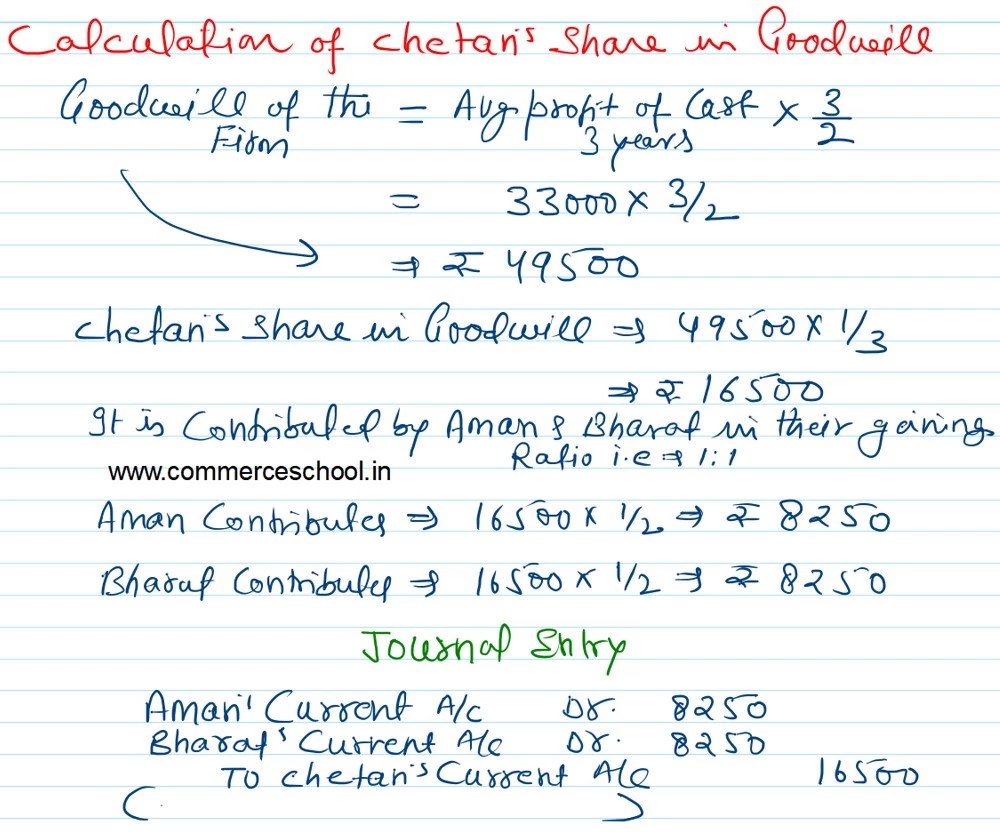

c) His share of Goodwill of the firm calculated on the basis of 1 and half times the average profit of the three preceding completed years.

d) Assets shall be revalued and liabilities re-assessed. Retiring partner will get his share in the gain (profit) and will bear loss, if any.

Chetan gave notice on 31st March, 2022 to retire with effect from 30th September 2022. On that date, the balance of his capital was ₹ 1,60,000 and his Current Account (in debit) ₹ 5,000. The profits for the three preceding completed years were: I – ₹ 45,000; II – ₹ 30,000, III – ₹ 24,000.

Revaluation of assets and reassessment of liabilities resulted in neither gain (profit) nor loss.

What amount is due to Chetan in accordance with the partnership agreement?

[Ans.: Amount due to Chetan = ₹ 1,77,000. Amount transferred from Chetan’s Current A/c to Chetan’s Capital A/c after adjustment – ₹ 17,000.]

Anurag Pathak Changed status to publish