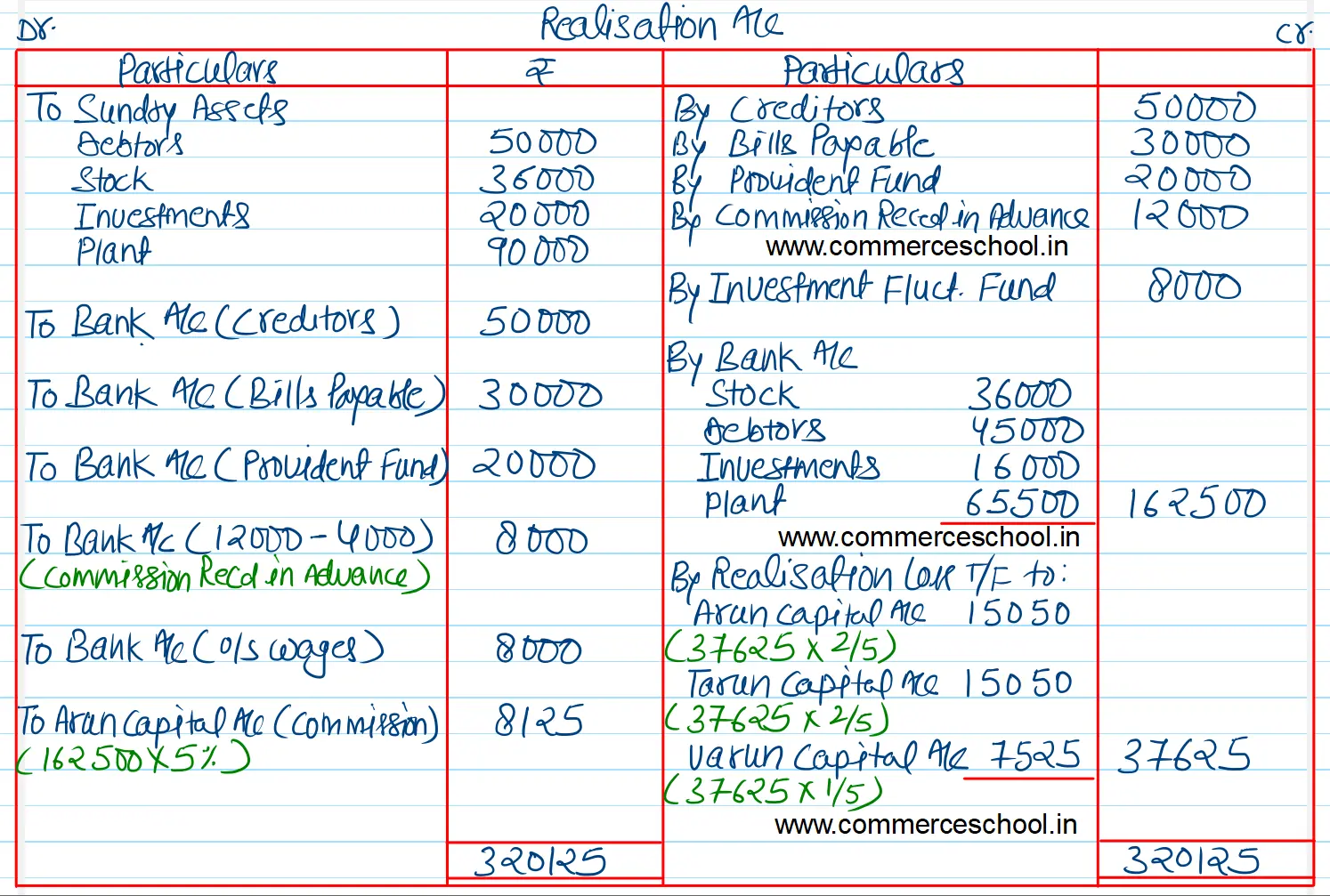

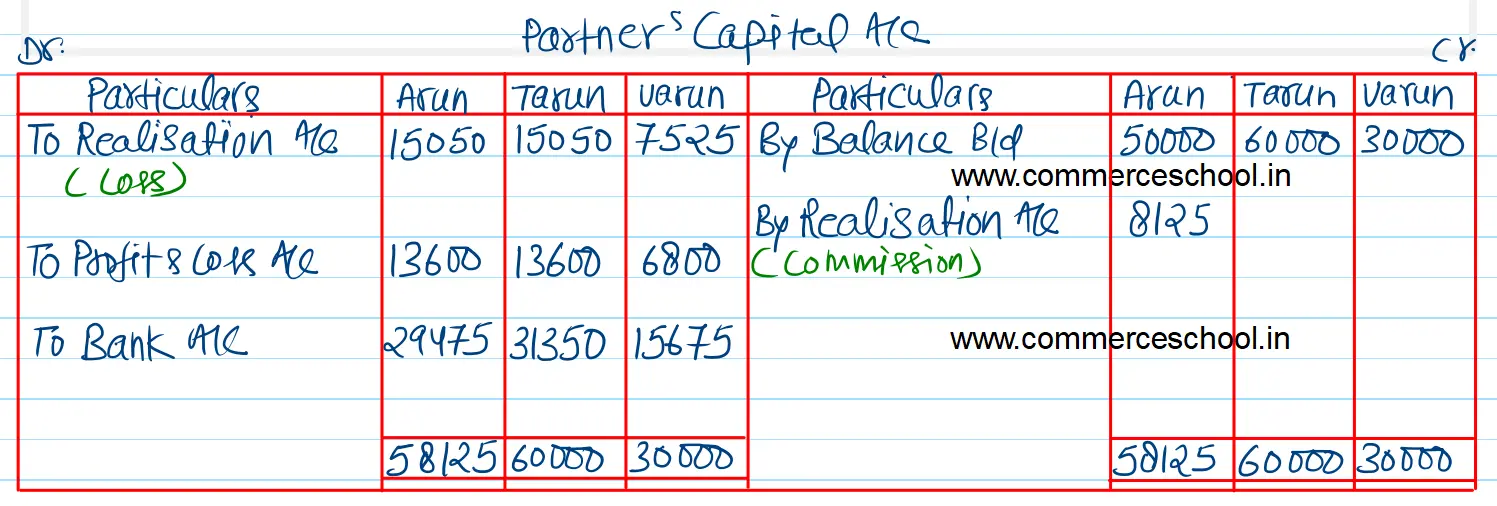

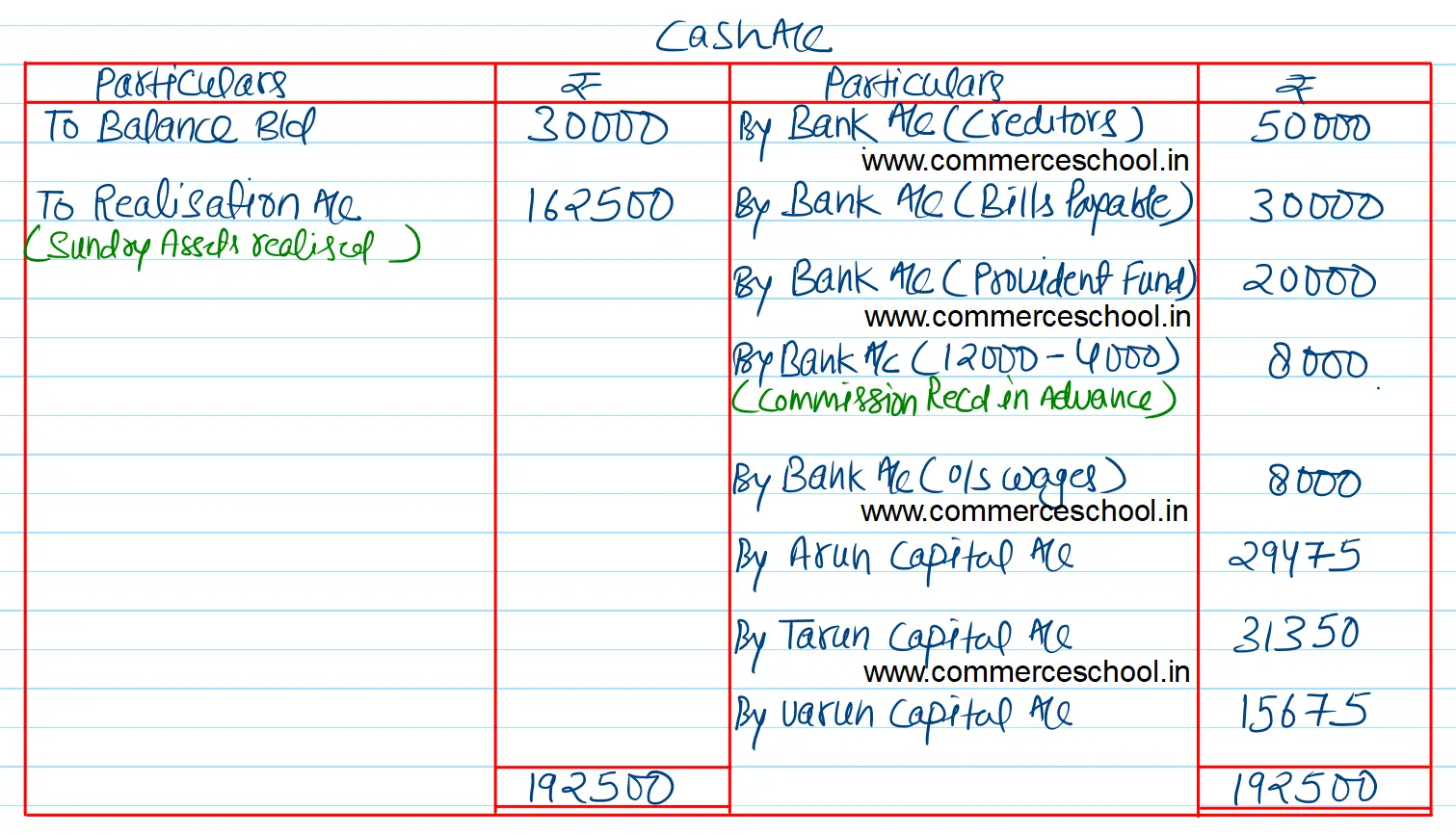

Arun, Tarun and Varun share profits in the ratio of 2 : 2 : 1. On 31.12.2022 their Balance Sheet was as follows:

Arun, Tarun and Varun share profits in the ratio of 2 : 2 : 1. On 31.12.2022 their Balance Sheet was as follows:

| Liabilities | ₹ | Assets | ₹ |

| Creditors | 50,000 | Cash | 30,000 |

| Bills Payable | 30,000 | Debtors | 50,000 |

| Provident Fund | 20,000 | Stock | 36,000 |

| Investment Fluctuation Fund | 8,000 | Investments | 20,000 |

| Commission Received in Advance | 12,000 | Plant | 90,000 |

| Capitals: Arun Tarun Varun | 50,000 60,000 30,000 | Profit & Loss A/c | 34,000 |

| 2,60,000 | 2,60,000 |

On this date the firm was dissolved. Arun was appointed to realise the assets.

Arun was to receive 5% commission on the sale of assets (except cash) and was to bear all expenses of realisation.

Arun realised the assets as follows: Stock ₹ 36,000, Debtors ₹ 45,000, Investments 80% of the book value, Plant ₹ 65,500.

Expenses of realisation amounted to ₹ 5,500.

Commission received in advance was returned to the customers after deducting ₹ 4,000.

Firm had to pay ₹ 8,000 for outstanding wages. This liability was not provided for in the above Balance Sheet.

₹ 20,000 had to be paid for provident fund.

Prepare Realisation Account, Capital Accounts and Cash Account.

[Ans. Loss on Realisation ₹ 37,625; Final Payment Arun ₹ 29,475, Tarun ₹ 31,350 and Varun ₹ 15,675; Total of Cash A/c ₹ 1,92,500.]

Anurag Pathak Changed status to publish