Balance Sheet of Somesh, Rahul and Kamlesh, who were sharing profits in the ratio of 3 : 3 : 4 respectively as on 31st March, 2025 was as follows:

Balance Sheet of Somesh, Rahul and Kamlesh, who were sharing profits in the ratio of 3 : 3 : 4 respectively as on 31st March, 2025 was as follows:

Balance Sheet of Somesh, Rahul and Kamlesh as at 31st March, 2025

| Liabilities | ₹ | Assets | ₹ |

| Sundry Creditors | 44,000 | Cash | 32,000 |

| General Reserve | 10,000 | Stock | 88,000 |

| Capital A/cs: Somesh Rahul Kamlesh | 1,20,000 1,00,000 80,000 | Investments | 94,000 |

| Land and Buildings | 1,20,000 | ||

| Loan to Somesh | 20,000 | ||

| 3,54,000 | 3,54,000 |

Somesh died on 31st July, 2025. The Partnership deed provided for the following on the death of a partner:

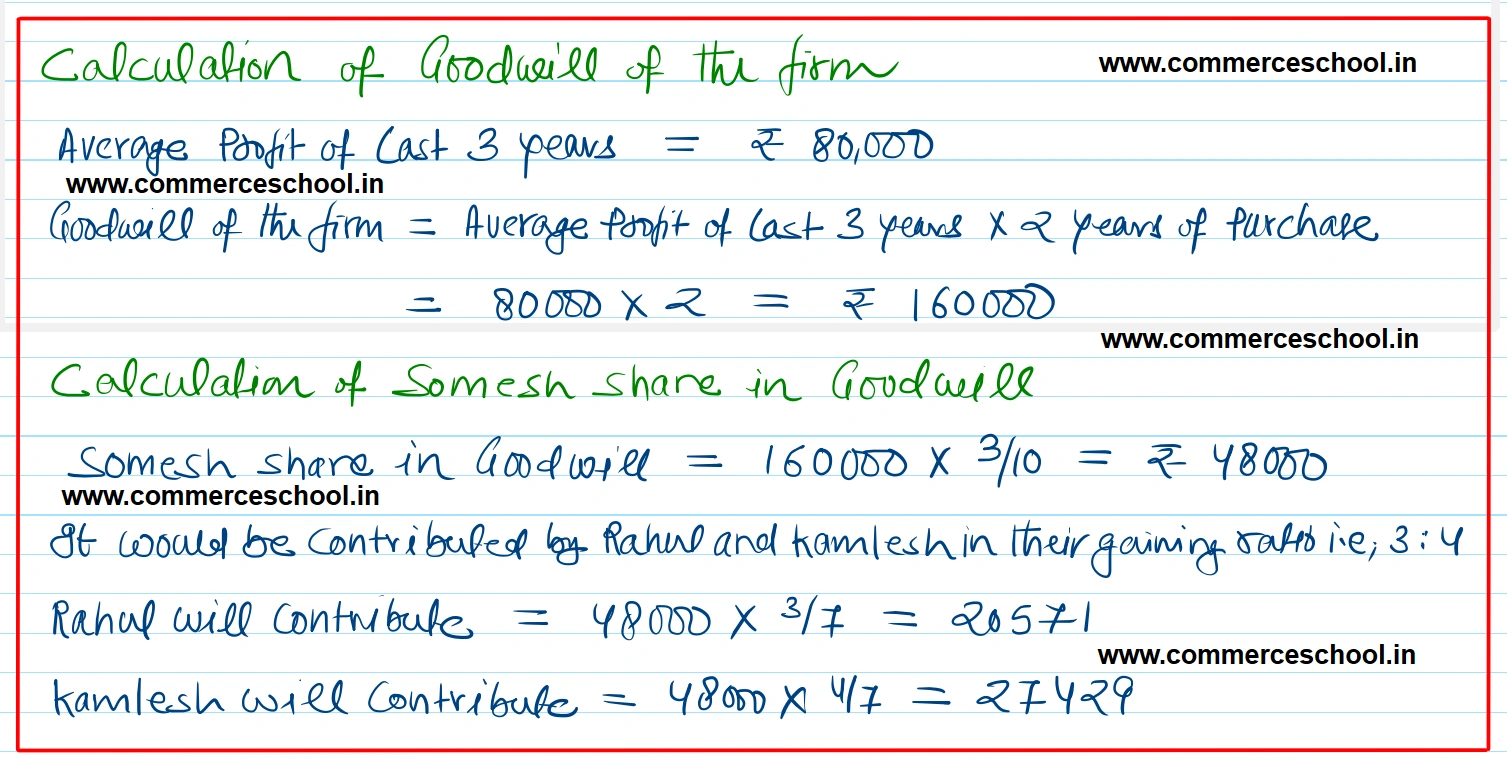

(a) Goodwill of the firm be valued at two year’s purchase of average profit for the last three years which was ₹ 80,000.

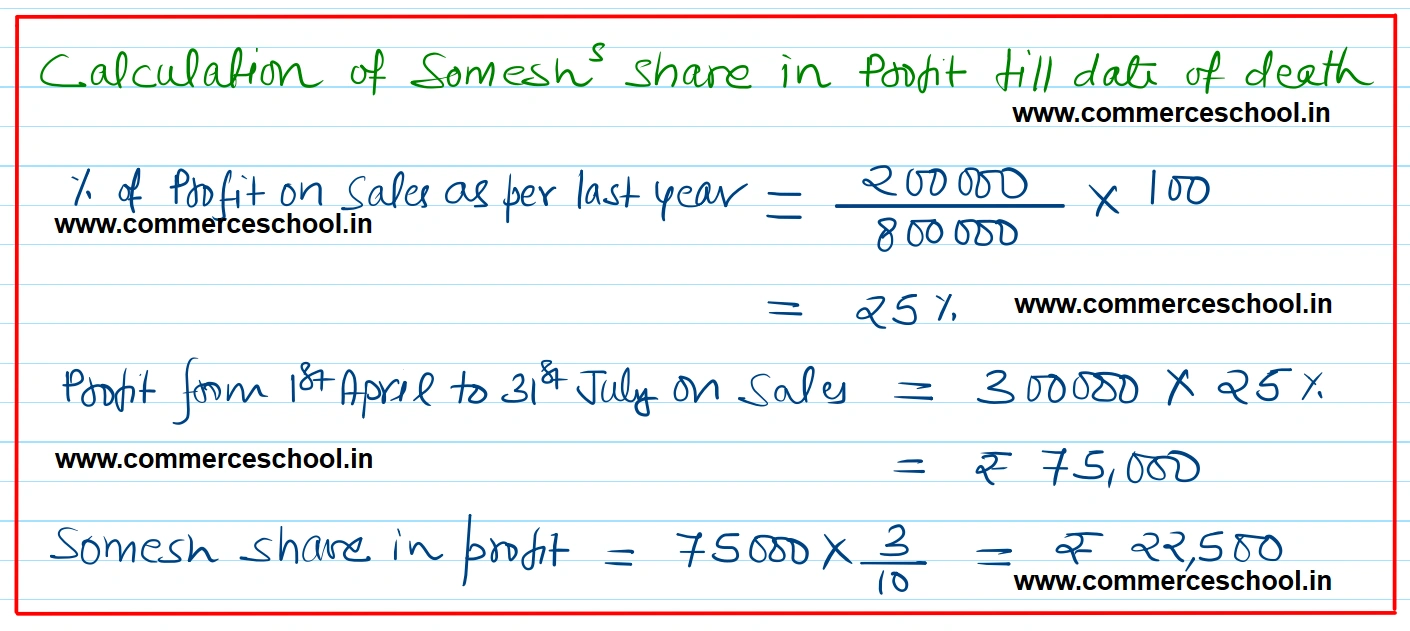

(b) Somesh’ share of profit till the date of his death was to be calculated on the basis of sales. Sales for the year ended 31st March, 2025 was ₹ 8,00,000 and that from 1st April to 31st July, 2025 ₹ 3,00,000. Profit for the year ended 31st March, 2025 was ₹ 2,00,000.

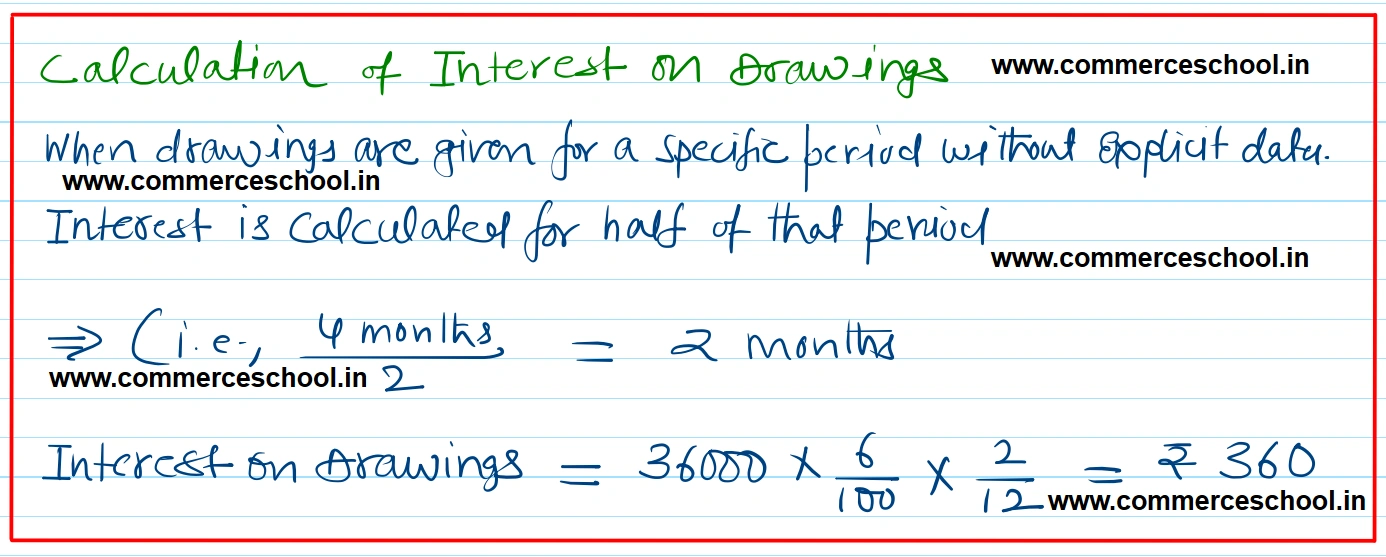

(c) Interest on capital is to be allowed and interest on Drawings is to be charged @ 6% p.a. Drawings for the period were ₹ 36,000.

Prepare Somesh’s Capital Account to be rendered to his executor.

[Ans.: Somesh’s share of Goodwill – ₹ 48,000; Somesh’s share of profit till death – ₹ 22,500; Interest on Capital – ₹ 2,400; Interest on Drawings – ₹ 360; Somesh’s Executors A/c – ₹ 1,39,54

Anurag Pathak Changed status to publish