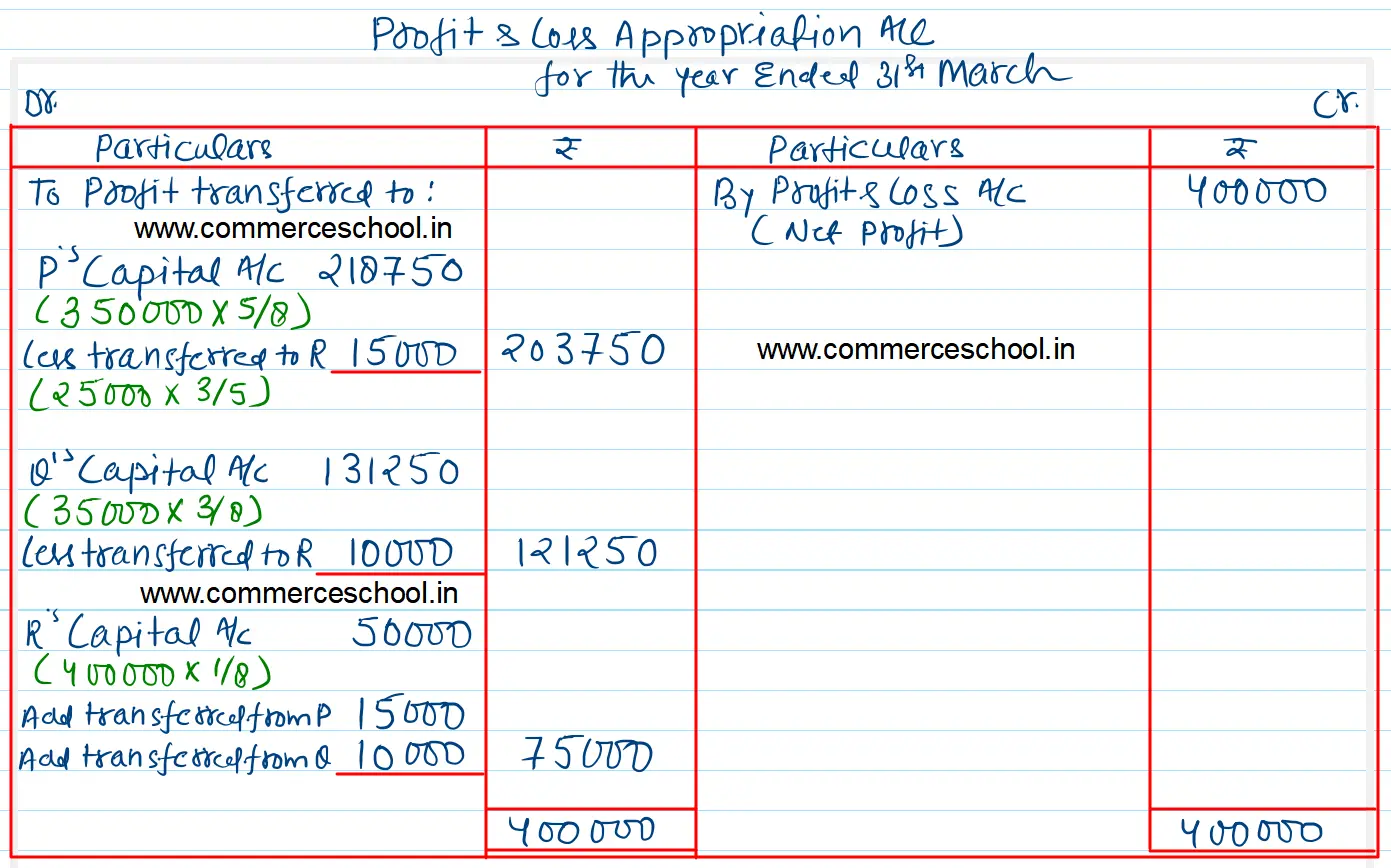

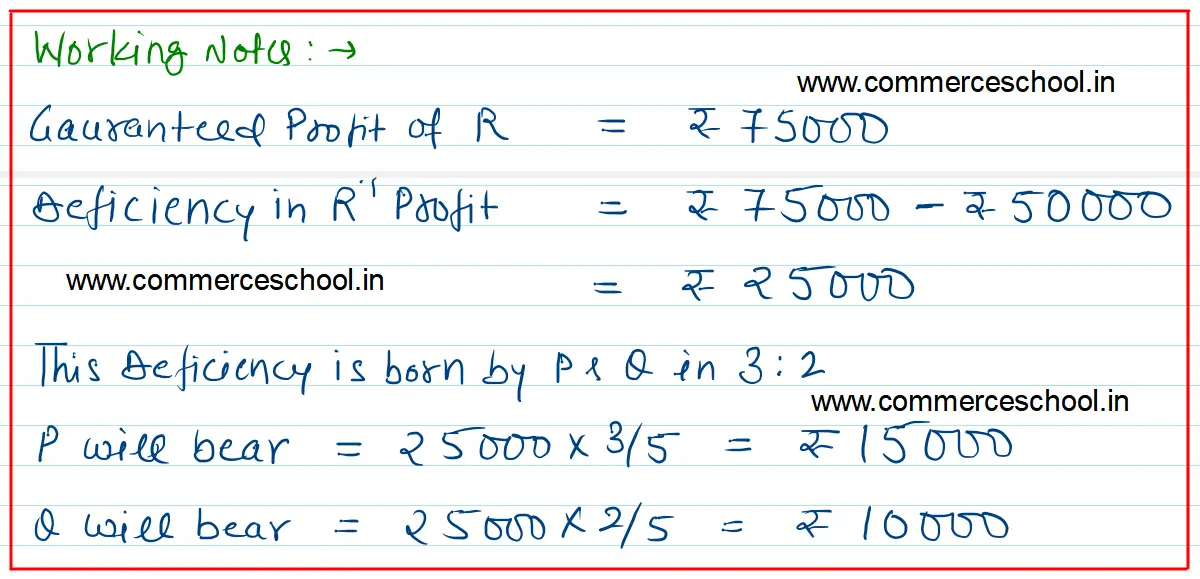

P and Q were partners in a firm sharing profits in the ratio of 5:3. On 1st April 2022 they admitted R as a new partner for 1/8th share in the profits with a guaranteed profit of ₹ 75,000.

P and Q were partners in a firm sharing profits in the ratio of 5:3. On 1st April 2022 they admitted R as a new partner for 1/8th share in the profits with a guaranteed profit of ₹ 75,000. The new profit-sharing ratio between P and Q will remain the same but they agreed to bear any deficiency on account of the guarantee to R in the ratio of 3:2. The profit of the firm for the year ended 31st March 2023 was ₹ 4,00,000.

Prepare Profit and Loss Appropriation Account of P, Q, and R for the year ended 31st March 2023.

Anurag Pathak Changed status to publish