Repairs to plant amounting to ₹ 2,000 had been charged to Plant and Machinery Account. Pass the rectification entries for the following transactions:

Pass the rectification entries for the following transactions:

(i) Repairs to plant amounting to ₹ 2,000 had been charged to Plant and Machinery Account.

(ii) An entry of ₹ 1,450 representing the selling price of goods returned to Mohan had been made in Return Outwards Book and posted. The amount should have been ₹ 1,300, the invoice value of the good in question.

(iii) A cheque for ₹ 8,500 received from Sandesh was credited to the account of Ramesh.

(iv) Goods to the value of ₹ 7,000 returned by Prateek were included in Closing stock, but not entry was made in the books.

(v) Goods costing ₹ 5,000 were purchased for various members of the staff and the cost was included in ‘Purchases’. A similar amount was deducted from the salaries of the staff members concerned and the net payments to them debited to Salaries Account.

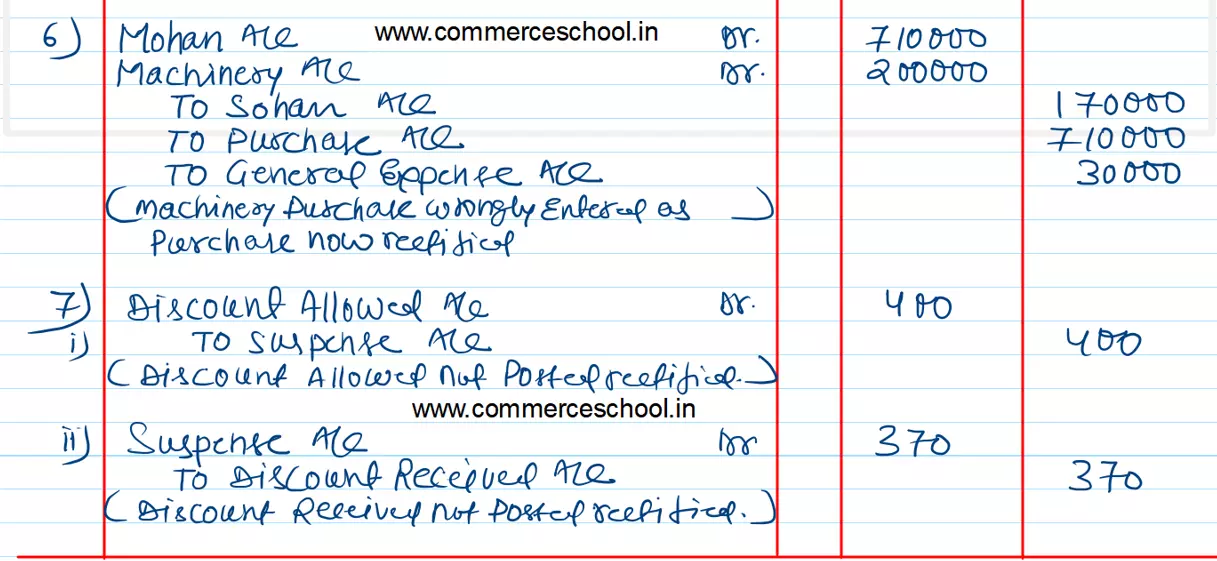

(vi) Credit purchase of old machinery from Sohan for ₹ 1,70,000 was entered in the Purchase Book as purchase from Mohan for ₹ 7,10,000. ₹ 30,000 paid as repairing charges on the reconditioning of a newly purchased second hand machinery were debited to General Expenses Account.

(vii) Debit and Credit totals of discount columns in the Cash Book which come to ₹ 400 and ₹ 370 respectively have not been posted to Discount Accounts.

Anurag Pathak Changed status to publish