Anshu and Vihu were partners in a firm sharing profits and losses in the ratio of 3 : 2. Their Balance sheet as at 31st March, 2023 was as follows:

Anshu and Vihu were partners in a firm sharing profits and losses in the ratio of 3 : 2. Their Balance sheet as at 31st March, 2023 was as follows:

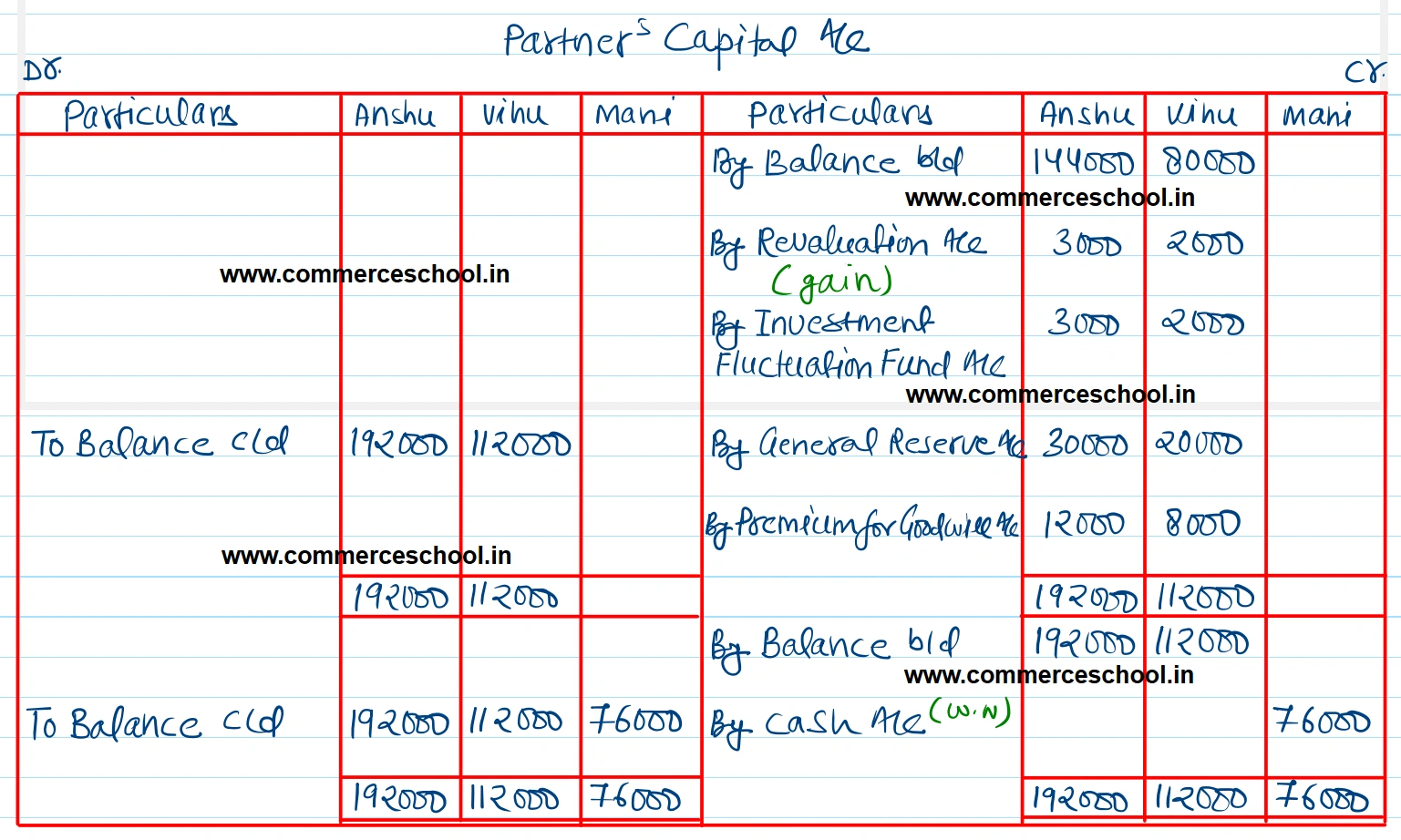

On 1st April, 2023, Mani was admitted into partnership for 1/5th share in the profits of the following terms:

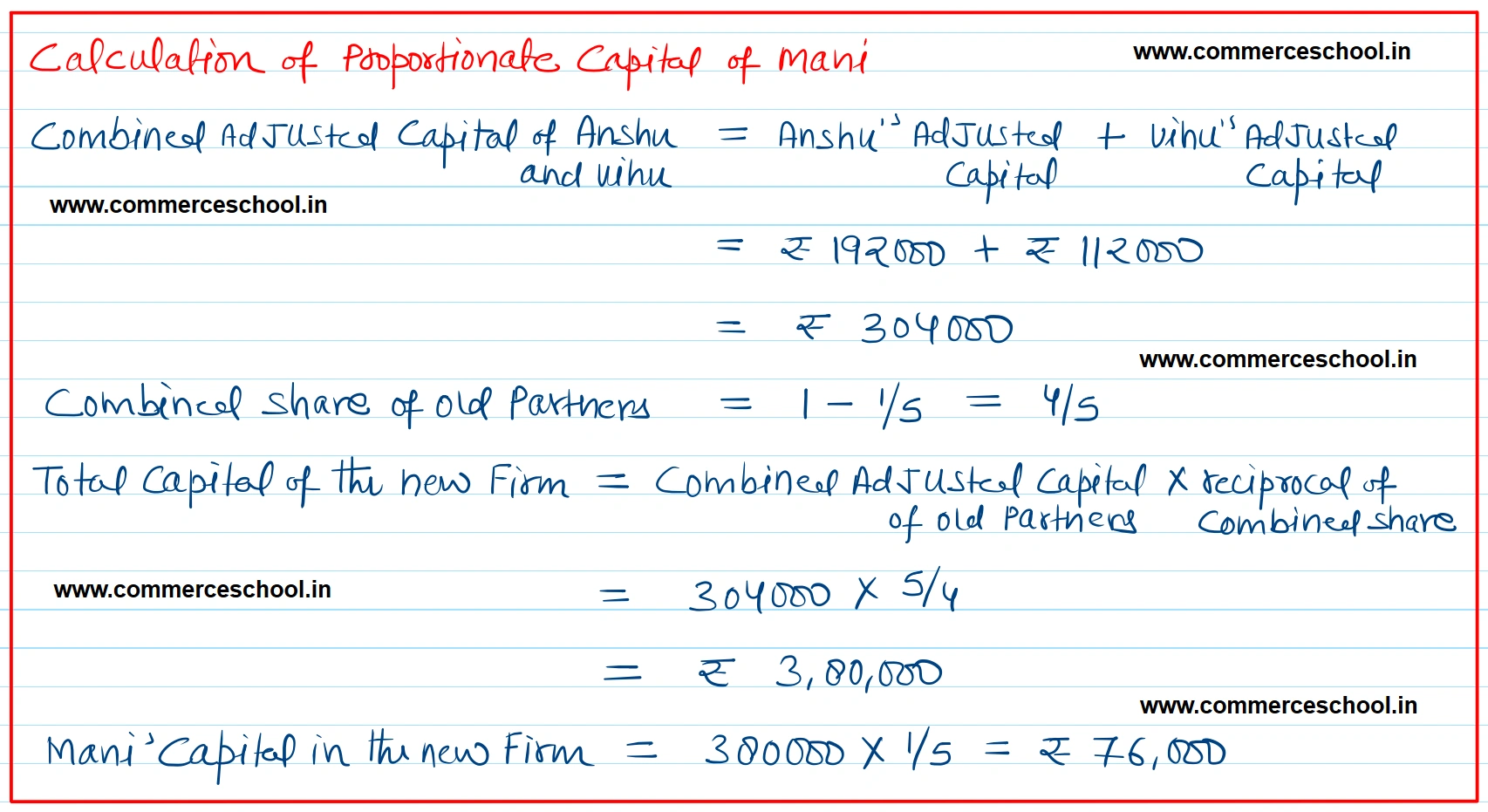

(i) Mani brought 20,000 as her share of goodwill and proportionate capital.

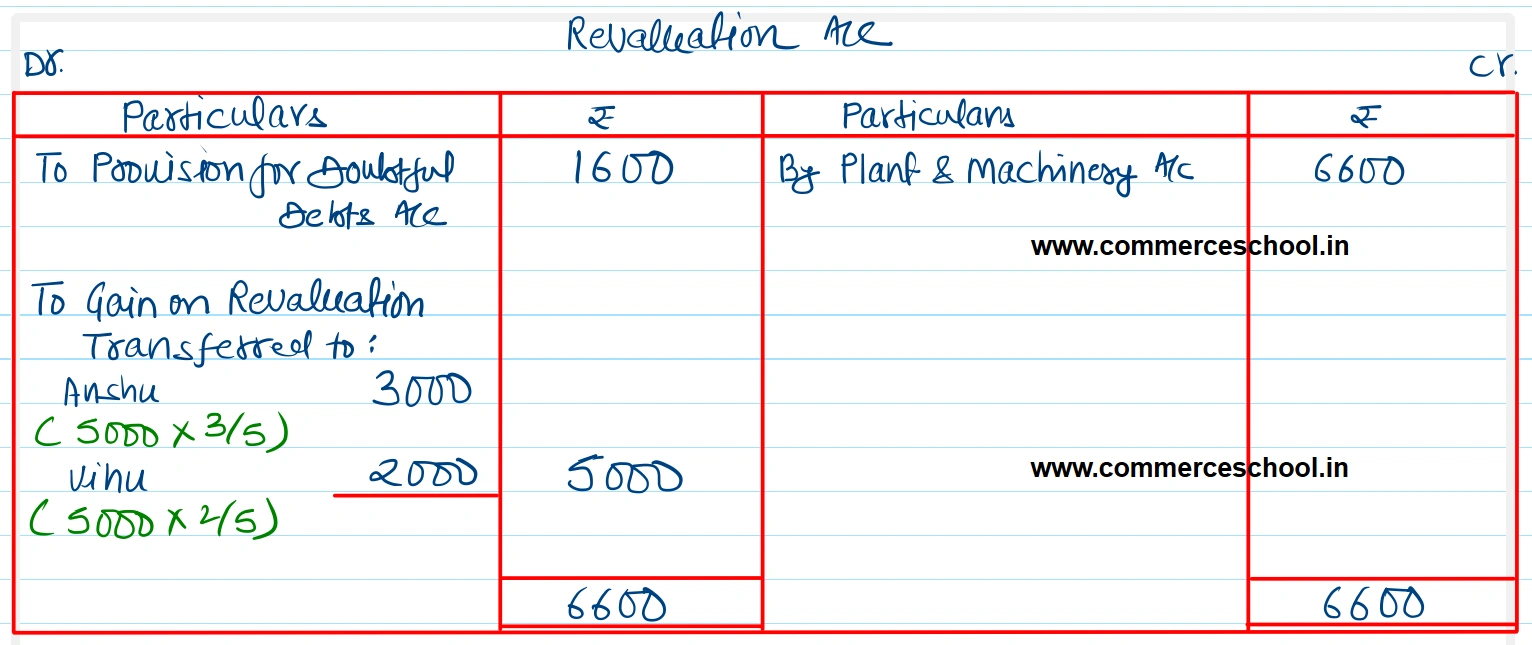

(ii) Provision for Doubtful Debts was to be maintained at 10% on debtors.

(iii) Market Value of investments was 35,000.

(iv) The value of Plant and Machinery be increased by 6,600.

Prepare Revaluation Account and Partners’ Capital Accounts.

(CBSE 2024 C)

[Ans.: Sacrificing Ratio-3: 2; Gain (Profit) on Revaluation- 5,000; Partners’ Capital A/c Balances: Anshu- 1,92,000; Vihu 1,12,000; Mani 76,000.]

| Liabilities | ₹ | Assets | ₹ |

| Creditors | 80,000 | Cash | 40,000 |

| General Reserve | 50,000 | Debtors 36,000 Less: PDD 2,000 | 34,000 |

| Investment Fluctuation Fund | 10,000 | Stock | 30,000 |

| Capitals: Anshu Vihu | 1,44,000 80,000 | Investments | 40,000 |

| Plant and Machinery | 2,20,000 | ||

| 3,64,000 | 3,64,000 |

Anurag Pathak Answered question