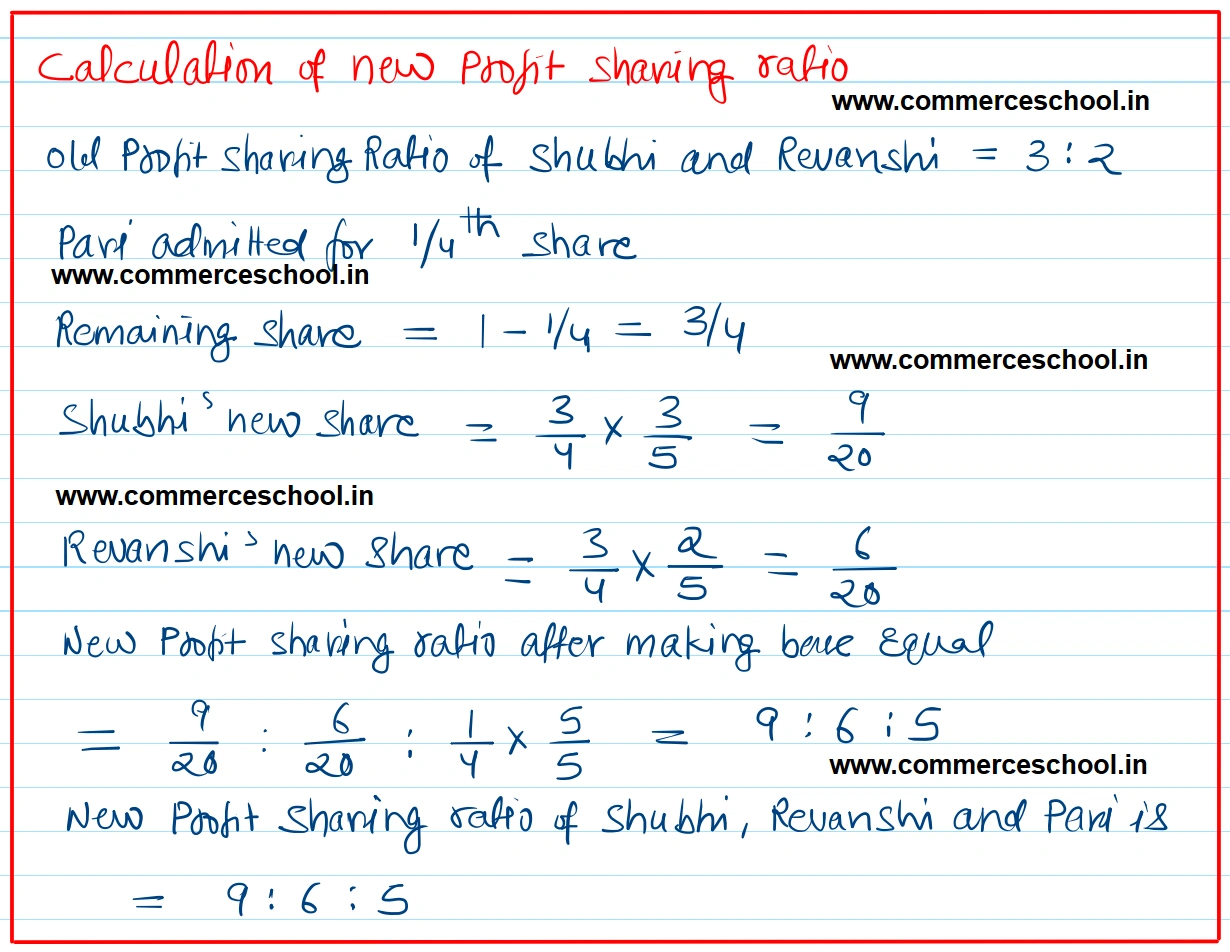

Shubhi and Revanshi were partners in a firm sharing profit and losses in the ratio fo 3 : 2. Their Balance sheet as at 31st March, 2023 was as follows:

Shubhi and Revanshi were partners in a firm sharing profit and losses in the ratio fo 3 : 2. Their Balance sheet as at 31st March, 2023 was as follows:

On 1st April, 2023, they admitted Pari into the partnership on the following terms:

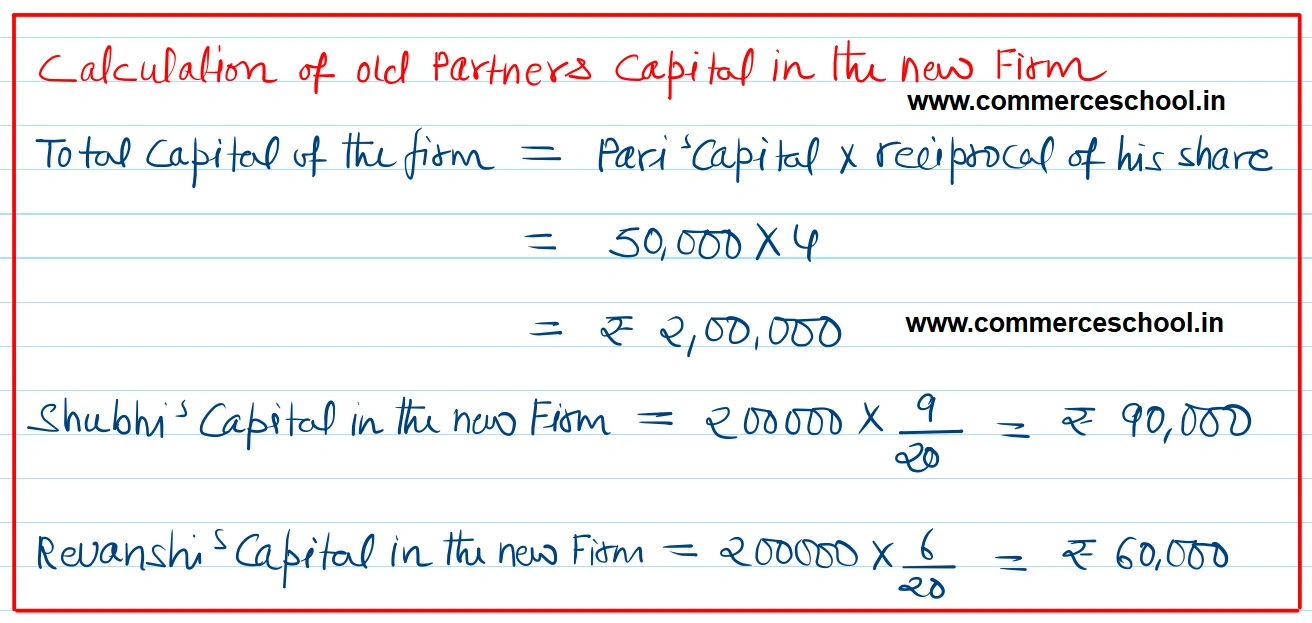

(i) Pari will bring 50,000 as her capital and 50,000 for her share of premium for goodwill for 1/4th share in the profits of the firm.

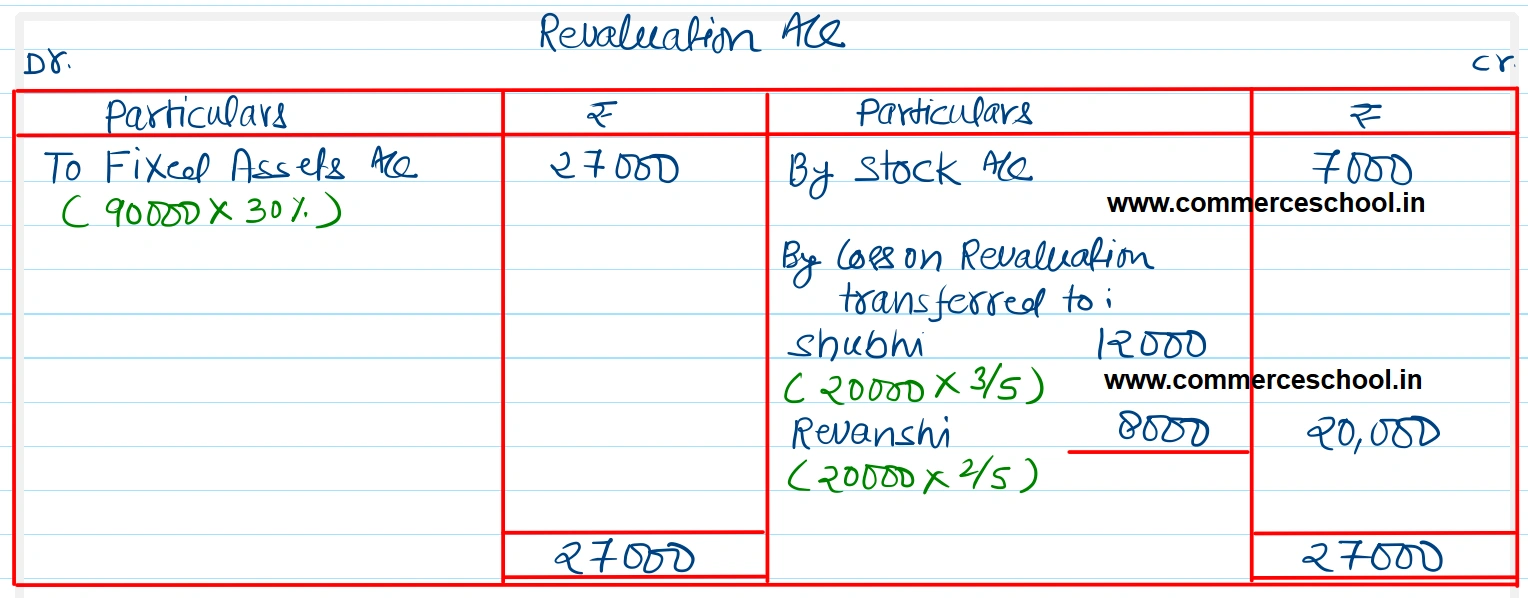

(ii) Fixed assets were depreciated @ 30%.

(iii) Stock was valued at 45,000.

(iv) Bank loan was paid off.

(v) After all adjustments capitals of Shubhi and Revanshi were to be adjusted taking Pari’s capital as the base. Actual cash was to be paid off or brought in by the old partners as the case may be.

Prepare Revaluation Account and Partners’ Capital Accounts.

(CBSE 2024)

[Ans: Sacrificing Ratio-3 : 2; New Profit-sharing Ratio-9 :6:5, Revaluation Loss 20,000; Shubhi will withdraw cash of₹ 6,000 and Revanshi will bring cash of₹ 4,000; Partners’ Capital Accounts: Shubhi 90,000; Revanshi 60,000; Pari 50,000.]

| Liabilities | ₹ | Assets | ₹ |

| Capitals: Shubshi Revanshi | 60,000 32,000 | Fixed Assets | 90,000 |

| General Reaerve | 30,000 | Stock | 38,000 |

| Bankn Loan | 18,000 | Debtors | 30,000 |

| Creditors | 70,000 | Cash | 52,000 |

| 2,10,000 | 2,10,000 |

Anurag Pathak Answered question