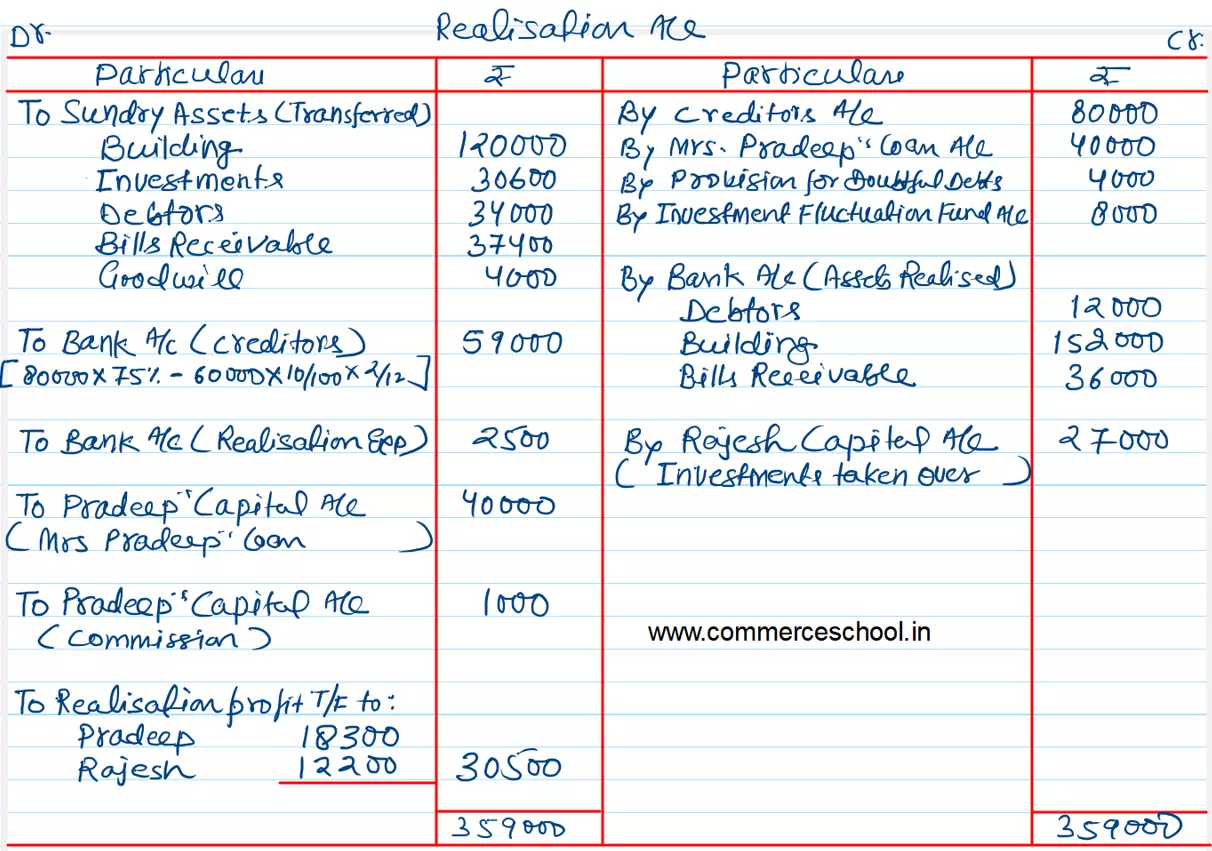

Pradeep and Rajesh were partners in a firm sharing profits and losses in the ratio of 3 : 2. They decided to dissolve their partnership firm on 31st March, 2018.

Pradeep and Rajesh were partners in a firm sharing profits and losses in the ratio of 3 : 2. They decided to dissolve their partnership firm on 31st March, 2018. Pradeep was deputed to realise the assets and to pay off the liabilities. He was paid ₹ 1,000 as commission for his services. The financial position of the firm on 31st March, 2018 was as follows:

| Liabilities | ₹ | Assets | ₹ |

| Creditors

Mrs. Pradeep’s Loan Rajesh’s Loan Investment Fluctuation Fund Capital A/cs: Pradeep Rajesh |

80,000

40,000 24,000 8,000 42,000 42,000 |

Building

Investment Debtors Bills Receivable Bank Profit & LOss A/c Goodwill |

1,20,000

30,600 30,000 37,400 6,000 8,000 4,000 |

| 2,36,000 | 2,36,000 |

Following terms and conditions were agreed upon:

(a) Pradeep agreed to pay his wife’s loan.

(b) Half of the debtors realised ₹ 12,000 and remaining debtors were used to pay 25% of the creditors.

(c) Investment sold to Rajesh for ₹ 27,000.

(d) Building realised ₹ 1,52,000.

(e) Remaining creditors were to be paid after two months, they were paid immediately at 10% p.a. discount.

(f) Bill receivables were settled at a loss of ₹ 1,400.

(g) Realisation expenses amounted to ₹ 2,500.

Prepare Realisation Account.

[Ans.: Realisation Gain – ₹ 30,500; Payment to Creditors – ₹ 59,000.]

Anurag Pathak Changed status to publish